Talking Points:

- This week saw Central Bank meetings from Japan and the United States. The Federal Reserve brought more of the same while the BoJ initiated a huge shift in policy.

- The Bank of Japan is now targeting the yield curve, specifically by targeting the yield on the 10-year JGB; while the Federal Reserve remained hawkish for 2016, but got more dovish for 2017 and thereafter.

- If you’re looking for trading ideas, check out our Trading Guides. And if you want something more short-term in nature, check out our SSI indicator. If you’re looking for an even shorter-term indicator, check out our recently-unveiled GSI indicator.

To receive James Stanley’s analysis directly via email, please SIGN UP HERE

BoJ Shifts Policy: Wednesday’s Bank of Japan meeting brought the ‘comprehensive assessment’ that the bank has been talking about since their July meeting. Investors have been ambitiously embarking on one of two themes with the Yen of recent: Either weak Yen in hopes of more stimulus or a strong Yen on the thought that the bank is running out of ammunition. And after the BoJ made such an aggressive move of instituting negative rates in January, markets have been growing increasingly skeptical that the almost-four years of outsized stimulus may continue in its current fashion. So this comprehensive assessment was a big deal because this could be the first step in an entirely new strategy from the BoJ in the effort of heading off decades’ worth of deflation.

In this shift of policy announced on Wednesday, the BoJ said that they will be targeting interest rates of the 10-year Japanese Government Bond, with the target of keeping the yield flat at 0%. This is markedly different than their previous approach in which their focus was aimed towards the amount of government bonds that they were purchasing, around ¥80 Trillion per year. And that approach appeared to work, at least somewhat at first, as the Yen weakened by more than 50% in the three years following the introduction of ‘Abenomics.’ But during summer of last year China began to slow down and Chinese markets collapsed, leading to a surge in the Yen as investors in China looked for safer harbors.

Matters haven’t really been the same since then. In response to weakness in China, the PBoC ‘revalued’ the Yuan by pegging the currency to a basket of currencies as opposed to just the US Dollar. And given that the Federal Reserve had been talking up the prospect of normalization, with the expectation of that beginning at last September’s FOMC meeting, ‘revaluating’ the Yuan in August probably seemed like a pretty good idea at the time. But that revaluation freaked out global markets, and in short order of that move from the PBoC, equities around the world began to collapse, to the point that the Federal Reserve had to back down from their planned interest rate hike in September of 2015.

But as normalcy was restored in US markets with multiple incursions of dovish commentary from numerous Federal Reserve members, the Yen just continued to strengthen, erasing more and more of the ‘work’ done by the BoJ after three years of Abenomics. This led to the Bank of Japan making the very surprising move to embark on the highly-theoretical, lightly-tested prospect of instituting negative interest rates in January of this year. And for the BoJ, this worked for about a day as it led to a single day of Yen weakness followed by seven-plus months of strength; erasing about another 20% of the weakness that was driven-in by three years of Abenomics.

Chart prepared by James Stanley

This is critical for the Japanese economy, which is highly dependent on exports. As the Yen strengthens, that’s a direct detraction from Japanese corporate profit margins. And each move they tried to make to help bring weakness into the Yen has seemingly fallen flat. So something new had to happen as the BoJ’s prior strategy was a) bringing diminishing marginal returns and b) continued to extend the banks presence in key markets like Japanese government bonds.

This move to target the interest rate on the 10-year government bond as opposed to the rigid ¥80 Trillion per year in asset purchases means that the BoJ has just given themselves a bit of flexibility as they can now buy as many or as few bonds as they might want in the effort of ‘steepening’ the yield curve, while also garnering the ability to be active by no longer targeting a specific duration. But this likely isn’t a panacea in and of itself, and may be a ‘step one’ type of approach for a ‘bigger picture’ strategy that the bank and Japanese government may be looking to institute in the coming months; perhaps with deeper coordination on the fiscal front to fund Japanese infrastructure projects.

So while Wednesday may not have brought upon the bazooka that so many were looking for from the Bank of Japan, this announcement and shift of strategy may have opened the door for the BoJ to do more, perhaps even with fiscal coordination, in the coming months. The one thing that is clear is that most interests in Japan are pointed in the same direction, with the goal of stimulating the economy out of decades’ worth of deflation. And with interest rates around the world remaining incredibly low, the opportunity exists to make long-term investments into infrastructure with future QE ventures.

The story of Japanese stimulus is likely not yet over; and while the bank’s firepower of their previous strategy may have been running low, the additional flexibility afforded by this move could reinvigorate the BoJ’s approach in the months of perhaps even the years moving forward.

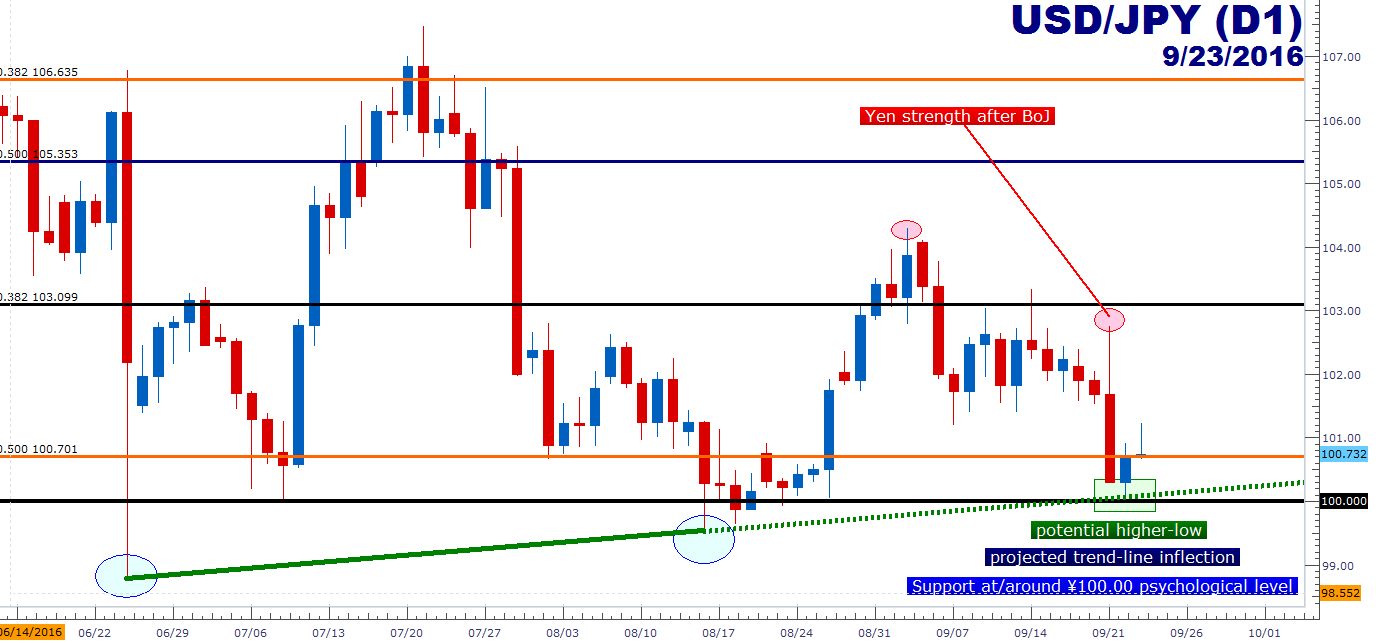

On the chart below we’re looking at the recent move in USD/JPY after this week’s BoJ and FOMC meeting. And while the selling in the pair was aggressive on Wednesday, this sent price action down to a major support zone in the pair, with prices running into a projected trend-line and the vaulted psychological level at ¥100.00.

Chart prepared by James Stanley

FOMC: Gone Until November, or, Make that December

This will be considerably shorter as there was far less by way of new information here. As widely expected, the Fed did not hike interest rates at Wednesday’s meeting. And also as expected, they did stay hawkish by pointing to the potential for a rate hike in 2016, giving markets the ‘hawkish hold’ scenario that so many expected. But, noticeably different was the Fed’s expectation for interest rates beyond 2016. The dot plot matrix saw reductions for every year after 2016 despite the Fed staying hawkish for the remainder of this year. As we had mentioned previously, this most recent September FOMC meeting carried numerous parallels to last September, in which the bank’s ‘hawkish hold’ produced even more risk aversion. By getting more dovish deeper in the future, of which these expectations are frankly quite meaningless given the cavalier changes to the dot plot matrix that have been seen this year, and the fear of the ‘hawkish’ part of the stance is offset by the ‘dovish’ expectations for future rate moves.

Or, we can state this stance in another way – the Federal Reserve is expecting yield curve flattening on the back of their monetary stance while the Bank of Japan is now actively engaging in yield curve steepening.

Thickening the drama around this theme is the fact that we’re about to hear from numerous FOMC officials in the week ahead: Tarullo and Kaplan speak on Monday, Yellen on Tuesday, Bullard, Evans, Mester and George on Wednesday; followed by Lockhart, Powell and Kashkari on Thursday.

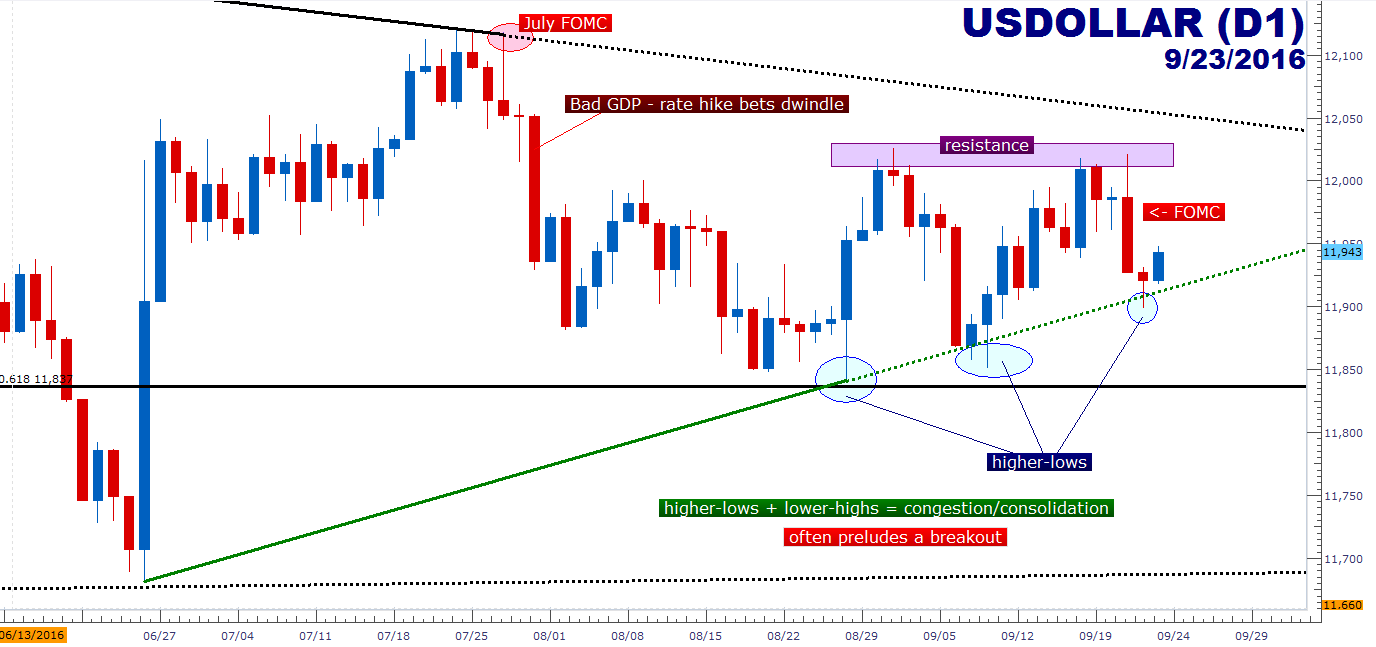

So we likely haven’t seen the end of USD-volatility around expectations for FOMC policy moves. On the chart below we look at the US Dollar, which ran down a projected trend-line as well after the recent Central Bank meeting. While USD is seeing higher-lows, it’s also in the midst of lower-highs. This is indicative of a congestion pattern that will, eventually, lead to a breakout. The big question is which side, and that will likely be answered, at least in part, by the chorus of Fed speakers that we’ll hear from next week.

Chart prepared by James Stanley

--- Written by James Stanley, Analyst for DailyFX.com

To receive James Stanley’s analysis directly via email, please SIGN UP HERE

Contact and follow James on Twitter: @JStanleyFX