US Dollar Fundamental Forecast Talking Points

- The Dollar ended the third quarter with a meaningful technical breakout, backed by hearty fundamental themes previous ignored

- Monetary policy forecasts find the Fed making a clear effort to acclimatize the markets to an impending taper, which would be a turning point in the bank’s policy cycle

- If risk trends collapse, the Fed may have to delay its plans to normalize; but the Dollar also has a safe haven appeal that could benefit in most scenarios

We are heading into the final quarter of 2021 with an unmistakable sense of change underway. The tempo of the global economic recovery from the pandemic-led recession slowed noticeably. Central banks were starting to ease up on their exceptional support structures, initially through ‘tapering’ their massive stimulus programs. Further, there were financial stains showing through different systemically important areas such as the Chinese real estate market and yet another standoff on the US debt ceiling. Such transitions bring uncertainty and frequently volatility. That represents a likely boon for the US Dollar given its liquidity and safe haven properties. Yet, as always, there are scenarios which could undermine the currency’s traction.

The Post-Pandemic Recovery Slows

The world’s economy may have not fully recovered from the impact of the abrupt and severe pandemic-led recession in the first half of 2020, but it has certainly recovered quickly. With fiscal and monetary support deployed by authorities across the globe, the cooperative effort proved remarkably effective. However, the scale of external support implemented cannot be maintained indefinitely. To sustain such policies would create inevitable points of instability such as uncontrollable inflation and financial bubbles. In fact, the seeds of these vulnerabilities may already be sown; but officials are still aiming for a controlled landing.

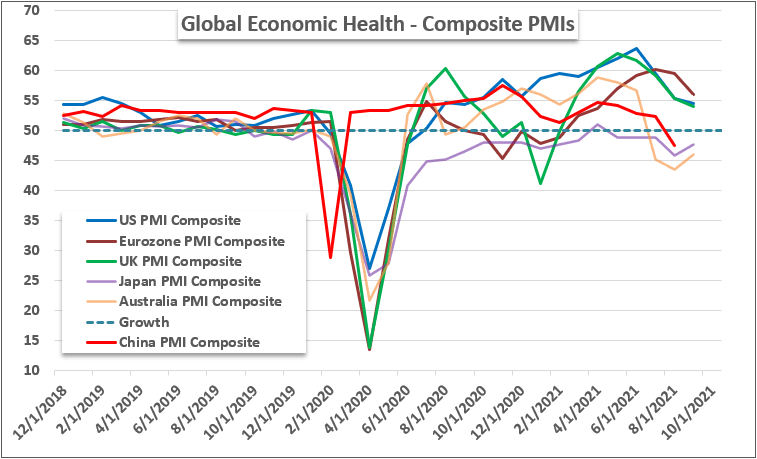

As the global ship rights itself, we have naturally seen the pace of economic measures temper. That should come as no surprise as growth normalizes and indicators based on rates of change (such as GDP) inevitability plateau. However, this routine stage in the cycle does not necessarily soothe consumers, businesses and governments the world over which have indirectly used forms of leverage to weather the storm and take advantage of the recovery. As the global pace of growth slows, the sense of universal opportunity recedes; and the capital starts to flow towards those areas of the financial system with both the depth and heft to offer stability of returns. While there will be some inevitable competition from the developed world, the US looks to be a direct benefactor of the qualified-risk pursuit. As an impressive baseline, the FOMC upgraded its 2022 GDP forecast to 3.8% in the September Summary of Economic Projections.

Chart 1: Major Economies Composite PMI Surveys

Forecasted Fed Hikes and Community

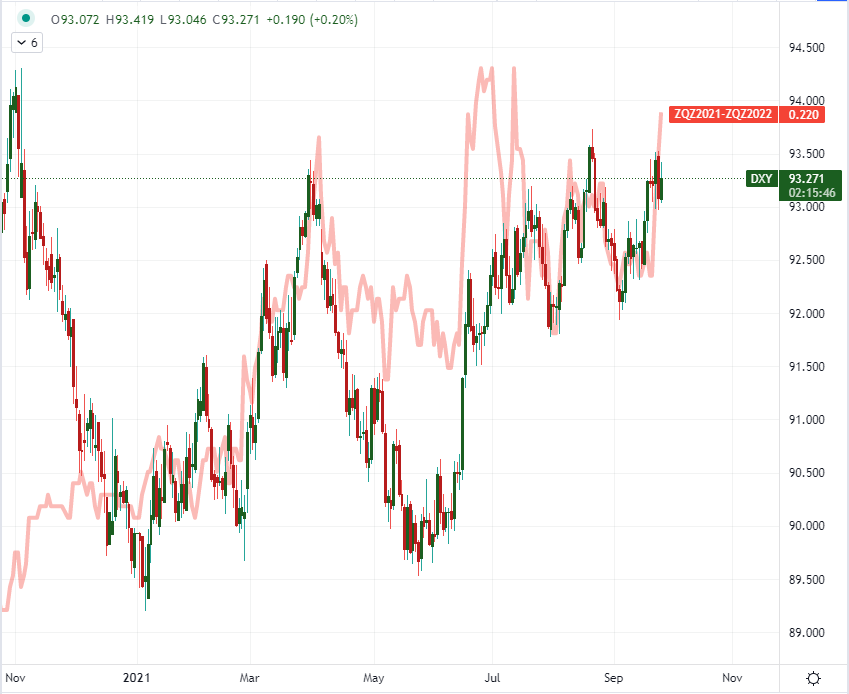

A recovery in economic strength is a strong motivation for central banks to rein in their extreme accommodation policies and that seems to be well underway heading into the final quarter of the year. While not all of the largest players are joining in the effort to ease back on stimulus programs, a host of the major players have acted, announced or hinted at taper. While those investors that have benefit from the perception of unlimited support from these deep-pocketed asset buyers may not appreciate the moderation, a collective shift can help reduce distortions in segments of the financial system which can frequently birth contagious financial events. For the Fed’s part, it ended the third quarter with a clear suggestion at the conclusion of its September policy meeting that the taper plan would be announced at the next meeting unless something went seriously wrong. Further, Chairman Powell suggested the winddown could end by mid-2022 and the first rate change could come at the end of the same year. That is relatively hawkish for the Dollar.

Chart 2: DXY Dollar Index and Implied 2022 Fed Funds Change

Source: TradingView; Prepared by John Kicklighter

Still a Top Safe Haven – With a Few Exceptions

If the world’s policymakers are able to land their efforts to stabilize economic expansion and shift risks held on their own records back on the market-at-large, the Greenback and US assets would be in a good position to take advantage of the fundamental winds. Alternatively, there has been an enormous amplification of risk over the past 18 months owing in large part to the bluntness of tools available to officials to fight the financial fire. An unintended but inevitable side effect of this effort was the fostering of moral hazard – taking on risk without worry as to the consequences related to that exposure. As growth cools and market volatility increases, the scrutiny investors will pay towards their existing risks and any further exposure will increase substantially. That evaluation is overdue given the unrelenting drive of speculative benchmarks like the S&P 500 and the measures of leverage like the NYSE client margin hitting records. In the event that this critical examination triggers risk aversion, the Dollar’s safe haven status is in good position to offer fleeing capital harbour.

While the Greenback is in general a top haven candidate during most scenarios of financial stress, there are a few probable courses which may lead capital to seek shelter elsewhere. The most prominent localized risk for the US currency and its fiat assets would be a crisis born out of the national debt limit. Heading into the final three months of the year, the federal government was once again haggling over the debt ceiling. A shutdown of the government is a tangible scenario that we haven’t seen in some years. While this is a situation best avoided, it is not truly critical. Missing a payment on debt already incurred would be potentially catastrophic for the global financial system, much less the US markets. While still a very low probability, the brinkmanship in Washington, DC could still result in troubling consequences like a sovereign credit downgrade similar to the Standard & Poor’s US downgrade in 2011. We justified the ‘risk-free’ value still owed Treasuries despite that cut, but it would be a very different situation should there be a second downgrade.

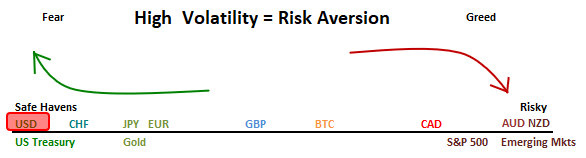

Chart 3: Risk Spectrum for Assets