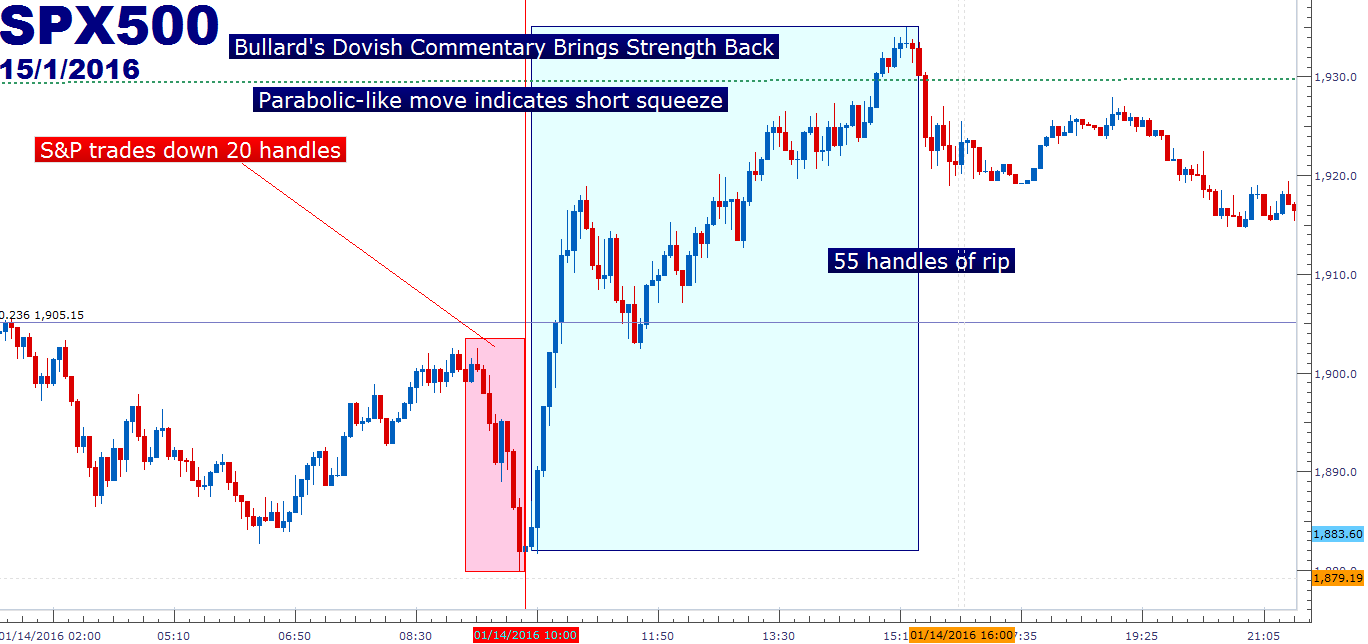

- Yesterday saw a jaw-dropping short squeeze in stocks after James Bullard of the St. Louis Fed (often considered the most hawkish member of the Fed), offered dovish commentary regarding rate hikes in response to pressure in Oil prices.

- That short-squeeze was quickly faded out of markets as Asia opened and simply sold that rip, followed by additional selling in Europe and now, more selling out of the United States.

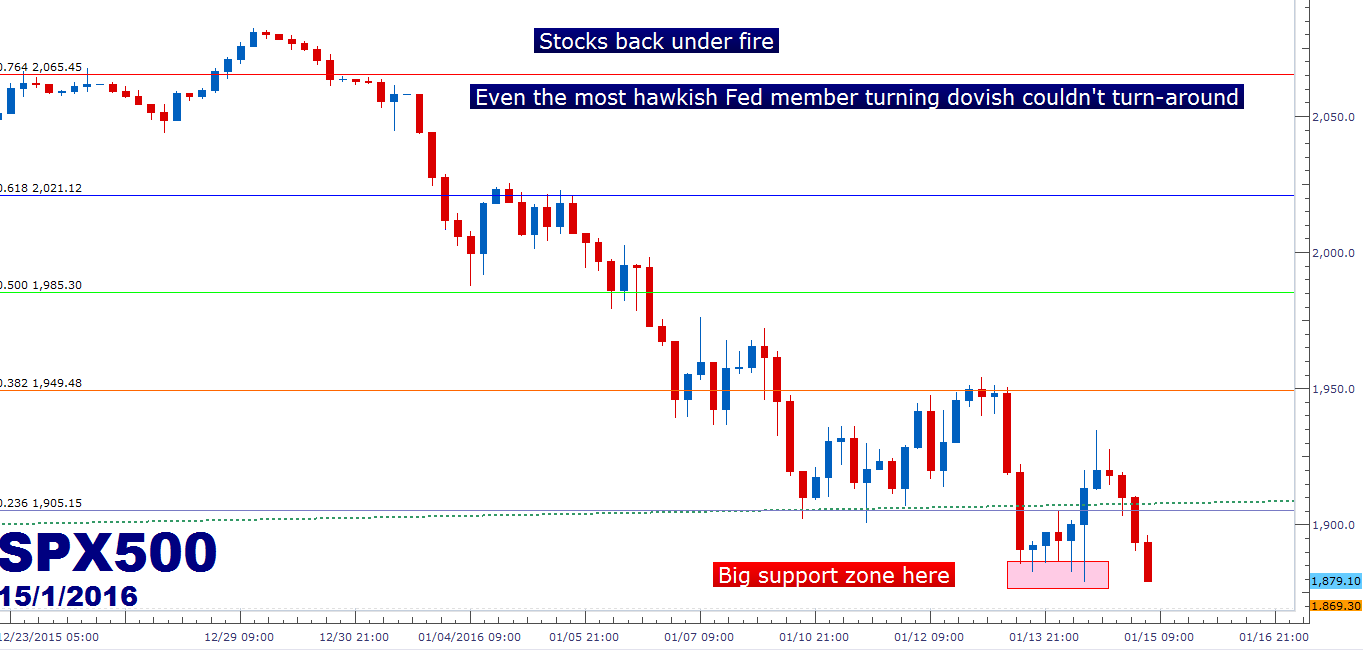

- This is a clear shift in tone for markets. Buy the Dip has become Sell the Rip. The one thing that may be able to turn this around might be the Fed shifting their stance away from their expectation for four full rate hikes for this year: Watch for Fed-speak on this theme in the coming weeks should pressure persist.

Yesterday was a pretty amazing day across markets. In our Market Talk piece yesterday, we discussed how the primary pressure point that seems to be exacerbating the carnage in commodity prices or the slowdown that’s picking up in Asia, it’s probably from the insistence of the Federal Reserve to kick rates up a full four times this year. We spent much of last year bantering over one, single rate hike. That just happened in December, and it takes some time for rate hikes (or cuts) to transmit through the economy; it’s not an overnight thing. So we don’t even know what the full macroeconomic impact of this rate hike is and already the Fed is looking at four more. This would probably freak markets out even if we weren’t watching Oil prices fall through every notable nearby support level, but the combined impact of these two themes converging at the same time, and added in with some significant risk of a pullback in China, and investors around the world, for the first time in six years, have more reasons to avoid risk than they do to absorb it.

Yesterday, we saw confirmation that rates are the pressure point, at least in the United States. Shortly after we published, discussing how each Fed member that’s spoken thus far on the year has seemingly taken a hawkish tone towards these four rates hikes; and we saw something quite notable take place shortly thereafter. The gentleman that is often considered to be the most hawkish member of the Federal Reserve took a markedly dovish tone. Mr. James Bullard of the St. Louis Fed mentioned that the recent moves in Oil prices have implications for the Federal Reserve’s rate hike plans. I know, I know; this sounds like a very obvious, no-brainer kind of statement. But hearing this from the most hawkish, rate-hike driving member of the Fed is notable.

Shortly after these dovish comments made their way into markets and the S&P 500 had begun trading higher. In a market that was getting heavily net short with very few bulls to be found, this small spark turned into a quick fire and the short squeeze was on. After shedding 20 handles in morning trading, the S&P put in a vigorous reversal of 55 points, setting a new short-term high just shy of our 38.2% Fibonacci retracement at 1949.

Created with Marketscope/Trading Station II; prepared by James Stanley

Even though this smelled of a short squeeze, in which a market caught heavily net short sees stops get triggered as prices rise, investors must take note of such situations. This is precisely what helped to turn stocks around in August and September of last year. As we neared the September Fed meeting in which the bank was expected to kick rates up for the first time in nine years, markets were freaking out and the Fed assuaged their fears by taking on a dovish stance. Eventually, stock prices came back as we, once again, had the support from the Federal Reserve.

But as stock prices came back and as normalcy was restored, the Fed got right back on that rate hike theme as we moved into December, and finally kicked rates higher at that meeting. But the strength that came back to markets in the middle of October was largely resultant of the Fed moving from hawkish back to dovish in response to economic pain increasing around the world. It started as a short-squeeze, and turned into an up-trend.

But that up-trend led to a lower-high, and the Fed did kick rates higher in December, so now there are quite a few reasons for investors to avoid risk, especially combined with the flurry of factors plaguing the global economy.

This is why yesterday’s short squeeze has stopped short, at least for now. As Asia opened up, investors just used that little bump in stocks to sell at better prices, and when Europe opened up that theme only continued. The S&P is back down and lower than we were yesterday, and it’s safe to say that the short squeeze is over.

This is why trend identification is so utterly important. News is often subjective, and the market’s manifestation on that news is usually even more subjective (and relative); but a market’s bias will often allude to the manner or direction in which that news will be priced-in to a market.

Right now the bias is to the down-side with the potential for panic should themes in Asia, Commodities or the Middle East heat up; and given recent pressure points this will likely remain until the Fed officially shifts their stance from expecting/looking for four rate hikes in 2016.

Created with Marketscope/Trading Station II; prepared by James Stanley

Thus far, the year has developed very similarly to how we had outlined in our Market Talk series to complete last year, entitled the Top 3 Themes Facing Global Markets in 2016 . The first part of that series looked at an Asian slowdown, and with Chinese stocks getting halted on the first day of trading this turned out to be a pretty strong pressure point for the global economy. The second part of that series looked at continued carnage in commodities, and how this will likely bring lagging performance in US corporate performance. And in the third part of that series we discussed rates, which is the elephant in the room and will likely be a primary point of contention moving forward.

The reason is because the Fed knew of these risks when they hiked and they did it anyways. There was another reason for this hike, or at least looking at the situation deductively there was another motivation for the bank to kick rates up when the global economic situation was so utterly sensitive. We discussed these risks a few days ahead of that hike in the article, Is the World Ready for a Rate Hike From the Fed? At the time, Chinese stocks were still clinging to support in the bear-flag formation that we had been discussing.

So while this doesn’t preclude the bank from moving back towards a dovish stance, similar to what happened last year when they backed off of rate hikes in March and June, it does mean that there are likely other factors of consideration for the members of the Federal Reserve, primarily in the realms of asset prices as QE has essentially just driven capital into asset classes beyond reasonable levels. Case in point, the S&P 500 is 280% more expensive than it was six years ago, while GDP grew only 12% in the United States over the same period. And last year’s flat performance indicated a potential top in the up-trend, as flat years have usually led to ‘big movements’ in the S&P 500.

This is why I had set up short stocks as my trade of the year. The situation had aligned nicely between the technical, fundamentals and the risk-reward of the setup.

So there has been some divergence, and something has to give eventually. The question is whether the Fed wants to risk putting even more gains in asset prices before ‘normalizing’ policy. And there is a time factor here – with rates really low, pension funds and income investments bring abysmal returns. So if Social Security was in a precarious place five years ago, it’s in a really dangerous position now with investment returns at such meager levels.

This isn’t as easy as ‘yay or nay’ on rate hikes – there are massive repercussions from whichever direction the Fed moves, and nobody knows how this will turn out.

Until then – use price action to show you the move and how to hit it – manage your risk appropriately (this should always be done when speculating in any market), and try not to get too caught up in any one move because, as we saw yesterday with the S&P’s 55-handle rip, even being ‘right’ in the short position in a bleeding market can bring on discomfort. This is why support and resistance is so important – it tells you when to bail or it shows when a move failed. And a lower-high is a great opportunity to add to short positions in a down-trend; that’s how the rest of the world treated this move in stocks yesterday.

As we’ve been discussing – the S&P isn’t the only place to play this theme. Japan is in a far more vulnerable, precarious state.

Created with Marketscope/Trading Station II; prepared by James Stanley

--- Written by James Stanley, Analyst for DailyFX.com

To receive James Stanley’s analysis directly via email, please SIGN UP HERE

Contact and follow James on Twitter: @JStanleyFX