Talking Points:

- Many global indices have continued higher into resistance points. Heavy data is on the docket for the next two weeks, and this will likely determine whether stocks rip or dip.

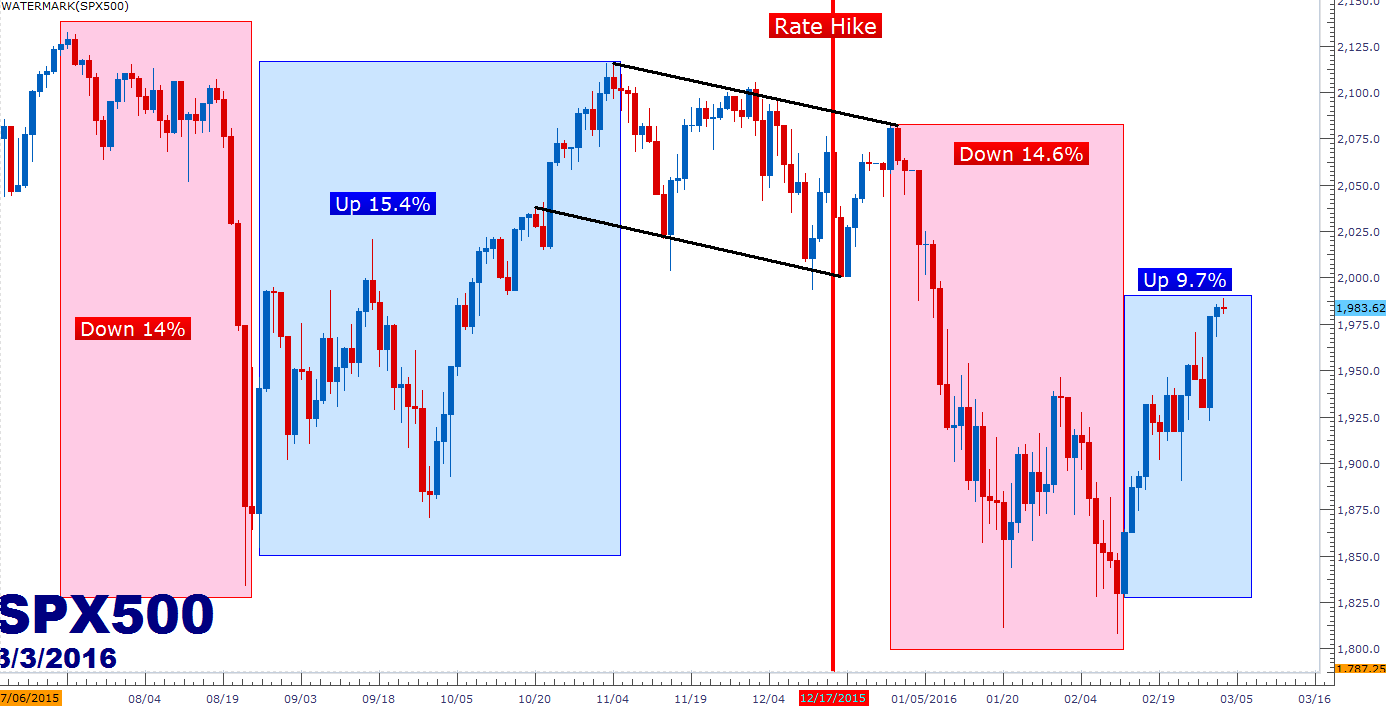

- The S&P has moved up by 9.7% with the Nikkei up 14% and the DAX up 12% in the three weeks since Ms. Yellen’s Congressional testimony; deductively highlighting how monetary policy is likely the primary focal point for markets at the moment.

- With FOMC in two weeks, and with NFP set for tomorrow, fully expect attention to be drawn to US data and policy remarks for cues on risk trends.

- This is a volatile market on both sides. If looking to traverse these terrains, traders should make sure to address risk management, as the one thing that a trader can be sure of is that they will, at times, be wrong. Make sure one bad trade doesn’t wipe away the gain from 7, or 8 winning trades.

Stocks Temper Gains Ahead of NFP: The ebullient stock gains over the past three weeks have created a significantly different picture for the global economy in a really short period of time. Three week ago, when Ms. Yellen began her second day of testimony in front of the Congress, global equities were looking to be in a very precarious position. This was the week that China was closed, yet stocks were still throttling to new short-term lows. Fears of global recessionary fears were fanning across markets after a brutal opening to February followed a brutal first three weeks of January.

But something interesting happened during that Congressional testimony: Ms. Yellen took a slightly softer stance towards the topic of negative rates than she had the day prior; and markets apparently took this as a dovish signal that the Fed would likely avoid any further 2016 rate hikes as rate hike expectations for the remainder of the year got completely priced-out of markets, and in-turn, risk assets rocketed higher. And while there have been a couple of points of resistance on the way higher, for most intents and purposes we’ve seen extremely strong moves across equities, in many cases with those hardest hit shares rebounding the most.

Since the pre-Yellen lows, we’ve seen a nearly 10% run in the S&P 500 (9.77%), a 14% run in the Nikkei (JPN225), and a 12% bounce in the DAX (GER30). And this is all in that three week period that began as Ms. Yellen was in day two of that Congressional testimony. These are big numbers, to be sure; and these are the types of events that can often get folks to change their biases or approaches in a market. The chart below illustrates some of the volatility that we’ve seen in the S&P 500 over the past six months.

Created with Marketscope/Trading Station II; prepared by James Stanley

But does the most recent bump in global equity prices mean that we’re back off to new highs? Not necessarily. As a matter of fact, increasing volatility in a market is often indicative of a turn or, at the very least, volatile congestion. After an extended bull run (or bear run for that matter), much of the market gets loaded-up on one side. This is why the trend is usually your friend, and why you usually want to trade in the direction of the general bias. But as we near a turning point, we see an increasing number of sellers (which leads to price movements lower). This isn’t likely to lead to a linear movements lower after an up-trend, as there are still folks looking to buy in the direction of that previous bias.

As an illustration and recent historical example, the Financial Collapse gyrated for ten months before we saw capitulation. The writing was on the wall, the fundamentals were bad and the environment was toxic for those ten months. Moody’s hit the initial wave of downgrades on Mortgage debt in July of 2007 and we saw the S&P make a new high just three months later. Again, writing, walls, etc. Perspective is a pretty important thing to a market practitioner. The S&P didn’t capitulate until the bulls chasing the previous up-trend submitted and stopped trying to buy.

Notice that there were plenty of bumps higher on this down-trend shown on the chart below. Increasing volatility often shows up at the top or bottom of a move, and you can see this on both sides of the Financial Collapse.

Created with Marketscope/Trading Station II; prepared by James Stanley

But Does This Mean a Collapse/Global Recession is on the Way?

I’m going to be straight up with you: I don’t know, and I’m fairly confident that nobody else in the world ‘knows’ for a fact what will happen. Few saw the Financial Collapse and even fewer saw the Tech Bust of the S&L snafu of 1987. Human beings can’t tell the future and are notoriously bad at forecasting. We’re riddled with observation biases and fight-or-flight impulses that work against us at almost every turn. Anyone that acts as though they know what tomorrow holds is likely being either intellectually disingenuous or is horribly misled. In either case, you probably want to be careful of listening to such a resource.

This is one of the reasons you’ll see so many charts in my work, because in over 16 years of following markets it’s one of the few things that I’ve found that ‘works.’ And by ‘works,’ I mean it strips out the superfluous minutiae that much of the world gets myopic around to instead focus on the one thing that truly matters: Price. Banks, despite the public hatred, are pretty good at what they do. They’re generally not that stupid, so if something ‘good’ happens or if something ‘bad’ takes place, they’ll generally respond with their positioning because they aren’t in the business of losing money. This is why price action is so widely followed by professional traders.

This means prices will move to reflect that increased supply or demand, and, in-turn, will reflect the state of market participants’ current stance or position on a market. And while the near-10% run over the past three weeks is very attractive, it’s still far too early to say definitively that the pain from the beginning of the year is over yet.

But if we deduce drivers and likely causes or pressure, what can determine the near-term directional stance in the S&P 500? This likely goes right back to the Fed, as it was the beginning of day two of Ms. Yellen’s Congressional testimony that set the lows. And this was the market running with the theory that the Federal Reserve may not hike rates for the remainder of 2016.

But this isn’t the first time we’ve seen such a scenario, is it? The world had widely accepted that a rate hike was coming as we neared the September FOMC meeting last year, but when the Fed backed down for fear of global pressures and as Fed members talked up the idea of ‘looser for longer,’ stock prices found support and moved higher. This is what led to the December rate hike. The same risks we have today were here in December, just as they were in January and February. The environment is the same. The difference is a 10% bump.

Whether or not this continues will likely be based around that prospect of further rate hikes. We hear from the Fed in two weeks (March 15-16), and this is where we can get an update on the dot plot matrix, inflation projections and expectations for further rate hikes. The prospect of a hike at the March meeting is extremely minimal at the moment, but the guidance offered will likely become the next ‘driver’ for markets.

But until then – expect even more onus to be sent towards US data. This puts even more emphasis on US data because if strength is seen in these prints, particularly on the employment front, the Fed may find it difficult to refrain from tightening policy. This may sound outlandish given the state of the global economy just three weeks ago (meant tongue-in-cheek given the equitability of stock prices to actual underlying economic performance), but if we go back to the fourth quarter of last year this is exactly what happened.

This is the Fed’s negative feedback loop: Markets go down and they get dovish (like we saw three weeks ago), and then markets go back up and they get hawkish, which then brings markets back down. And this type of grind can take place for a long time, just as we saw in 2008 before capitulation took place.

--- Written by James Stanley, Analyst for DailyFX.com

To receive James Stanley’s analysis directly via email, please SIGN UP HERE

Contact and follow James on Twitter: @JStanleyFX