Talking Points:

- Stock prices received a boost after yesterday’s speech from Chair Yellen, and it’s looking increasingly unlikely that we’ll be seeing a rate hike out of the Federal Reserve anytime soon (June/July). Since yesterday’s speech, USD has put in bearish price action.

- The prospect of ‘forward guidance’ is relatively new in Fed terms, taking on a more prominent role post-Financial Collapse. Forward guidance has never successfully been used in a rising rate environment, so the bigger question is how markets will contend with forward guidance as rates move higher when the Fed is telegraphing significantly tighter conditions for the quarters/months/years ahead.

- If you’re looking for trading ideas, check out our Trading Guides. And if you want something more short-term in nature, check out our SSI indicator. And if you're looking for something even shorter-term, check out our GSI indicator.

Yellen Speech: Chair Yellen’s speech in Philadelphia yesterday was emblematic for much of her tenure atop the Federal Reserve: She provided a few hints and clues pertaining to future rate hikes without anything very telling, and markets reacted by expecting the Fed to continue to support asset prices as a top priority.

One of those hints that Ms. Yellen gave to markets pertained to last Friday’s NFP report (and includes the previous NFP report as well), when she said ‘New questions about the economic outlook have been raised by recent labor market data. Is the markedly reduced pace of hiring in April and May a harbinger of a persistent slowdown in the broader economy? Or will monthly payroll gains move up towards the solid pace they maintained earlier this year and in 2015?’

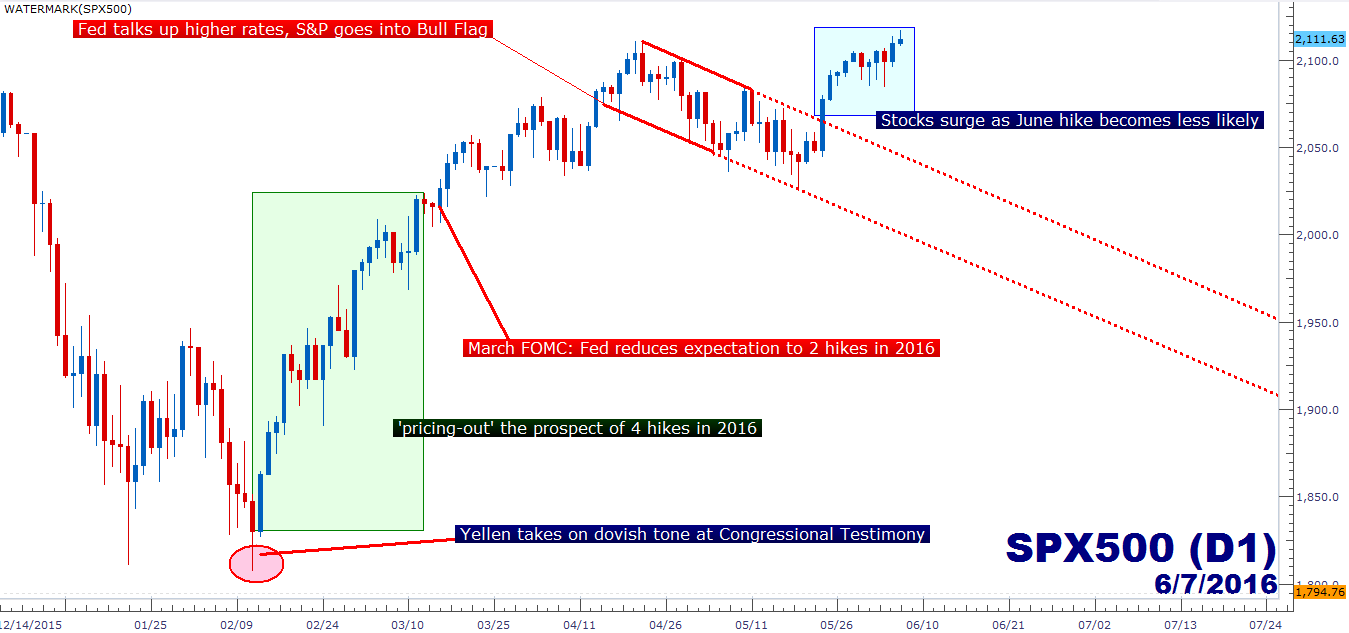

This gives the appearance that the Fed isn’t going to hike until they’re fairly certain that the broader economy can handle the extra 25 basis points. And this was somewhat of the general market consensus as we came into May when rate hike expectations for June were hovering around 5% after a fairly poor NFP print for the month of April. But multiple Fed members throughout the month of May discussed the prospect of 2-3 hikes for the remainder of 2016, and this brought those probabilities for a hike in June back up to around ~30% while the US Dollar put in an extended rally throughout the month.

Created with Marketscope/Trading Station II; prepared by James Stanley

But the bigger question is whether the actual problem is a single 25 basis point rate hike, or if the issue actually stems from something larger; such as telegraphing multiple rate hikes in the future when it took so much effort to enact a single hike last year in 2015. This speaks to the prospect of ‘forward guidance,’ which was thought to be a tool that the Fed could use to provide an additional sense of support to markets. Forward guidance came into play in the early 2000’s but in response to the Global Financial Crisis took on a life of its own as the bank began to use ‘forward guidance’ to assure markets that rates would stay really low for a really long time.

This does a few things for markets, key of which is telegraphing extremely dovish economic policy months and in some cases, years in advance. This means that investors can operate with a greater sense of safety when taking on risk as the expectation is for that representative Central Bank to stick with loose monetary policy. So investors can comfortably acquire stocks as the expectation is for rates to stay low, which makes it easier for many companies to continue operating without the pressure of higher rates, and this provides a sense of semblance for markets as investors can continue buying debt while at extremely low yields as the expectation is for rates to continue to stay low.

But what happens when rates move higher? Rising rates are one of the bond investor’s biggest foes (along with inflation). Because in a bond with a fixed rate of return, those higher rates simply mean that your bond is worth less. If you buy a bond at par with a 3% coupon when the discount rate is at 3%, why would investors want to pay you full price for that same bond after rates move up to 5%? They wouldn’t – you’d have to take a hit on the principal to get rid of that bond.

So rising rate environments are especially unfriendly to bond investors because higher rates mean that a) currently held bonds are worth less in this higher-rate environment and b) the prospect of even higher rates in the future (as rates continue to run higher) mean even more losses down-the-road as your lower-yielding instrument will be even more unattractive in the secondary market as rates continue to rise.

With forward guidance telling investors that rates will rise as many as four times in a single year, you’re basically assuring investors that any long-dated bond purchases will be underwater twelve months from now. This is what the Fed was doing as we came into 2016, and this is why a single 25 basis point rate hike is being so closely watched; it has less to do with this one hike than it might for future policy stance as that ‘especially accommodative’ environment created by the Fed and enjoyed by so many investors may soon be coming to a close.

So, while forward guidance may have been hugely helpful in telegraphing to investors that policy would stay especially loose for a long, long time, using that same forward guidance in an expected rising rate environment, it would seem, is creating considerable pressure for global financial markets as every investor on the planet attempts to get in front of the Fed’s next move.

Of late, forward guidance from the Fed via the Dot Plot Matrix (each Fed member’s expectation for rates in the coming quarters/years) has been a huge driver for markets. After coming into 2016 with the central expectation for four hikes this year, risk markets caved as risk aversion set-in. And after that risk aversion set-in, the Fed dropped that guidance to the expectation for two hikes in 2016 and this functioned as a form of weak stimulus as stock prices shot higher.

Created with Marketscope/Trading Station II; prepared by James Stanley

As we move deeper into 2016 where numerous questions exist as to economic direction, investors need to remain cognizant of the risks. As the Fed begins to talk up higher rates, look for pressure to begin building in risk markets as investors try to get out of the door before the exodus ensues. But while the Fed is talking up a continuation of ‘emergency-like’ policy, risk will likely continue to be ‘on’ to some degree.

--- Written by James Stanley, Analyst for DailyFX.com

To receive James Stanley’s analysis directly via email, please SIGN UP HERE

Contact and follow James on Twitter: @JStanleyFX