DAX 40, Russian Default, Crude Oil, Fed, Beige Book, NZD, BoJ, JPY - Talking Points

- The DAX 40 is steady even though risks are growing

- Fed hikes are on the way, it is just a matter of how fast

- Equities hit pause for now - will the DAX recovery continue?

The DAX 40 has held up despite German energy supply from Russia coming under further scrutiny.

The finance minister appears to be a logger heads with the foreign minister over the timing of withdrawing dependence on the Eastern source. The former describes the exit from Russian energy happening as fast as possible. The latter says that oil imports will cease by the end of the year.

A Russian debt default might be on the horizon. The Credit Derivatives Determinations Committee (CDDC), made up of mainly US investment banks, identified a “potential failure to pay” on a credit default swap. This could lead to a technical default.

In the meantime, crude oil is little changed from yesterday’s open, with the WTI futures contract near US$ 103 bbl and the Brent contract just under US$ 108 bbl.

The Federal Reserve’s Beige Book was released late yesterday, with concerns around inflation and geopolitics revealed as central for the US central bank. The full report can be read here.

Separately, San Francisco Fed President Mary Daly said, “I see an expeditious march to neutral by the end of the year as a prudent path.” Many markets analysts see neutral as 2.5%.

Treasury yields tumbled none-the-less as a number of analysts recommended the recent rout in bonds (the inverse of higher yields) as a buying opportunity. Borrowing costs recovered around 5 basis points in Asia, with the 10-year Treasury note now returning to around 2.87%.

Gold is slightly softer in Asia as yields tick up, trading around US$ 1,950 an ounce.

Wall Street had a mixed day, with the Dow up slightly, the S&P 500 down a bit and the Nasdaq losing 1.22%. Tesla reported better than expected profit results after the bell and this has seen Nasdaq futures lead the main US indices into the green in the Asian session.

Trade Smarter - Sign up for the DailyFX Newsletter

Receive timely and compelling market commentary from the DailyFX team

APAC equities have been mixed, with Hong Kong and Chinese mainland indices going south while Australian, Japanese and South Korean bourses found slightly firmer footing.

Chinese President Xi Jinping gave an address that didn’t seem to relieve investors looking for further stimulus measures. He kept to a vague political script that pushed a united Asia agenda and had a subtle dig at the West.

The New Zealand Dollar went lower after CPI data missed expectations. This would be a welcome relief for the RBNZ after they hiked by 50 basis points earlier this month.

The headline year-on-year figure came in at 6.9% instead of the 7.1% anticipated, the highest level in 32-years.

The Kiwi pulled the Aussie down and the Yen maintained its merry march lower after yesterday’s reprieve. USD/JPY is now back above 128. USD and CAD have been the gainers on the day.

The Bank of Japan (BOJ) meeting next week might be interesting, with yield curve control (YCC) under the microscope. More jawboning today from Japanese Finance Minister Shunichi Suzuki did little to help the Yen.

After Eurozone CPI this morning, the US will see the weekly initial and continuing jobless claims data cross the wires.

Federal Reserve Chair Jerome Powell and European Central Bank President Christine Lagarde will be on an IMF panel examining the global economy. Bank of England Governor Andrew Bailey will also be making comments at a separate event.

The full economic calendar can be viewed here.

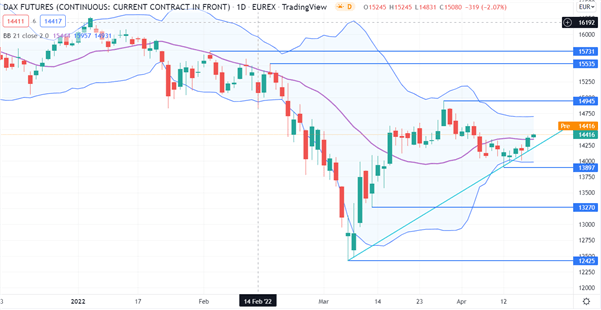

DAX 40 Technical Analysis

The DAX has continued to consolidate with a 13897 – 14945 range.

This consolidation has seen volatility decrease as illustrated by the narrowing of the 21-day simple moving average (SMA) based Bollinger Band.

Support might be provided at the recent lows of 13897, 13270 and 12425. On the topside, resistance could be offered at the prior peaks of 14945, 15535 and 15731.

--- Written by Daniel McCarthy, Strategist for DailyFX.com

To contact Daniel, use the comments section below or @DanMcCathyFX on Twitter