AUSTRALIAN DOLLAR FORECAST: BEARISH

- The Australian Dollar has the RBA poised for action ahead

- Commodities and yield spreads can’t fight a runaway US Dollar

- Fed hawkishness boosted USD. Will AUD/USD make a new low?

The Australian Dollar started last week on the back foot after the release of PMI data on Monday. The January numbers show the IHS Markit Australian Composite PMI fell to 45.3 from 54.9 previously.

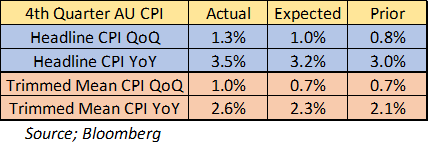

Tuesday saw the release of CPI with both the headline and trimmed mean measure beating expectations.

The RBA monetary policy committee will be meeting this coming Tuesday. The rate of inflation itself, is not too concerning for them, but the rate of acceleration of the price increases in the latest data will be of concern.

The RBA has a mandated target for headline CPI to be 2-3% on average over the business cycle.

While the headline number is above the target range, trimmed mean remains at a reasonable pace. The RBA place an emphasis on the trimmed measure of CPI as it excludes volatile inputs and allows for an interpretation of prices that sees through short term noise.

The impact of Omicron going into the end of last year and to start 2022, may have slowed price pressures. However, the underlying strength in demand might be enough to trigger a response from the RBA.

They have already telegraphed that the asset purchase program is under review and these CPI numbers will give them every excuse to reduce it or abolish it all together. It is currently running at AUD 4 billion a week.

A rate hike seems unlikely this Tuesday, and the market is not expecting lift-off until the June meeting, although it has priced in a 60% chance for a May hike.

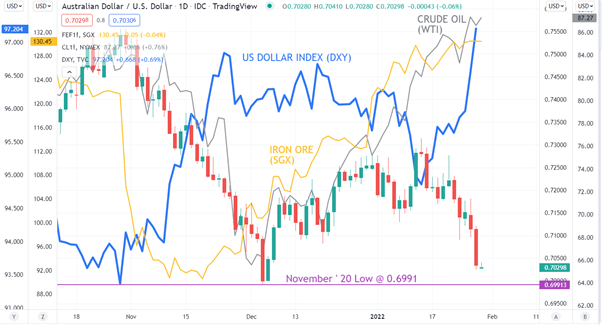

Iron ore, energy commodities, aluminium, wheat, gold, copper and many of Australia’s other top exports are trading at healthy historical prices. But it means nothing for the Aussie when the US Dollar is roaring higher.

The Federal Reserve meeting last week saw the central bank turn more hawkish than had been expected. In particular, Fed Chair Jerome Powell did not rule out a rate hike at every meeting this year, starting in March, should conditions warrant it.

This saw real yields rise and equities sell-off, creating a risk-off environment. Despite yield spreads moving in favour of AUD, it remains vulnerable when the macro backdrop for risk appetite is deteriorating, as it is now.

The US Dollar has been the driver for AUD/USD and until the fallout from the Fed is digested, risk assets such as AUD are likely to remain under pressure.

The chart below highlights the impact the strength that the US Dollar (DXY) is having on AUD/USD.

CHART - AUD/USD, US DOLLAR INDEX (DXY), IRON ORE (SGX) AND CRUDE OIL (WTI)

Chart created in TradingView

--- Written by Daniel McCarthy, Strategist for DailyFX.com To contact Daniel, use the comments section below or @DanMcCathyFX on Twitter