Talking Points:

- The U.S. Dollar continues to give back post-NFP gains after Friday’s print drove an aggressively volatile day of price action in the Greenback.

- The European Central Bank is the headline on this week’s calendar, and the big question is whether the ECB extends their €80 billion/month bond-buying program here, or later in the year.

- If you’re looking for trading ideas, check out our Trading Guides. And if you want something more short-term in nature, check out our SSI indicator. If you’re looking for an even shorter-term indicator, check out our recently-unveiled GSI indicator.

To receive James Stanley’s analysis directly via email, please SIGN UP HERE

The Dollar’s Slow Burn: Last week’s price action ended with a fairly aggressive day of volatility in the US Dollar. The Dollar first sold off on the initial release of Non-Farm Payrolls, only to reverse in the minutes after. This USD strength lasted for a couple of hours after that bullish reversal began, at which point the Greenback started a slow burn that has continued to drive the currency lower since around 11am ET on Friday morning.

Created with Marketscope/Trading Station II; prepared by James Stanley

Traders looking for directional cues in the Greenback this week may be left wanting, as there aren’t many ‘big’ US data points expected to hit markets. Tuesday brings ISM Non-Manufacturing for the month of August, and later in the day we’ll hear from president of the San Francisco Fed, Mr. John Williams. Wednesday sees the release of the Beige book from the FOMC, and Thursday has initial jobless claims. Friday brings another Fed speaker to markets with Mr. Eric Rosengren of the Boston Fed when he delivers an economic forecast at 7:45 AM ET; and the week closes with wholesale inventories set to be released at 10:00 AM ET on Friday morning.

At issue in the Greenback are probabilities of near-term rate hikes from the Federal Reserve. This Friday’s NFP-miss is likely contributing to some of the back-and-forth price action in the Dollar, with traders caught between the recent uptick in Fed-hawkishness and the continued spate of slowing economic data that could provide the Fed with more ‘room’ to operate before kicking up that next rate hike. With the next FOMC meeting on the calendar for two weeks from now, we’ll likely see markets continuing to try to get in-front of any expected announcements.

Probabilities for an actual hike in September remain below 50%; historically speaking it would be unlikely to see the bank pose a move when so many aren’t expecting it. So the big question appears to be just how hawkish the Fed might be at their September meeting when discussing potential hikes for the remainder of the year. Or, to put otherwise, it appears that markets are expecting a return of last September’s ‘hawkish hold,’ when the Federal Reserve didn’t hike rates, but warned that a hike was imminent.

While last September’s hawkish hold didn’t work out too well for risk markets, the context of the situation was markedly different than present day. Last September saw global markets still on their heels after fear had engulfed global markets after China’s ‘Black Monday.’ This left many feeling exposed, so much so that the Fed had to back off of an interest rate hike that they’d been plotting for months (and for some Fed members, years). The initial excitement of the no-hike announcement saw quick gains rush into equity indices, but as the Fed transmitted a hawkish stance for later in the year with eyes on a hike in December, risk aversion came back and stocks continue to sell-off. And this risk aversion lasted all the way until the end of the month, when a chorus of Fed speakers sang a dovish tune that finally allowed for support to come in to stocks.

On the chart below, we’re looking at the S&P 500 since last September’s hawkish hold (on the left side of the chart). This highlights the big difference between the situation that the Fed is looking at between this September and our last one:

Created with Marketscope/Trading Station II; prepared by James Stanley

Does this mean that the Fed will hike; no. But it does mean that one of the big risk factors that they were afraid of last September is no longer as large of an issue. Last September, the Fed backed down because of weakness in global markets highlighting fragility of the U.S. recovery. But this September, the S&P 500 is sitting near all-time-highs, after having just shrugged off the risk from the Brexit referendum.

This opens the door for the Fed to go considerably more hawkish, even in the event of a no-move decision. Timing is of an issue, as another risk factor may be lurking around the corner with U.S. elections. And while the Fed is supposed to remain apolitical, it’s also their job to steward the economy based on potential risk factors and, frankly, the current U.S. election cycle appears to be the epitome of a ‘risk’ for global markets. The next Fed meeting is in November, just one week ahead of the election, so a hike here probably isn’t likely. But December could be an opportune time for the Fed to pose a move a move on rates, and we’ll likely hear how aggressively they want to move forward at their next meeting in two weeks.

Another Central Bank will take the spotlight this week with the European Central Bank. The ECB launched a gargantuan stimulus program in March, so it’s not likely that we’ll hear any big, fresh announcements as the bank is still in the process of seeing if those measures are carrying much impact. The bigger question is what the ECB may do with their €80 billion-per-month bond-buying program that’s set to expire at the end of March 2017. It’s almost a foregone conclusion that this program will be extended, but the big question is whether the ECB does that here or whether they wait until December. The logic behind waiting would be to save as much ‘dry powder’ as possible in the event that the ECB needs to address another bout of risk aversion should the situation arise.

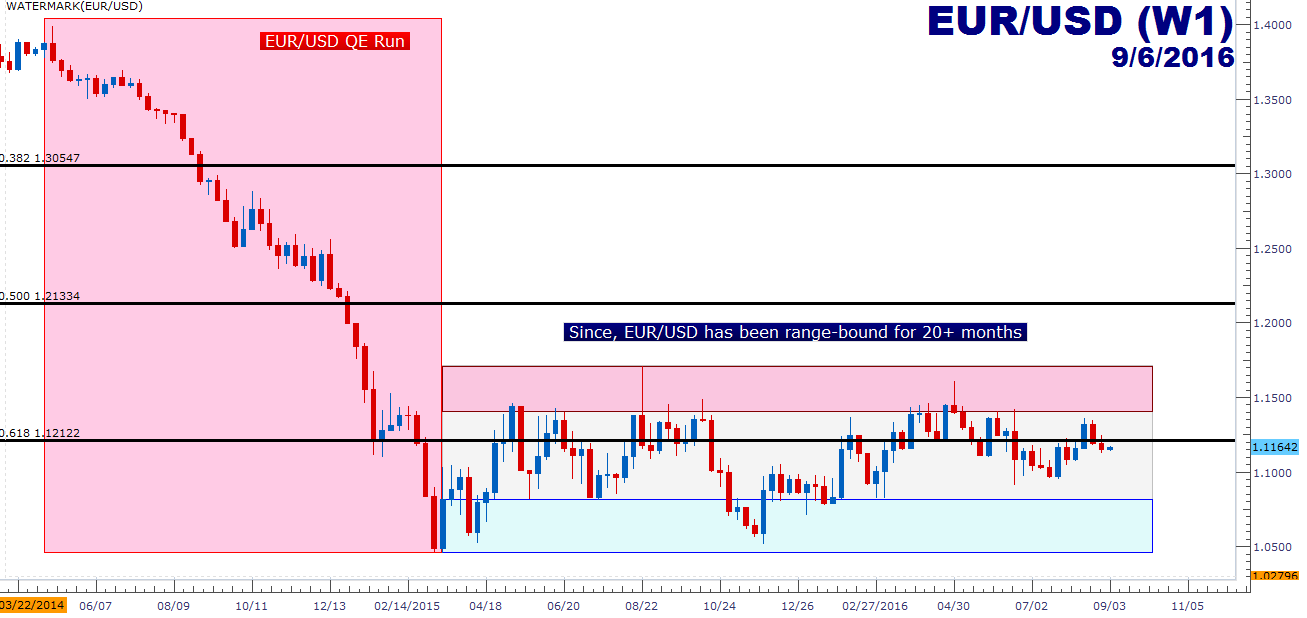

But for all of the excitement between the European and US economies over the past few years, EUR/USD has been relatively range-bound for the better part of the last 20 months. EUR/USD drove lower after the initial announcement of European QE in summer of 2014; and after this 3,000+ pip down-trend ran into a batch of support around 1.0500 that the pair has yet been unable to break. On the flip-side of price action has been the persistent resistance that’s built-in around the 1.1400 handle on the pair. For traders looking for a turn of momentum these would likely the barrier levels that they’d want to watch to look for that directional break:

Created with Marketscope/Trading Station II; prepared by James Stanley

--- Written by James Stanley, Analyst for DailyFX.com

To receive James Stanley’s analysis directly via email, please SIGN UP HERE

Contact and follow James on Twitter: @JStanleyFX