Talking Points:

- Oil prices have seen a dramatic drop over the past 24 hours, seemingly triggered by a comment from Oil magnate, Harold Hamm.

- This has raised fresh questions as to whether last year’s bullish move in Crude Oil prices has sustainability. Below, we look at a series of support levels to follow for such a theme.

- If you’re looking for trading ideas, check out our Trading Guides. And if you’re looking for ideas that are more short-term in nature, please check out our Speculative Sentiment Index (SSI) Indicator.

To receive James Stanley’s analysis directly via email, please SIGN UP HERE

Oil prices have spent much of the past 24 hours heading-lower, falling below a key psychological level at $50/brl and a 17+ year trend-line that’s held as support in WTI since mid-December. The catalyst appeared to be a comment from Oil Magnate Harold Hamm; who warned that U.S. Production growth ‘is going to have to be done in a measured way or else we’ll kill the market’. If the past nine years have taught global markets anything, doing things in a ‘measured way’ doesn’t appear to be a popular strategy within the United States economy; and this comment has been construed as a potential pain factor for the future of oil prices.

Chart prepared by James Stanley

In the summer of 2015, the Fed was still under the presumption that lower Oil prices would actually stimulate the U.S. economy. Because the United States had imported so much Oil in the past, a correlation had developed in which lower oil prices would mean more discretionary income for consumers – and this was income that would usually be re-directed towards other purchases. So the money that would normally filter-down to Oil producers could be re-directed towards consumer purchases. But as U.S. shale production continued to grow, the United States dependency on foreign sources of Oil diminished. And as we saw in in Q1 of last year, lower Oil prices could expose a very fragile section of the American economy given this heightened importance on shale production. Many banks were levered-up on debt to energy companies. Lower oil prices made it more difficult to service that debt. And if a group of oil producers with which U.S. banks are highly-levered are all going through the same pain factor at the same time, this could create a capital squeeze within the banking system.

And this really triggers a lot of different fears from a lot of different places. Dwindling oil prices became a major macro headwind in early 2016; but Oil prices reversed and began putting in bullish-moves starting on the second day of Fed Chair Janet Yellen’s Humphrey-Hawkins testimony on February 11th of last year. Since then we’ve seen the insertion of a few additional bullish drivers, mostly on the supply side of the equation as an OPEC deal struck in November helped to further stoke bullish motivation.

Chart prepared by James Stanley

But this is another area where matters have changed with the shifting landscape of global oil production. OPEC, as a cartel, used to wield considerable power. But with the rise of Russian energy production and the continued advancements in shale extraction in the United States, non-OPEC producers became increasingly more-important. This also makes coordinating strategy more difficult, as a ‘co-opetition’ develops amongst oil producers in and outside of the cartel. So, the sustainability of the ‘deal’ reached in November had questions surrounding it from day one. The election of President Donald Trump opened up a range of possibilities for further drilling and extraction out of the United States, so Mr. Hamm’s comment appears to be an example of ‘saying what many were fearing’.

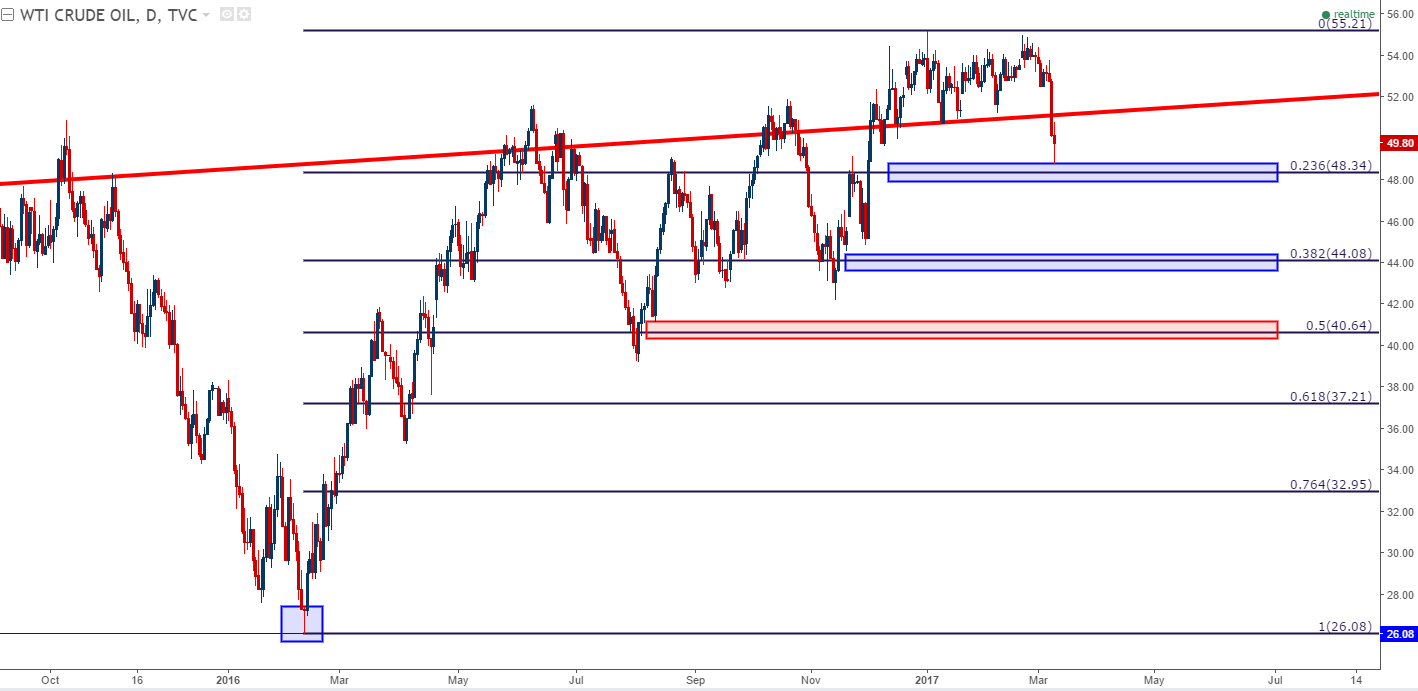

The big question is whether this bearish-move has sustainability. On the chart below, we look at some key areas to watch for such a theme. This morning’s swing-low in WTI bounced right-off of the 50% Fibonacci retracement of the most recent bullish move. If prices are able to break-below this zone, the prospect of near-term bearish continuation could appear more-likely:

Chart prepared by James Stanley

For the ‘bigger picture’ or longer-term reversal, there are key support levels at 48.34 and then 44.08. Breaks-below these areas will open the door for a ‘bigger picture’ bearish move; and if the level of $40 is crossed, trouble is likely-ahead for Oil prices.

Chart prepared by James Stanley

Is the Bear Coming Back to Oil Prices?

This is still a very young, panic-prone move off of a singular comment; so we probably want to tap the breaks on making a ‘big picture’ prognostication off of just a day’s worth of price action.

But – Oil prices have shown a sensitivity to a hawkish Fed. This is what helped to really hasten that down-trend in Q1 of last year: The Fed said that they wanted to hike a full four times in the year and Oil prices didn’t appear to like any of that. It wasn’t until the Fed capitulated on those expectations that Oil prices began to rise again, and that strength held throughout the Presidential Election and rate hike in December as the Fed remained relatively passive.

But more recently, the Fed has ramped-up that hawkishness again; and this appears to be what’s put Oil prices in such a vulnerable state that a single comment from Mr. Hamm could break the prior bullish trend. So – the most likely determinant as to whether Oil prices continue this bearish theme is going to be just how hawkish the Federal Reserve is next week when they’re largely expected to hike rates.

For traders looking to navigate such themes – watch price action. If sellers are able to over-take these longer-term support levels, we might be in the midst of another ‘shift’ in the spectrum of Oil prices.

--- Written by James Stanley, Analyst for DailyFX.com

To receive James Stanley’s analysis directly via email, please SIGN UP HERE

Contact and follow James on Twitter: @JStanleyFX