The US central bank announced a significant shift in its monetary policy stance to end 2021, but the ultimate impact of the more hawkish bearing seemed to barely register for the Dollar and risk assets in general. If we were to take the lack of direction of this systemically important shift at face value, it would be easy to interpret that some other fundamental consideration is directing the Greenback - or that we have simply disengaged from economic and financial currents altogether. However, it would be short-sighted to believe that some of the most influential winds in the market no longer matter. Anticipation bolstered by forward guidance certainly helped to soften the blow of the late news, but thinned liquidity was arguably the most distortionary aspect. As we move into 2022, markets will fill back out and the Fed will find itself near the hawkish end of the pack. So what course will the Dollar follow into the new year?

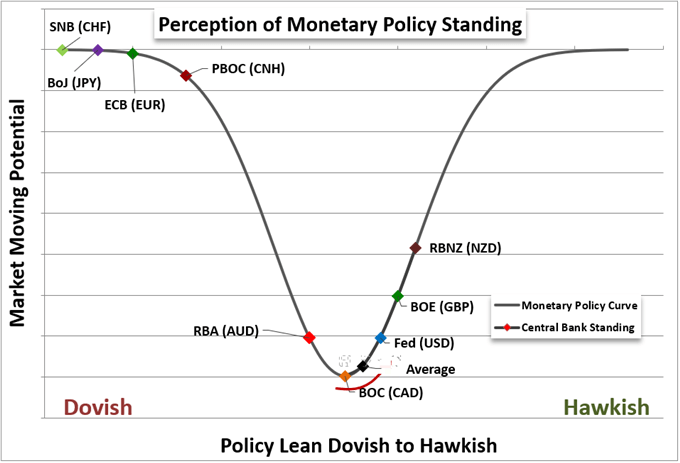

The Monetary Policy Depth Charts

As we enter a new trading year, we also seem to be transitioning into different monetary policy waters. While there are still some very notable doves among the major central banks (such as the European Central Bank and Bank of Japan); the majority are tapering, projecting near-term rate hikes or already lifting their benchmarks. That backdrop is important because it gives context of relative value. Were it only the Federal Reserve that were on course to raise rates while other major peers were static or easing, there would be a distinct carry advantage to the Greenback? That is, of course, a favourable tail wind so long as the post-pandemic risk appetite run carries over uninterrupted into the new year. As it stands, some of the currencies that have enjoyed a carry advantage to the Dollar in the past - including the British Pound, New Zealand Dollar and Canadian Dollar - once again hold a current and forecasted yield premium, yet this is also where the Dollar has gained traction more aggressively over the final two months of the past year.

Chart 1: Relative Monetary Policy Stance – From John Kicklighter

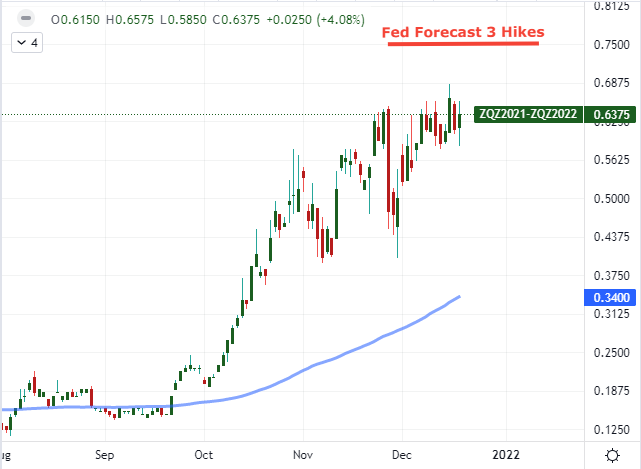

Forecasts carry more weight in future movement than do current yield differences. This represents a greater downside risk for the US Dollar through the first three months of the year. At the December 15th FOMC rate decision, the policy statement announced the accelerated pace of taper ($30 billion per month) which would bring QE to an end by end of March, while the summary of economic projections (SEP) raised the forecast for rate hikes in 2022 to three 25 basis point hikes. That is modestly more aggressive than what the market was expecting the central bank to adjust to - from a single 25 bp hike in September - so there is perhaps a little more upside on this fundamental dimension moving forward. However, a further acceleration of rate forecasts is improbable without it representing alternative issues. If the Fed is hiking at a pace faster than three hikes over the span of 9 months, if we consider the first move comes after the end of taper, is fairly aggressive with the state of economic uncertainty. Such a move would likely only come in an environment where other central banks are raising under similar duress from inflation, which would temper the carry potential. Alternatively, if financial pressures build and the US central bank throttles back its forecasts, it would likely lead to a significant loss of altitude for the Greenback.

Chart 2: US Rate Change Forecast Implied from 2022 Fed Funds Change - Daily Timeframe (August to December 2021)

Source: TradingView; Prepared by John Kicklighter

Adding Risk Trends to the Mix

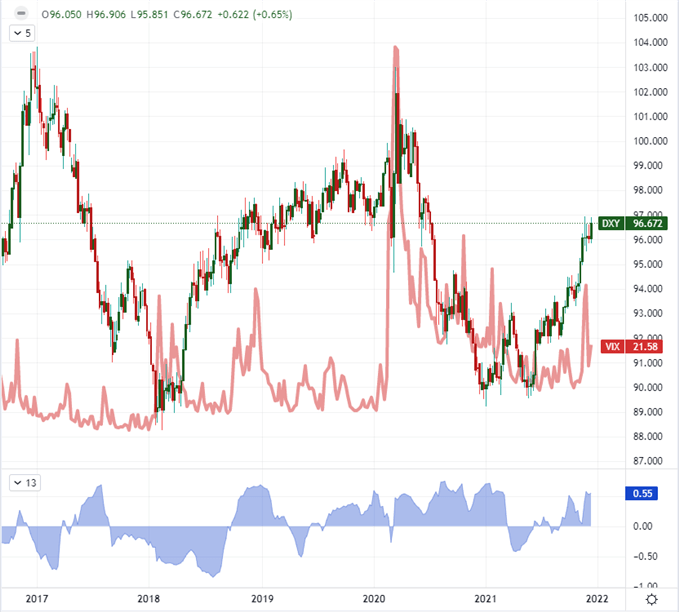

There has been a shift in the monetary policy tempo through the second half of 2022 for a reason: inflation has proven more persistent than authorities had bargained for. While there are those that view inflation only in what it means for central bank policy, it is important to remember there are very real-world economic implications. The rise in costs of goods at the wholesale, business and consumer level throttle economic activity. If the slowdown in recovery is too sharp, it can readily compound the existent concerns floating around the market and the rich level of the markets at large, in turn leading to a market retreat. As a carry currency, the Dollar has a lot of ground to lose after the Dollar's charge through the second half of this past year. For those that have traded through more extreme market periods, a bearish view of the US currency during risk aversion may seem counter to everything the textbooks suggest; but the Greenback is more appropriately a haven of last resort. If we slide into a period of 'risk off' that encompasses the entire financial system, then the Dollar may resort to its more rudimentary role. Otherwise, treat it as a risk asset.

Chart 3: DXY Dollar Index Overlaid with VIX and 20-Week Correlation (Weekly)

Source: TradingView; Prepared by John Kicklighter

External Risks That Aren't Central Bank Anchored

With the Dollar's safe haven status in mind and a shift in focus from localized monetary policy, there are other matters that Dollar traders need to contemplate through the opening run of 2022. The complication of the impending US debt limit is a deadline that keeps resetting. After another last-minute delay, threat of an unthinkable US default has shifted to the first quarter of 2022. In all likelihood, the government will find enough support for another delay, but the markets will never doubt this move. More uncertain is the situation with the newest wave of the coronavirus. The omicron variant has seen a resurgence in infections on the coast while certain countries across the ocean have already acted to shut down their economies to halt the spread. Will US officials be forced to eventually follow a similar solution?