Talking Points:

- The Federal Reserve rate decision for January is issued at 2PM this afternoon, and there is little chance of a hike here. But more interesting will be the details inside of the statement, and the Fed’s expectations for rate hikes for the remainder of the year.

- There are major risk factors in the global economy right now that the Fed has to contend with around these rate decisions. In a special report last night, we discussed the threat of a credit bubble coming to roost in China, and we’re nearing a point where movements in Oil prices are being driven more by panic and fear than supply and demand, and that’s a dangerous thing.

- If trading around the news this afternoon (or ever, really), risk management needs to be addressed. Check out our Traits of Successful Traders to see what’s worked for others and what hasn’t. And if you’re looking for markets that might be ‘stretched’ and opportunistic, check out our Real-Time SSI indicator.

We’ve already produced some significant coverage to preview FOMC this afternoon. My colleague Christopher Vecchio discussed that in his morning piece, and David Song will be publishing a piece right before the meeting takes place at 2PM. So rather than re-hash what these gentlemen have so eloquently already said around today’s meeting, I wanted to provide a primer with some context on what to look for this afternoon.

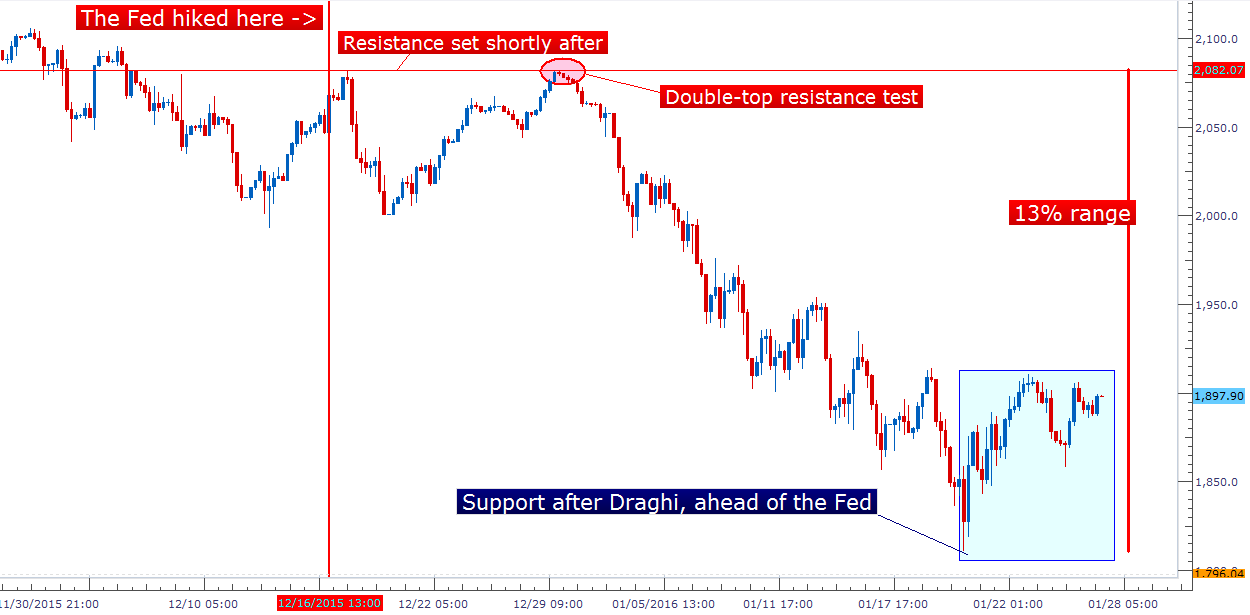

There is practically zero chance of a hike at this meeting, but more pressing will be the Fed’s outlook for the rest of the year. This has been a huge pressure point of recent, as the Fed’s expectation for four rate hikes in 2016 is the likely scourge of this most recent bout of risk aversion. After the Fed hiked in December, we said the road was long. That road got significantly bumpier in the two weeks following, and with the open of the New Year, matters materialized very quickly as Oil moved from $37.50 to $27.53, and China began to see massive sell-offs in their equity markets (again).

Created with Marketscope/Trading Station II; prepared by James Stanley

So, the case can be made that we’re looking at a significantly different environment than we were just a month ago. The big question is how the Fed sees this, and how this may impact their rate hike plans for the remainder of the year.

If history is any guide (which it sometimes is), then investors might expect the Fed to take on a dovish tone this afternoon, denoting that the increased risks in the global economy warrant caution and attention. If this happens (as it has in the past), then risk assets will likely rally as investors get the feeling of another gust of wind from the Federal Reserve behind the sails of the market. This is how matters have developed over the past six years… This is why ‘bad was good’ on the data front – because the worst the data was, the higher the probability of more Central Bank support. So bad was good, and good was technically ‘bad’ as this meant less support from the Fed; but in most cases it wasn’t really that ‘bad’ because good data was, at the very least, evidence of ‘recovery.’ This is a pretty distorted environment, isn’t it? This is just another consequence of ZIRP. And one can make the case that this is a positively-biased feedback loop going on in markets, influenced by the Fed.

If data was bad, it’s ok – more support is coming. If data was good, eh, well at least we’re recovering. This is why stock prices ran to all-time highs while inflation was non-existent, because low rates compelled investors to take on more risk than they normally would in the search for return. And as long as things kept growing and as long as markets kept moving up, that’s really no big deal. But prices don’t always move up, do they? What happens when investors have a legitimate and viable reason for risk aversion?

A Market build on stimulus - Every theme of risk aversion over past seven years has been offset by more QE or dovishness from the Federal Reserve.

Chart created with Marketscope/Trading Station II; prepared by James Stanley

This is precisely what happened in 2008 in mortgages. Excessive risk was taken on because of the perceived safety of the asset class (CMO’s) and as long as home prices kept growing, all was well. But once home prices moved down, those levered-up portfolios felt the pain. And that led to a domino effect of selling. The problem we have now is that the elevated asset prices aren’t just in real estate. It’s in the S&P, and that means it’s in most American 401k investors’ portfolios.

The Fed took a lot of blame for the housing bubble in 2008, in the fact that they were slow to raise rates as home prices were going ballistic. And this is really just a result of the tech bust, in which we had the first instance of ‘historically low rates’ as the Fed took rates from 6.5% all the way down to 1% (in 2003-2004) in the effort of re-invigorating the economy after a massive bubble had burst. Those 1% rates eventually worked. Buying a home was never more attractive, and demand for homes pushed up prices to the point where ‘flipping’ real estate became a thing. Many were quitting their regular jobs so that they could speculate on the real estate market, not too different from how many were quitting their regular jobs to become day traders only a few years earlier (before the tech bubble collapsed, of course).

After the housing bubble burst, the Fed did the same exact thing in taking interest rates down to ‘historically low’ levels, and nothing has changed for seven years; that is, until December. So this is why where we’re at now is so utterly important: This isn’t just near-term home or stock prices, we’re seeing a market that’s still carrying the baggage from two very recent and two very severe bubbles bursting within the last 16 years. Asset prices are elevated, that can’t even really be argued with. The big question is whether Ms. Yellen will take a Paul Volcker-like approach in instituting tough policy for the betterment of the long-term prospects for the American economy, or whether she will yield to near-term pressures after stock markets shaved of 13% of these elevated levels.

Chart created with Marketscope/Trading Station II; prepared by James Stanley

Nobody knows for certain how this will play out because the world has never seen such a situation and there’s simply nothing to compare this to. This is just further reason for risk aversion, because we may be nearing an area where the Fed can’t offset global weakness because the Fed ran out of firepower and can’t combat a bigger-picture credit meltdown in China, or continued pain in Commodity prices (which appears to be bringing in credit risk into the United States).

What we do know is that asset prices are elevated by most historical metrics, selling has already begun as risks in Asia and commodities have risen, and the Fed runs the risk of creating an even larger bubble if they continue the pattern of dovishness that’s brought us to such elevated levels in the first place.

At 2PM today, we’ll get our next clue as to the direction that Ms. Yellen and the Federal Reserve want to take this.

--- Written by James Stanley, Analyst for DailyFX.com

To receive James Stanley’s analysis directly via email, please SIGN UP HERE

Contact and follow James on Twitter: @JStanleyFX