Talking Points:

- The close of business today marks the end of Q3; and 75% of the way through the year we’ve already seen some very interesting themes develop. Below we look at three of the most pertinent themes as we turn the page into Q4.

- While US Presidential elections will likely dominate the headlines, the potential for this to be a ‘major’ market driver may be a bit overrated; as the Federal Reserve still has the potential to offset additional weakness, and monetary policy is still incredibly loose. A bigger potential concern may be banking stress in Europe.

- If you’re looking for trading ideas, check out our Trading Guides.

To receive James Stanley’s analysis directly via email, please SIGN UP HERE

Tomorrow marks the end of the third quarter and the beginning of the fourth; and when traders arrive at their desks on Monday morning, all new trades will be lined up for Q4, and 2016 has already been quite the eventful year. We started with threatening risk aversion just two weeks after the December rate hike. This was the first rate hike from the Federal Reserve in over nine years; but likely more pertinent to that risk aversion was the Fed’s expectation that they were going to raise rates a full four times in the calendar year of 2016. Midway through Q1 that risk aversion reversed aggressively around Chair Yellen’s comments pertaining to the possibility of negative rates or additional policy options should the Fed need to make moves to support markets again. And this helped to return strength in areas like Oil, Stocks and International currencies.

The Second Quarter brought us the Brexit referendum. Much of the lead-up to the vote was spent talking about how there was little chance that Britain would leave and, if they did, how catastrophic the situation might become. British voters went to the polls at the end of Q2 and elected to leave, and then we spent most of Q3 bantering about the details for actually executing the Brexit. As we enter Q4, that’s still very much up-in-the-air, and it doesn’t look as though Article 50 is going to be triggered in the next few months.

There are, however, some very pertinent themes for markets as we enter the final quarter of 2016, and in this article we’re going to delve into three of the more interesting with the biggest potential to produce ‘big’ moves.

European Banking Stress

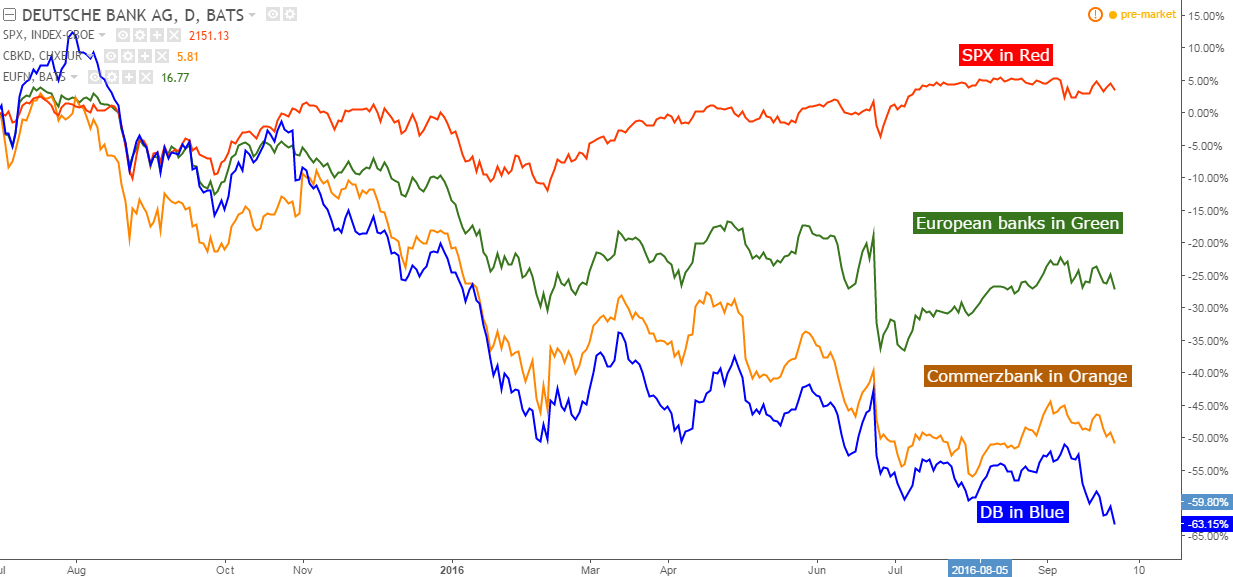

Deutsche Bank has been in the news quite a bit lately. Just a couple of days ago we did a write-up on the background behind this situation in the article, Central Banks at Full Throttle, DB Starting to Wobble. But Deutsche isn’t the only European bank facing hard times. The second largest bank in Germany, Commerzbank, recently announced that they were going to layoff nearly 10,000 workers. And if we move out of the largest economy in the Euro Zone, the situation doesn’t necessarily improve as large banks in both Italy and Spain, critical European economies; continue to face similar albeit less-profound pressures. We had discussed the situation with Italian banks back in January, so this isn’t a ‘new’ development. But what has changed since January are ECB rates. As in, they’ve went deeper into negative territory, and this only adds more pressure on European banks as their standard business model of loaning funds out at higher rates that they’re able to borrow at sees margin compression with the flattened yield curve.

The big worry here isn’t just one bank getting hit. The bigger concern is a contagion effect; because banks trade with each other and if one major bank gets taken out, this can create a nasty cascade effect across markets as other banks get pinched by counterparty risk. If Bank A trades with Banks B-Z, and Bank A all of the sudden can’t meet their margins or capitalize their positions, then Banks B-Z are left holding the bag. Banks B-Z likely aren’t oblivious, and they’ll likely take note of the pinch created from Bank A not being able to meet their obligations, and Banks B-Z will probably tighten up their risk. This means less leverage, and less leverage means selling.

We had discussed this theme back in March as it looked as though the deluge in Oil prices might have the potential to create such an environment if the losses continued. But the losses didn’t continue, and Oil prices rallied by nearly 100% in a 4-month window, and the threat of this theme took a step back from the brink. But more recently the Department of Justice in the United States levied a $14 Billion fine to DB for improprieties during the housing boom/Financial Collapse. And this raised fresh questions about the sustainability of Deutsche and, in turn, the rest of the European banking sector.

So going into Q4 this is the top theme for markets to watch because, frankly, it can have the most firepower. It’s also going to be one of the most difficult to time and follow, as this is basically a liquid situation that will continue to morph and develop as there isn’t a template-response for the ECB to handle such situations.

The Two Largest Banks in Germany Are Facing Intense Pressure (DB and Commerzbank)

Chart prepared by James Stanley

US Presidential Elections

US Presidential elections this year are a mess. If you’ve had any exposure to American media over the past 16 months you’re likely well-aware of this fact. Many have said that one candidate will bring on massive changes that could spell huge economic downturns with trade embargos and walls going up; while there are a plethora of questions around the honesty, reliability and health of the other candidate.

But perhaps more to the point US Presidential elections appear to be taking a similar tone to the Brexit referendum; where so many in the world are so sure of what’s going to happen that they’re not only basing their assumptions on these unfounded predictions; they’re allowing them to shape their entire worldview. Many appear to be forgetting that Congress plays a pretty strong role in the US political structure, and a President is not a dictator. More normally, politics is a lot of talk with little actual ‘change.’ Just as we’ve seen with the Brexit referendum: It took about 13 hours for British voters to elect to leave the European Union, and not much has happened in the three months since as politicians try to decide how to even begin the negotiation discussions.

The concern around the upcoming US Presidential election appears to be more resultant of social media, echo chambers, safe spaces and curated news feeds – all shaping social voice and opinion around a key issue (like Brexit). So while the doom-and-gloom forecasts may be entertaining to read, like somewhat of a non-fiction version of the movie Mad Max, there is very little realistic basis to make such an assertion; and to the trader reality is all that matters because that’s what can move prices to your stop or, even worse, create a margin call.

So heading into Q4 we’ll likely see some element of volatility around US Presidential elections in the middle of the quarter (November 8th); but for this to be a truly ‘game-changing’ type of move, we’ll likely need to see some other theme(s) develop to make the consequences of what might actually happen worsen.

Should stocks sell-off around the US Presidential elections, this could bring on a ‘buy the dip’ type of setup, similar to what happened around the Brexit referendum; because Central Banks are likely not going to pull the punch bowl simply because they’re unhappy with who American voters put into office in November.

On the chart below, we’re looking at how the Brexit referendum impacted the S&P 500 compared to two of the prior periods of ‘worry’ in the prior fourteen months.

Chart prepared by James Stanley

The Fed – Are We Getting a Hike in December?

One of the more pervasive market-movers this year has been expectations around Federal Reserve rate hike plans. Coming into the year, the Fed expected to hike rates a full four times in 2016. That didn’t go over too well, and by March the Fed had already whittled that expectation down to two hikes for the remainder of the year.

In June we saw even more whittling, but this time to expectations beyond 2016; and in September we saw more of the same as the Fed downgraded expectations for rate hikes beyond this year. So while the bank came into the year super aggressive, they’ve spent much of the time being passive and loose with monetary policy expectations. While the bank has been saying that November is a ‘live meeting,’ meaning that they might actually hike, the fact that this rate decision is happening just one week ahead of Presidential elections makes that look very unlikely.

December, however, sees the bank bring out a fresh dot plot matrix, there’s a press conference, and this could be a much more opportune time for the Fed to pose that next hike; and they may be compelled to do so in order to keep market participants’ trust in forecasts and guidance.

But as we’ve seen of recent, the bigger issue isn’t likely a single 25-basis point rate hike. More pressing will be the bank’s outlook into the future, and whether they pose a repeat of last year by being exuberantly hawkish for a global market that may not be ready for even more tightening.

--- Written by James Stanley, Analyst for DailyFX.com

To receive James Stanley’s analysis directly via email, please SIGN UP HERE

Contact and follow James on Twitter: @JStanleyFX