Talking Points:

- The U.S. Dollar continues to show as one of the strongest global currencies, posing a fresh top-side breakout today.

- Given the increasingly-dovish backdrop around the world, unless the Fed offers dovish commentary at their meeting next week, the prospect of top-side continuation in the greenback could be extremely attractive.

- If you’re looking for trading ideas, check out our Trading Guides. And if you want something more short-term in nature, check out our SSI indicator. If you’re looking for an even shorter-term indicator, check out our recently-unveiled GSI indicator.

To receive James Stanley’s analysis directly via email, please SIGN UP HERE

The U.S. Dollar is putting in gains against many major currencies thus far on the morning, with significant moves of strength being seen against Australian and New Zealand Dollars as well as British Pounds.

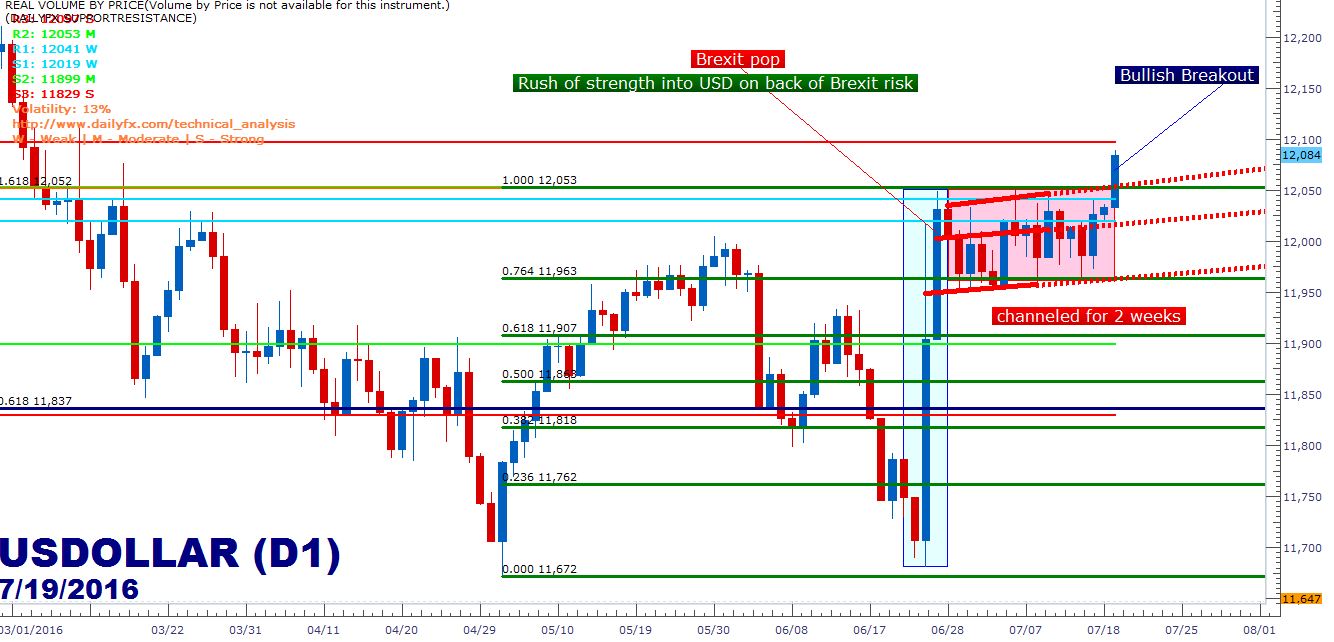

In the two weeks after the Brexit referendum, the U.S. Dollar stayed in a relatively consistent range as represented by the slightly-upward sloping, red channel on the chart below. As risk aversion brought gains into the greenback on the heels of Brexit, support held even as order was restored and equities began running higher again. One of the likely reasons for the continued support and strength in the US Dollar is one-in-the-same as the reason for equities popping higher: The expectation for more Central Bank stimulus out of Japan along with the expectation for more-dovish policy out of Australia, New Zealand and the U.K. There are only so many places in the world for capital to flow, and with each of these Central Banks making nods towards future policy moves that could spell weakness; this has deductively driven capital into USD.

Created with Marketscope/Trading Station II; prepared by James Stanley

This global Central Bank synergy has had a big impact on equities in the post-Brexit environment, seeing fresh all-time highs print on the S&P 500 (SPX500) and the Dow Jones (US30), along with robust post-Brexit rallies being seen in the FTSE100 (UK100) of 16.7%, in French Stocks (CAC40 – FRA40) by 10% and in German stocks (DAX – GER30) of 8.7%. Also of note is the significant move being seen in Japanese stocks as represented by the Nikkei, which has gained 12.4% since the lows after Brexit. As we discussed last week, a recent win in Japanese elections to offer Shinzo Abe’s coalition a super-majority in the upper-house of parliament will likely clear the way for even more stimulus down-the-road, and investors are rejoicing by buying-into the Nikkei in anticipation.

Created with Marketscope/Trading Station II; prepared by James Stanley

Deductive Strength

If major currencies in Japan, the U.K. and Europe are all being driven lower by either dovish policy or the expectation for more dovish policy we will likely see capital flows moving into the US Dollar. This could bring on additional USD strength, but on the topic of continuation potential in the Dollar, another topic of interest presents itself.

With stocks at fresh all-time highs, are we going to see the Fed begin to talk up the prospect of rate hikes in the remainder of the year, specifically pointing to September or December for that next possible rate hike? This wouldn’t be out of the realms of possibility considering the fact that the Fed had attempted to volley expectations for rates higher at their April meeting, when they said that they felt markets were underpricing the probability of a rate hike in June. And throughout May this was very much the thematic message from the Fed; and while this took place we saw stocks temper their 2.5 month rally off of the February lows. And probably one of the starkest turn-arounds was seen in the Gold market. As the Fed began talking up the prospect of higher rates in May, the Dollar surged and Gold retraced more than $100 of its recent $350 gain to find support at the $1,200 psychological level. But as it became obvious that we likely wouldn’t be getting a rate hike in June, and then furthered by risk aversion around the Brexit-referendum, Gold moved right back into its bullish stance and surged to fresh two-year highs.

Created with Marketscope/Trading Station II; prepared by James Stanley

Beware of Another Iteration of the Fed Feedback Loop

With Stock prices at highs, given recent historical patterns we may begin to see the Fed talking up the prospect of higher rates: This refers to the ‘Fed Feedback Loop.’ Given the brutal reaction from markets around recent events such as Brexit, expect the Fed to do this in a rather passive manner, likely by pointing to strength in the American economy at their rate decision next week without committing to anything tangible. After this meeting, the Fed has nearly two months until their next one in September; so this could be an opportune time to give the market slightly hawkish comments while coupled with the dovish global backdrop in order to gauge market response. If we see market sell-off in response to that hawkish commentary, we’ll likely see those potential hikes move right off-the-table (similar to August of last year, or January/February of this year). However, if we see equity markets continuing to find support, the Fed may be able to engineer a rate hike in 2016 (such as December of last year).

The one thing that is clear is that there is an over-arching drive at the Fed to kick rates higher, and this is likely because of the long-term ramifications of ZIRP/NIRP policies. In December of last year, just before the first rate hike in over nine years, Chair Yellen had said she feared a greater possibility of a recession if the bank didn’t hike rates.

What this means: Don’t get too comfortable in long-risk positions as we’re sitting near highs approaching a FOMC meeting. Don’t get too bearish around any one event just yet because we’ll likely see the Fed shift stances in the wake of turmoil in equities. And if we are seeing dovish moves simultaneously from Japan, the U.K. and perhaps even Europe later in the year, there are few places for capital to flow and the US Dollar could be primed for further gains.

--- Written by James Stanley, Analyst for DailyFX.com

To receive James Stanley’s analysis directly via email, please SIGN UP HERE

Contact and follow James on Twitter: @JStanleyFX