Fundamental Forecast for Dollar:Neutral

- Despite the downgrade in 1Q GDP this past week, hawkish speculation surrounding the Fed outlook fed the Dollar

- NFPs, the PCE deflator and Fed speak will offer rate speculation milestones; while risk trends and cross winds stir

- See the 2Q forecast for the US Dollar and other key currencies in the DailyFX Trading Guides

Though the USDollar cooled its pace modestly from the strongest weekly advance in two years, the currency nevertheless put in for another impressive advance. Once again, the FX market seems to be focusing its appreciation to the first-mover status on monetary policy; and the Greenback is well positioned to reap the benefits. However, recovering from a month of consolidation and further month of retreat is not especially difficult to muster under favorable winds. To fully revive the Dollar’s run of the past year and carry further to 12 year highs, though, will take a far more convicing fundamental push.

Two weeks ago, the USDollar regained traction after a month-long slide. The spring board for this recovery was a shift in the tone surrounding the Fed’s monetary policy bearings. Some of the market’s more closely-followed instruments for timing rate hikes (Fed Fund futures and Treasury yields) didn’t seem to move forward their assumptions of that first 25 basis point hike. Fed Fund futures are still pricing a liftoff all the way out to January 2016 and the curve has not steepened despite warnings by various officials that a late start would likely translate into a faster pace thereafter.

There is some merit to a dispirate forecast across asset types, but from FX we also experience a greater appreciation of relative position. While the market may steadfast in its doubt of a hike this year – despite the concerted efforts of Chairwoman Yellen, Vice Chair Fischer and others to emphasize this possibility – it is still a more hawkish bearing than those considering rate cuts (RBA, RBNZ) or pursuing QE programs (ECB, BoJ). All that is needed is a general appreciation for yields and the benchmark currency is bestowed a greater degree of demand. Before the Great Financial Crisis razed global interst rates, we would see this same feature when a high-yielding currency would advance whether its own benchmark rate were raised or the appetite for yields simply acted as a tide that lifted all ships.

A general appreciation of diverging monetary policy efforts has proven a key motivator for the currency market – not to mention the source of major trends and a principal reason FX volatility has proven stickier. That said, even relative perspective will have limitations so long as the world’s monetary policy hold near the zero bound. That means, progress from a leader like the US Dollar increasingly demands progress on its own advantage or perhaps a new driver.

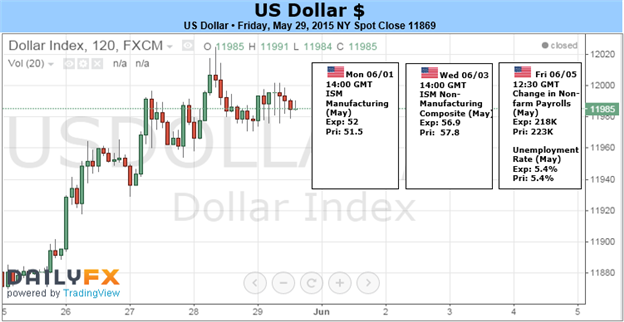

To fuel or quench interest rate expectaitons in the week ahead, we have a range of event risk that is more than capable of drawing out the hawks and doves. A range of Fed speeches and data will be bookended by two key pieces of event risk. On Monday, the BEA’s PCE deflator – the Fed’s favored inflation gauge – is due. If the argument for an earlier hike is going to be made, it will be made through evidence of revived price pressures. Friday’s NFPs will be another headline-crowding event. That said, payrolls and unemployment will ultimately matter less than wage growth – another wage figure.

Interest rate forecasting has proven the most tangible motivator for fundamental traders these past months, but it is not the only game in town for price and volatility. Risk trends should not be underestimated for its heavy influence over the market. Volatility measures in different capital markets look dangerous, but not as dangerous as equity indexes like the S&P 500 and Shanghai Composite. Meanwhile, the ‘relative’ factor to exchange rates should have us also looking at Greece, the RBA rate decision and other event risk that can buoy or crush the Dollar’s most liquid counterparts. -JK