Talking Points:

- The Nikkei moved into ‘official’ bear market territory with a 20% drop from the highs. But Germany and China are already in ‘bear markets,’ and we may be seeing the US join that camp in the coming weeks.

- The driving pain factor here appears to be the Fed. Fed members have already shown brief signs of backing down from the 4-hike in 2016 mantra, but risk aversion has continued. We’ll likely need a more aggressive statement or set of statements from the Fed for fear to recede.

- Bigger-picture, the prospect of forward guidance is a threatening one, especially in a rising rate environment. This may be too much information for markets to handle. During ZIRP, forward guidance is stimulus. In a rising-rate environment, forward guidance is undue fear of tightening.

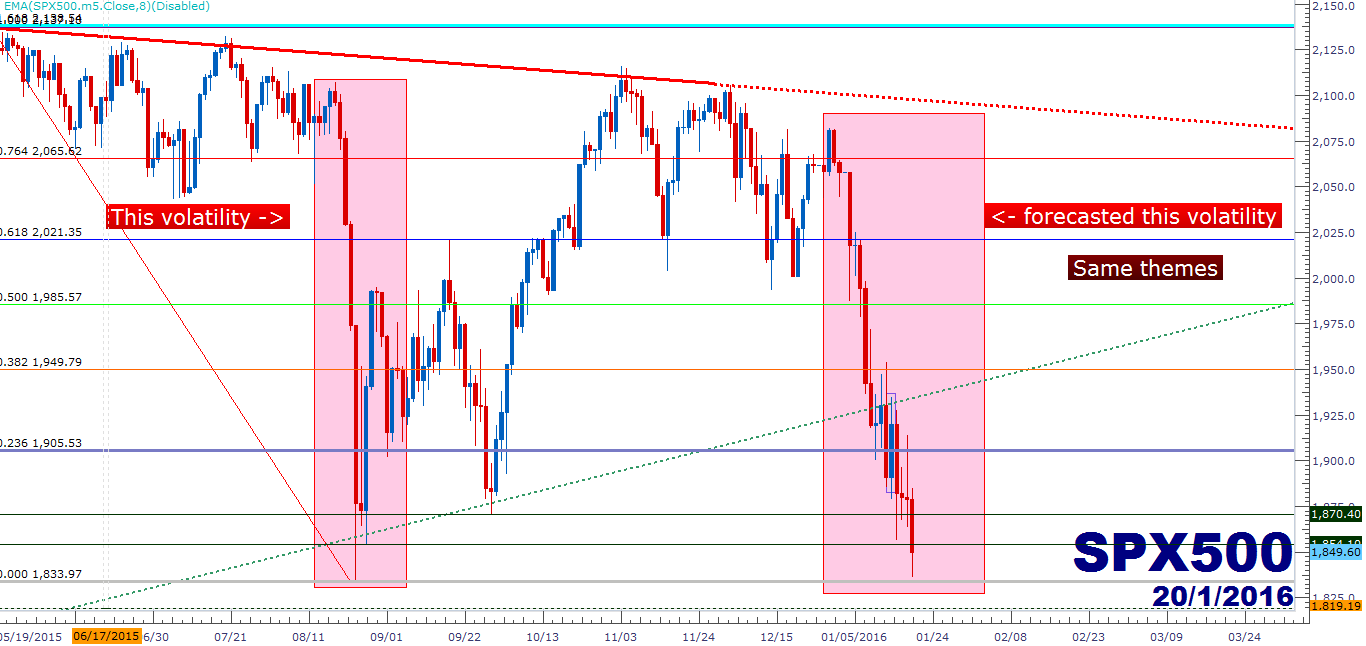

It’s been a dizzying year for stock markets around the world, and we won’t waste your time recanting the fallen. If you’d like to read about it, you’re more than welcome to check out our piece from yesterday in which we discuss China; or you can read our piece from last week, in which we discussed how the favored ‘buy the dip’ strategy that had became commonplace with Federal Reserve support behind equity markets has recently become ‘sell the rip,’ as investors get more risk-averse after the Fed’s taken on this hawkish, rate-hiking path of monetary tightness. The big headline on the morning is the fact that the Nikkei just dropped into ‘bear market’ territory, denoted by a drop of 20% or more from the highs. We’ve been talking about the strategy of using Japan to trade the slowdown in China, and this was a Central part of our Q1 forecast for equity markets. With this drop in Japan, we’ve come extremely close to my third and final target on the setup. But after seeing such aggressive moves seen so quickly, I’m going to add an additional target at the previous low of 14,353.

Created with Marketscope/Trading Station II; prepared by James Stanley

If you do want background:

If you’d like the ‘big picture’ look at what’s going on, we had outlined the situation to end 2015 in our three-part series, The Top 3 Themes Facing Markets as We Approach 2016. In the first part, we looked at China and how the potential for a deeper slowdown in the country could potentially drag the rest of the continent with it, and should Japan get snared into another recession, their already-vulnerable economy stands to take some massive hits after three+ years of QE have been unable to stem the deflationary tides. In the second part, we looked at the carnage in commodity prices and how, eventually, this would bring some dire effects to economies around the world as lower commodity prices spelled, essentially, deflationary impacts that corporates around the world would have to contend with in the coming months. And in the 3rd part of that series, we looked at the elephant in the room and the one thing that would likely trigger the previous two situations into an untenable state: Interest Rates.

The reason for pointing all of this out, other than to give you a primer and a background on the current situation, is to highlight the fact that none of this is news. We’ve known that China has been slowing down for a while, and commodity prices have been dropping for the better part of two years now (four or five depending on the commodity you’re looking at); but the changing factor that appears to be the driver behind this pain is the insistence of the Federal Reserve to a) kick up interest rates at a time when the rest of the world can’t really bear it and b) sticking to this expectation for four rate hikes in 2016, i.e., overly aggressive forward guidance that has markets freaked out.

It may be hard to believe, but there was actually a time when the Federal Reserve didn’t give forward guidance, and markets operated just fine. As a matter of fact, there was something to be said about the Federal Reserve keeping some data to themselves. Investors had to remain on their toes because they didn’t want to be on the wrong side of a rate play when Greenspan was delivering actual news that markets didn’t know was going to happen. Forward guidance was rolled out in desperation during the Financial Collapse as Central Bankers threw any idea against the wall that might work. The thought that telegraphing to markets that rates would stay ‘super-low, for super-long’ was thought to be a form of stimulus in-and-of-itself because, after all, they’re telling the markets very loudly ‘we are not going to raise rates on you, so go take on risk.’

But with rates moving higher – this stimulus from forward guidance is no longer really stimulus at all, is it? It’s a threat, more or less, and not only that – it’s a threat that markets never really bought. The Fed insisted on the expectation for four rate hikes in 2016 ever since the rate hike, so if it wasn’t the rate hike that freaked markets out, it would almost certainly be this expectation for four more in the calendar year of 2016. This is likely why China has recently taken on an aggressive stance towards speculators with the volatile adjustments to HIBOR rates. But the fact that markets are second-guessing the Fed, and aren’t fully pricing in the Fed’s expected rate hike schedule brings up a far more troubling question: Is the World losing confidence in the Federal Reserve?

Created with Marketscope/Trading Station II; prepared by James Stanley

But these are facts that aren’t really up for debate: China is slowing, commodity prices are dropping like a rock attached to an anvil, and the Fed is looking to aggressively hike rates. As we’ve deductively outlined, given the fact that China/Asia slowing down and commodity prices coming off ‘aren’t really news,’ the one factor that’s changed over the last month in financial markets has been the Fed and the fact that they actually kicked rate higher whereas that scare had receded in August/September. And now that the risk-off move is becoming well-entrenched, what could potentially turn these trends around?

What Could Reverse this - Watch for the Fed – and Expect More Activity

This isn’t the first time that markets have sold off on fear of the Fed. We had similar such instances in during the Taper Tantrum in 2013 and again during the ‘mini’ taper tantrum of 2014 – but both of those situations were offset by smooth Fed language. In both situations, risk aversion was picking up as the Fed began and finished winding down their most recent allotment of QE purchases. The thought being, without the Federal Reserve support that markets had become accustomed to and markets would be vulnerable to a litany of risks (two of the main ones we’ve already listed). But in each situation, Fed members gave interviews and commentary that alluded to ‘looser for longer.’ Eventually, support came back to stocks and they kept doing what they had been doing (moving higher).

After the hike in December, the Fed stuck to their rather aggressive expectation for four hikes. We discussed this last week in the article, Stocks Still Falling, Fed Still Talking: Higher Rates a Harsh Reality. Within an hour of publishing that, the man considered to be the most hawkish member of the Federal Reserve, Mr. James Bullard, provided some shockingly dovish commentary (basically he always voted for rate hikes and now he’s backing down). He mentioned how the drop in oil was noteworthy for the Fed, and it could actually impact the rate hike schedule. This is the same type of thing that turned around risk aversion during the taper tantrums of 2013 and 2014, and for the early part of last Thursday – it looked like Mr. Bullard’s commentary may have ‘worked’ as stock markets started going back up again. But that didn’t last… sellers merely used that bump higher to sell-in at better prices. We discussed the reaction to Mr. Bullard’s commentary in the Market Talk last Friday.

Created with Marketscope/Trading Station II; prepared by James Stanley

We discussed this the morning after the Fed hiked in the article, Rates are Up but the Road is Long.

But while this may not have ‘worked’ this time, this does show the Fed’s hand. Just like we saw in September of last year, if risk aversion is heating up the Fed will back down. And if risk aversion is really heating up outside of a meeting, then we’ll likely see Fed members in financial media talking about fewer than four rate hikes this year.

But given the reaction that we’ve seen around the world so far this year, it may take more than just a few interviews to turn this thing around: We may need to hear official Fed language towards their rate hike schedule or expectations for 2016 before we can get some remission in this recent bout of risk aversion.

And perhaps even bigger than that – we may need to see a re-engineering of the way that the Fed is handling this situation: Forward guidance appears to have become a major drag for these efforts because, even if the world could bear a 25 or 50 basis point rate hike out of the Fed, the prospect of four more hikes over the next 12 months is an extremely aggressive picture for investors to bear. And should the situation turn sour, there are numerous questions as to whether the Fed even has the firepower to do another round should that be required.

Nobody knows how this whole situation will pan out and that’s just another reason for investors continuing to sell risk assets. Neo-Keynesian economics is facing its most difficult and toughest test yet: Stock prices are still extremely elevated by most historical metrics, and it’s obvious at this point that those valuations are because of QE-driven asset flows: The big question is, what is ‘fair value’ in an honest world without a constant spigot of liquidity coming from Central Banks. And that’s what markets are attempting to discover right now.

But this pain is not relegated to Japan and the United States. We hear from another Central Bank tomorrow when the ECB delivers their rate decision for January. After the ECB disappointed markets in December after previously stoking hopes for an increase to QE, equity markets out of Europe have went into a near-collapse-like mode. The Dax is currently testing those lows from September, and is currently off 23.6% from the highs set back in March of last year (ironically enough, this is when European QE began, and German stocks have only moved lower since the actual program has been at work).

Should the ECB fail to speak to an increase in QE or any surrounding details tomorrow morning, and we can see some additional pain in European equity bourses. The chart below looks at the DAX, and offers a few different levels of interest for the next two trading days:

Created with Marketscope/Trading Station II; prepared by James Stanley

--- Written by James Stanley, Analyst for DailyFX.com

To receive James Stanley’s analysis directly via email, please SIGN UP HERE

Contact and follow James on Twitter: @JStanleyFX