Talking Points:

- Minutes from the July FOMC meeting were released yesterday, and despite a slightly-hawkish tint, the US Dollar continued to sell-off on the expectation that the Fed will continue to be passive in the face of messy data out of the United States.

- This furthers a theme of markets expecting the Fed to remain passive despite their hawkish pleas; and of recent, these hawkish claims appear to be bringing a diminishing marginal impact to USD price action.

- If you’re looking for trading ideas, check out our Trading Guides. And if you want something more short-term in nature, check out our SSI indicator. If you’re looking for an even shorter-term indicator, check out our recently-unveiled GSI indicator.

To receive James Stanley’s analysis directly via email, please SIGN UP HERE

Meeting Minutes from the Federal Reserve’s July rate decision were released yesterday, and similar to the scenario from April/May, the minutes showed a slightly more-hawkish read from the bank regarding near-term rate hikes. The minutes suggested that a rate hike could be possible as early as the bank’s next meeting in September, but many members of the Fed weren’t convinced that a rate hike was necessary in July as they lacked confidence that inflation was on track to meet the bank’s 2% target. This comes fresh on the heels of two different Fed members talking up the possibility of a move next month as both Mr. William Dudley and Mr. Dennis Lockhart had pointed to September for the bank’s next potential move in the build-up to yesterday’s release of July Minutes.

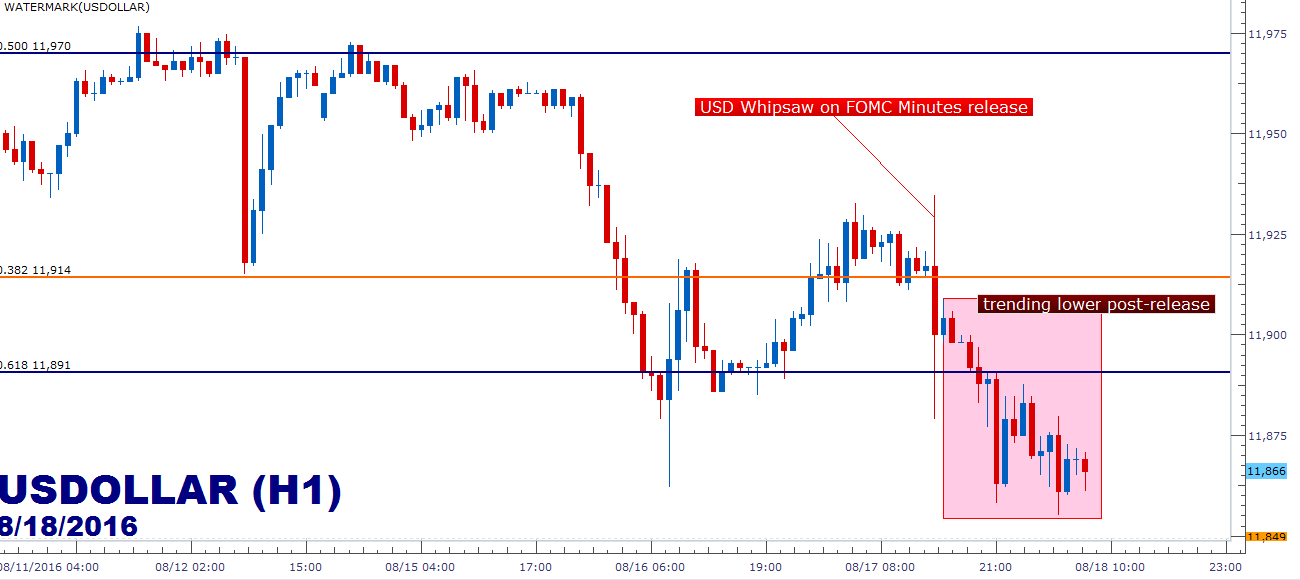

Despite all of this, markets are continuing to expect the Fed to display the same pattern of passiveness that they’ve become well-known for after eight years of ‘emergency-like monetary policy.’ Ahead of the Minutes release yesterday, probabilities for a rate hike in September were at 12%, while December was at 50%. After the release of those minutes, the probability of a hike in September rose to 18%. But this didn’t last for long, as rate expectations have continued to edge lower in the aftermath of the release, with September now clocking-in at 15% with December edging lower to 41.7%. And as those rate expectations edged lower through the Asian and European sessions, the US Dollar fell along with them:

Created with Marketscope/Trading Station II; prepared by James Stanley

This is what’s different from the April/May Minutes release; as the warnings from the Fed that markets may be ‘underpricing’ the probability of a move at the bank’s next meeting had prodded a fairly significant bout of USD strength through May, but thus far, have failed to inspire much strength in the Greenback after the same claims at the July meeting.

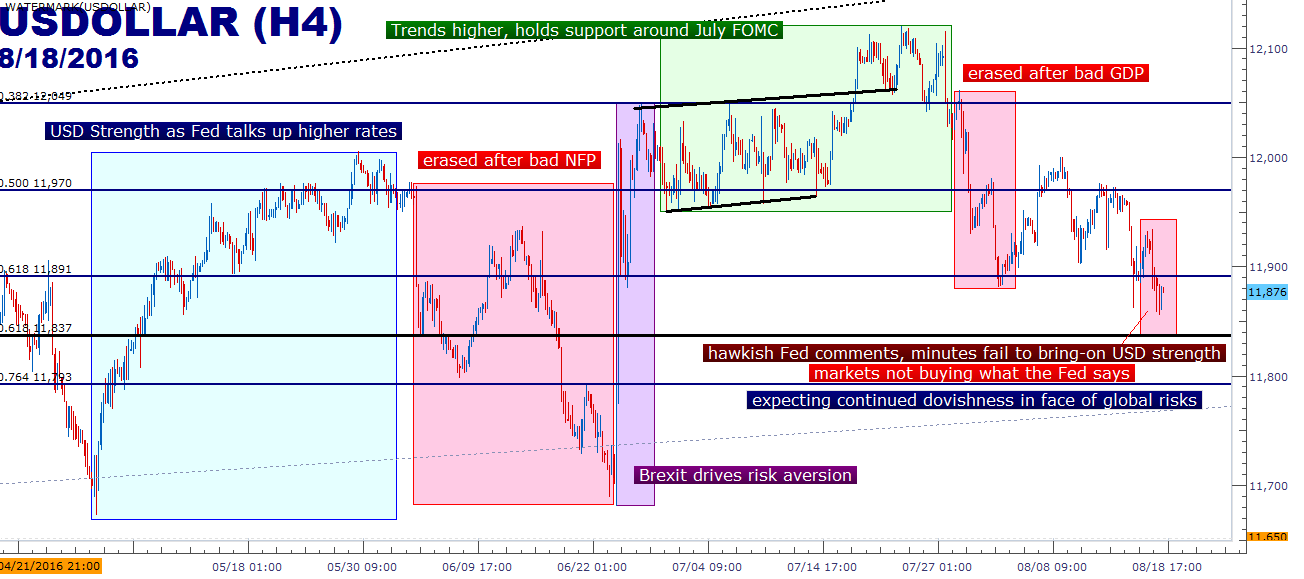

Divergence in expectations between markets and Federal Reserve policy is surely nothing new, but of recent, the Fed’s claims towards tighter monetary policy have begun to bring a diminishing impact in markets, as market participants are becoming increasingly convinced of the Fed’s pervasive dovishness despite their display of persistent hawkishness. On the chart below, we’re looking at the 5+ year up-trend in the US Dollar, and this was largely driven by expectations of the Fed eventually hiking rates in 2015.

Created with Marketscope/Trading Station II; prepared by James Stanley

Much of the choppiness in USD that’s developed since the early part of 2015 has been driven by market expectations around Fed expectations (a tricky prospect, to be sure); with market participants trying to look for clues in offbeat Fed commentary or interviews, or data releases or economic reports, all in the effort of gleaming when that next potential move from the bank might take place.

Coming into 2016, the Federal Reserve had expected as many as four full rate hikes in the year. This was aggressive, even for the rosiest of economic projections, especially when considering the slowdown being seen in China, and the carnage that was being seen in Oil prices. And shortly after the open of the New Year and just a couple of weeks after the Fed’s first rate hike in over nine years, global markets began to sell-off with aggression.

This pain lasted for six weeks until Chair Yellen testified in front of Congress for her twice-annual Humphrey Hawkins testimony and displayed a dovish tone that seemed to pacify markets as support came-in to key areas of equities, Oil, and various commodities. This helped to alleviate the fear that the Fed was going to try to push through a full four rate hikes in the year despite the global risks that continued to flare. On the chart below, we can see that brutal reversal in the Green back that saw eight months of gains erased in February, March and April of this year.

Created with Marketscope/Trading Station II; prepared by James Stanley

This price action led all the way into May, at which point the Fed began to talk up higher-rates, again, pointing to a potential hike in June. In short order, traders began to re-buy the Dollar as rate hike expectations edged higher throughout the month, but that all came crashing down on June the 3rd when Non-Farm Payrolls printed a shockingly-negative figure of +38k jobs added versus an expectation for +160k.

Since then, the Brexit referendum provided a quick-pop of strength into the Greenback on risk aversion fears, and as NFP has come-in extremely robust over the past two months, leading to a continuation of strength in the US Dollar. But after GDP printed far-below expectations, traders, again, faded out that probability of near-term rate hikes out of the Federal Reserve.

Created with Marketscope/Trading Station II; prepared by James Stanley

So, despite what the Fed says regarding the tightening of monetary policy, markets do not seem to be buying this theorem regarding near-term rate hikes, especially for September. But perhaps more to the point, the Fed appears to be losing some element of firepower with fears around future rate hikes. In the prospect of normalization lies the risk of creating reverberations through a fairly contorted bond market that’s been driven to new highs after 8+ years of accommodation and low rates. This is what had led to the ‘taper tantrum’ a few years ago as QE was coming to an end.

So, while September may not bring a rate hike, get prepared for the Fed to try to incrementally ramp-up the hawkishness in order to prepare markets for a potential rate hike later in the year, likely after the election in December. The bigger question is whether markets will listen and respond, or whether they’ll continue to expect passiveness from the world’s largest national Central Bank in the effort of keeping asset prices elevated.

--- Written by James Stanley, Analyst for DailyFX.com

To receive James Stanley’s analysis directly via email, please SIGN UP HERE

Contact and follow James on Twitter: @JStanleyFX