Talking Points:

- PBOC Governor Zhou Xiaochuan made comments over the weekend warning of elevated corporate debt levels in China relative to GDP; but an announcement of relaxed Margin Lending rules from China Securities Finance Corp were enough to offset those concerns to bring a continuation of the recent rally in Chinese stocks.

- Data is relatively light this week with the highlight on the calendar being Fed-speak after a dovish FOMC delivery.

- If you’re looking to improve your trading approach, check out our Traits of Successful Traders research. And if you’re looking for trading ideas, our Trading Guides can provide a plethora of longer-term ideas while our SSI Indicator can help with shorter-term and swing-trading ideas.

China has a debt problem, and most of the market is well aware of it at this point. We had written on this topic just a couple of months ago, noting that China’s increased debt-load across the country can make it even more difficult to recover from this most recent bout of weakness. Nonetheless, it was still somewhat surprising to hear such a public admission of vulnerability from a Chinese regulator, as this weekend the governor of the People’s Bank of China, Zhou Xiaochuan, warned that the ratio of corporate lending to GDP had become too high, saying that the country needed to develop more robust capital markets to help offset this concern.

The premise of developing more robust capital markets, either with the Shanghai-Hong Kong Stock Connect or opening up the Bond Market for foreign investors, more freely allows for capital to flow in and out of China. In essence, this would allow for more foreign investors to take on these risks rather than Chinese investors.

The bigger question is whether massive injections of foreign capital would be enough to help the Chinese economy turn the tide. As has been widely noted upon the conclusion of China’s annual conferences and at the 13th Fifth plenum (China’s five-year plan), reform of SOE’s, or State-Owned Enterprises is high on the list of China's to-do items. And one of the big reasons is the inefficiency that will often come from a government-owned business. Just three weeks ago, Bloomberg wrote an in-depth piece on the city of Tonghua, entitled ‘Death and Despair in China’s Rustbelt.’ The article outlines China’s attempt to convert a steel mill that was operated by a SOE to private ownership. This didn’t work out well , and with recent reports to expect up to 1.8 million layoffs as China makes cuts to Coal and Steel industries, this could present considerable volatility moving forward.

And while these risks are very real, and while the warning from Governor Zhou may seem imposing, Chinese stocks put in a strong rally last night with the Shanghai Composite gaining +2.15% while the Shenzhen Composite put in a +2.68% incline. The likely cause for the rally: A State-Owned Enterprise, China Securities Finance Corp, announced that they’d start issuing loans to securities firms to buy stock. Of recent, Chinese stock performance has begun to mirror margin debt levels, indicating that the recent rally in Chinese equities has been debt-driven.

If anything, this should highlight the theme that has basically become a global phenomenon, of Central Banks doing whatever they can to keep markets elevated despite the notable downshift in global economic data. As we’ve been saying for the better part of six months, for those wanting to trade an Asian slowdown, Japan may be a far more attractive venue, with a short Nikkei and Long Yen stance. The Bank of Japan is one of the more stretched Central Banks, and may have decreased flexibility moving forward, and this could make them more vulnerable to a Chinese slowdown than even China.

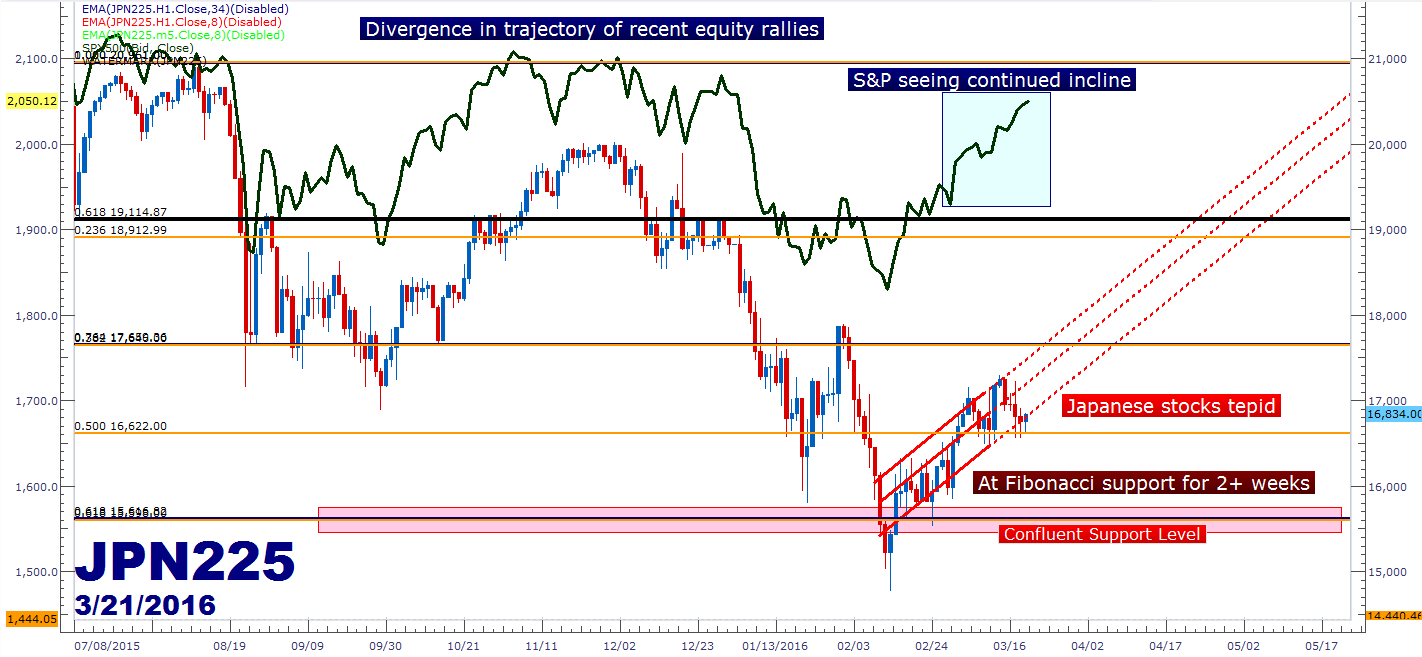

As we had written on Friday, the Yen continues to strengthen as Japan sees even more increasing pressure from capital flows. But perhaps equally interesting at this point is the tenuous rally being seen in Japanese stocks while their Chinese and US counterparts see even more bullish price action.

On the chart below, we’re looking at the Nikkei with the S&P overlaid (in green). Notice that the past two weeks have seen differing trajectories in these assets, with the notable difference being that Japanese stocks continue to meander near Fibonacci support while US Stocks continue to be strongly bid. The current level of support on the Nikkei is the 50% Fibonacci retracement of the move from the June 2013 low to the high from last year (shown in orange on the below chart).

Created with Marketscope/Trading Station II; prepared by James Stanley

--- Written by James Stanley, Analyst for DailyFX.com

To receive James Stanley’s analysis directly via email, please SIGN UP HERE

Contact and follow James on Twitter: @JStanleyFX