Talking Points:

- The Chinese Yuan officially became a 'reserve currency' as part of the IMF's SDR basket as of October 1. Since then, the Yuan has continued to weaken, and this may be bringing some element of pressure into global equity markets.

- October has already been an eventful month for markets; and the Chinese Yuan hasn't been the only driver as we’ve also seen a growing concern around a pivot in rate hike policy out of the Federal Reserve from the United States.

-If you’re looking for trading ideas, check out our Trading Guides. They’re free-for-all and updated for Q4.

To receive James Stanley’s Analysis directly via email, please sign up here.

Global stocks are lower thus far on the morning, and there are a couple of potential drivers for such a move. The big piece hitting the headlines was another contraction in Chinese exports. Chinese exports were down -10% year-over-year versus expectations for a decline of -3.3%; and while a portion of that move is likely due to the weaker Yuan and stronger US Dollar, this does counter the hope or expectation that a weaker Yuan would bring on a direct increase in trade.

This was a big part of the heavy concern around China in Q3/Q4 of 2015; that a drop in global demand would bring a deeper and wider slowdown in China. And with so much leverage in the Chinese economy, that slowdown could potentially get really very bad; so bad that it might impact the rest of the world. While Chinese consumption of imported products may not appear to be a threatening factor to many economists, the exposure amongst foreign banks to the Chinese economy certainly should be.

A novel way to manage trade flows is through the currency. A weaker currency could improve exports, as the lower prices in foreign markets could spurn additional demand. So, as the Chinese Yuan was being fixed weaker by Chinese regulators, global markets have taken notice. On the chart below, we’re looking at the USD/CNH spot rate along with the S&P 500. Notice how there has been a slightly delayed response in equity selling after a quick spike in USD/CNH.

Chart prepared by James Stanley

Throughout the first half of this year Chinese policymakers rushed-in new policies and strategies in the effort of shoring up their capital markets. A big part of this has been controlling the spot rate in USD/CNH, and for much of the year the 6.7000 level provided somewhat of a ‘psychological barrier’ on the pair. But on October 1 the Yuan officially became part of the SDR currency basket. Since then, matters haven’t really been the same, as the Yuan has been continually weakening, moving well beyond that 6.7000 level. And as this weakness has continued to increase, pressure in equity markets has begun to show more prominently.

There are two big questions to answer here: 1) Are Chinese regulators going to continue to aggressively weaken the Yuan now that the currency is part of the SDR reserve basket and 2) Will that additional weakness bring continued pressure into global equity markets.

The answer to the second part of that question is likely related to another factor of pressure that has been picking up of recent, and that has to do with the potential for tightening of rates in the U.S. economy.

USD Holding Resistance as Rate Hike Fears/Expectations Drive Markets

We discussed this theme on Tuesday and since then we’ve had the release of meeting minutes from the September FOMC meeting; further confirming the fact that there is a growing chorus within the Federal Reserve that believe that recession odds may be higher should rates stay low. And this really speaks to the theoretical part of the argument regarding rate policy. In one camp, we have the extreme neo-Keynesians that see little reason to raise rates off of ‘emergency-like’ levels due to a lack of inflation. In the other camp, we have the lighter neo-Keynesians that believe that policy should be normalized more quickly, regardless of stock prices as that is not one of the Fed’s mandates, in the effort of addressing very real long term risks of low rates for pensions and defined benefit funds.

Which camp is right, nobody really knows. But what we do know is that there has been massive dislocation in both equity and bond markets around-the-world, and much of this is resultant of artificially low rates trying to masquerade monetary policy as fiscal-like measures. And this isn’t just the United States; this has become a global phenomenon. It’s just that the US is at the forefront of this theme as it’s the first economy that’s attempted to ‘normalize’ rates after so much accommodation. For the extreme neo-Keynesians, this isn’t much of a concern for now; markets are still trading very near all-time-highs, and these folks don’t seem to mind much that investors are now treating stocks like bonds (for dividend payments instead of interest-bearing coupons), and bonds like stocks (for capital appreciation as rates drive even lower, pushing prices higher).

But for the ‘lighter neo-Keynesians,’ the fear is in what hasn’t yet happened, or the realization that this level of dislocation rarely just ‘works itself out.’ That’s what we’re hearing Ms. Loretta Mester talk about right now, and this is what Ms. Yellen touched on last year in December when the bank finally hiked rates after nine years of holding them flat.

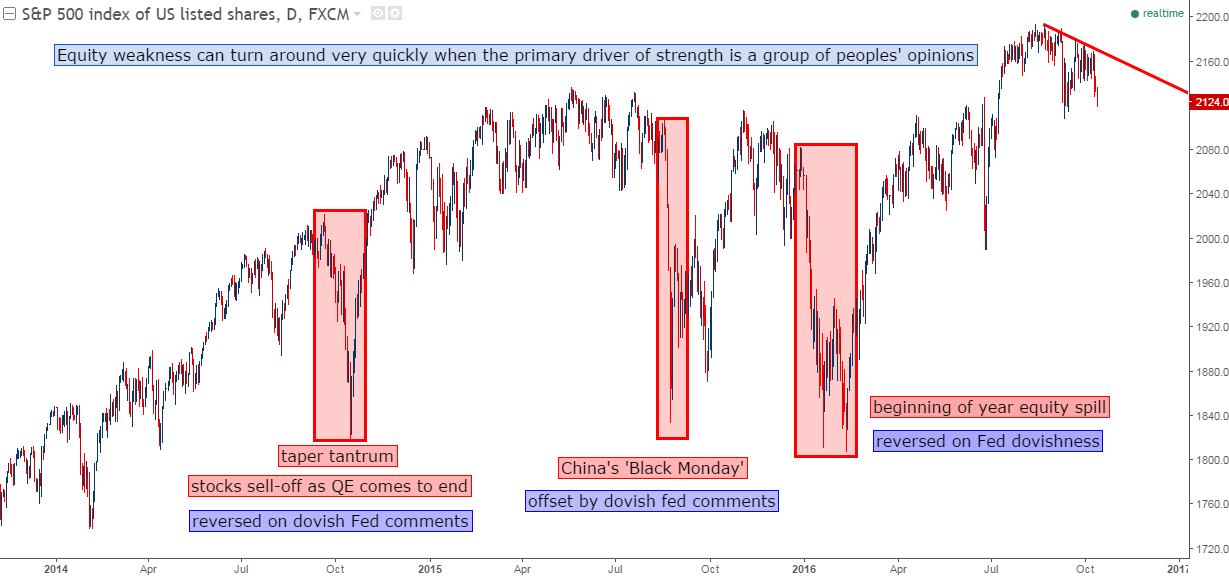

The big fear here is that the Fed might pull the punchbowl. Much of the world is loaded up on trades in markets that are being not only supported, but driven by Central Banks; and should that support all of the sudden just dry-up, well there could be some very vicious selling nearby. Central Bank support has been key to the continued drive-higher in global equities. Each time pressure has begun to show in the S&P 500 over the past year, weakness was offset by more dovish Fed commentary.

Chart prepared by James Stanley

Is this likely to happen soon? Probably not, at least if we take recent history into account; this is very similar what helped to create sell-offs in Q4 of last year, and again in Q1 of this year as the Fed held exuberantly-aggressive rate hike expectations going into each of those periods. But as equity markets collapsed in each instance, the Fed rushed to markets with more dovish commentary and promises of ‘looser for longer.’ Since the last bash of weakness, we’ve even heard Ms. Yellen mention the prospect of negative rates being on the table (February 11th), and then in August the idea was floated that QE could be used, again, to offset incoming equity weakness.

So, it looks as though any ‘major’ market sell-offs (like S&P below this year’s low of 1810) aren’t going to happen until the Federal Reserve is ready to let markets move lower; unless another factor creeps up that the Fed may not be able to offset - like a larger slowdown in China or a European bank blowing up. But outside of that, it would appear that higher stock prices are at the whit and whim of the Fed. We discussed this theme in the Q4 forecast for global equities entitled, Picking Up Pennies in Front of the Steamroller. To get the full DailyFX Q4 Trading Guide, please click here.

--- Written by James Stanley, Analyst for DailyFX.com

To receive James Stanley’s analysis directly via email, please SIGN UP HERE

Contact and follow James on Twitter: @JStanleyFX