Talking Points:

- The morning has started with bounces in global stocks not traded in China. China saw brisk drops throughout the session, but the Yuan strengthened significantly, and in-turn, global stocks recovered.

- This short-term recovery in risk-trends could afford the opportunity to look for trend resumption setups for the remainder of the week, namely against Japan by buying the Yen and selling the Nikkei.

- Warning signals are still flashing aggressively with Copper prices falling to a new 5.75 year low, and Oil prices falling below $32.50. This theme appears to be far from over.

- To time trends, our SSI tool can be helpful. You can access SSI in real-time directly at this link.

It was an aggressively bearish session for Chinese equities to open the week, as stocks gapped lower and never really recovered while facing persistent selling throughout the session. After last week’s -10% decline, the Shanghai Composite shed -5.33% and Shenzhen was hit by a -6.6% loss, bringing the year-to-date returns on the Shanghai Composite to -14.76%, and Shenzhen’s running tally is currently at -19.96%. And this is over a grand total of only six trading days.

Curiously around these movements in stocks - the Yuan was fixed at a stronger rate last night, which should’ve spelled relief for stocks, as Yuan weakness in response to the Chinese slowdown was perhaps the most troubling part of the further development of this theme for Global equities. The thought being: As China continues to slow regulators would continue to guide the value of the Yuan lower. This weakness in the Yuan could spell trouble for trade partners, as it makes domestic production and consumption in places like Japan, the United States and Europe more expensive, on net, with a weaker Yuan (because the same good can be produced even cheaper in China with weakness in the Yuan v/s USD, JPY, or EUR). So, as China’s equity markets were peeling off and as the Yuan was bracing lower, the rest of the world ducked for cover for fear that China would continue slamming the Yuan lower.

That didn’t happen last night, and Chinese stocks still put in huge move lower. This may be highlighting that the Asian slowdown theme is taking on a life of its own, where investors in Chinese stocks are hitting the offer regardless of what good news might be happening. After last week’s halts and circuit breakers, many are still rightfully jumpy around these asset classes, and that will likely remain for a while.

The silver lining of last night’s session is that stocks outside of China saw some relief during last night’s session with the Yuan moving higher. So, as Chinese regulators fixed the Yuan at a stronger rate – we saw Chinese stocks sell off while most other global bourses moved higher. This highlights the potential for the Yuan to be one of the primary pressure points in the coming week. The chart below illustrates the recent moves in the Yuan:

Created with Marketscope/Trading Station II; prepared by James Stanley

This opens the door for some interesting plays: So, to summarize last night’s price action: We basically had retracements in some major trends led by Yuan strength (and Yuan weakness has been one of the primary drivers of risk aversion). There was no data or evidence that the weakness that’s been seen thus far in the new year is close to receding; and the potential for further development of risk aversion is probably about the same as it was last week (we’ve had zero data to indicate otherwise, at least so far).

So this can open the door for trend resumption plays.

One of the more attractive areas to play this theme could continue to be in the Yen. As we outlined in the article, the Yen as the safe-haven vehicle of choice, Japan is in a very vulnerable position after 3+ years of QE have been unable to bring any actual semblance of a legitimate recovery into the economy. This is a clear example of where monetary stimulus hasn’t shown any signs of actual progress in the real economy as continued attempts at fiscal reform have failed.

Monetary stimulus, by design, is not meant to grow economies. It’s meant to stop or stem slowdowns. And while the Nikkei may have moved higher and the Yen lower on the back of these policies, inflation is still lagging and the Bank of Japan has some very big issues to contend with. Japan is already carrying a greater than 2.25 debt-to-gdp ratio, and with such a large portfolio, they’re already spending a large portion of their budget on debt service, and this is with yields at record low values. This was a central portion of the analysis that my colleague Christopher Vecchio utilized for his trade of the year in short GBP/JPY, which has amazingly already hit its first target in the first trading week of the year.

As we outlined in the article series, The Top 3 Themes as We Approach 2016, in Part 1, we discussed an Asian slowdown, and we concluded that for investors to gain exposure to this theme they’d likely be best served by looking to Japan.

So far on the morning we’re seeing retracements in both the Yen and the Nikkei, and this could open the door for trend resumption plays. The first chart below is in AUD/JPY, which could be one of the more ‘risk-sensitive’ pairs should risk aversion continue to develop, and after that we’ll look at the Nikkei.

Created with Marketscope/Trading Station II; prepared by James Stanley

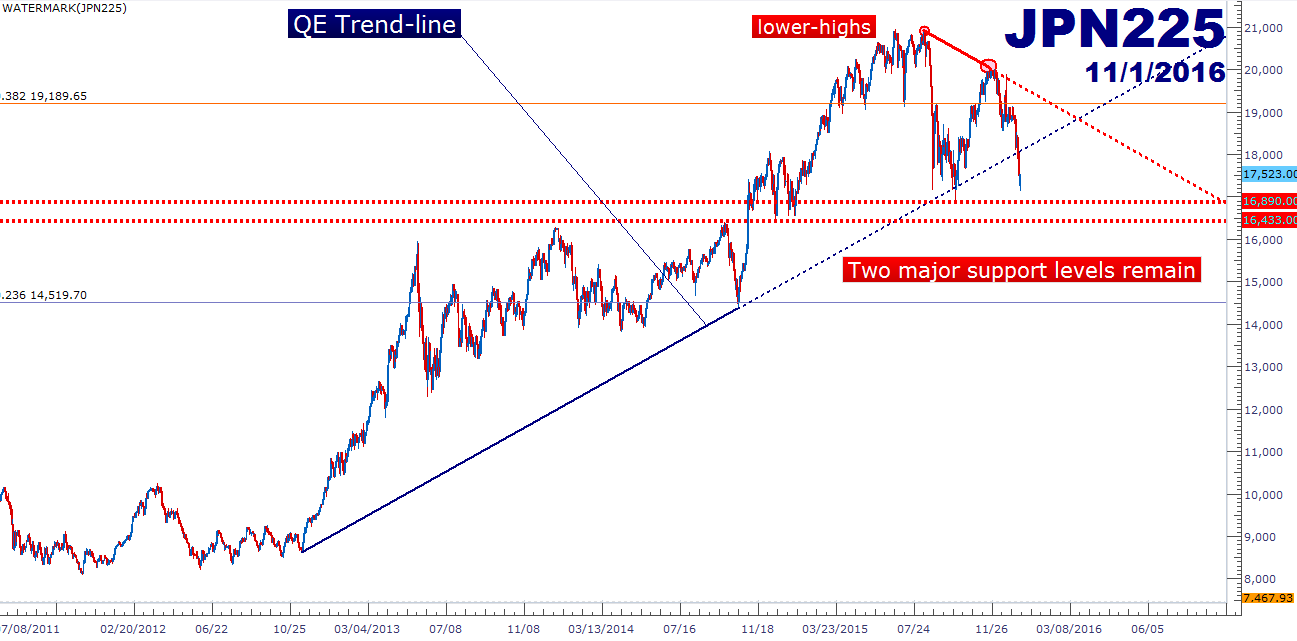

And in Japanese stocks, we have a similar type of situation in which the lows from last summer are coming into question as persistent selling is driving prices lower:

Created with Marketscope/Trading Station II; prepared by James Stanley

And for the shorter-term setup, we’re looking at the hourly chart below with potential resistance areas based on prior support values. This is a ‘price action tell’ that could give traders the idea that sellers are coming back into the market and responding to resistance.

Created with Marketscope/Trading Station II; prepared by James Stanley

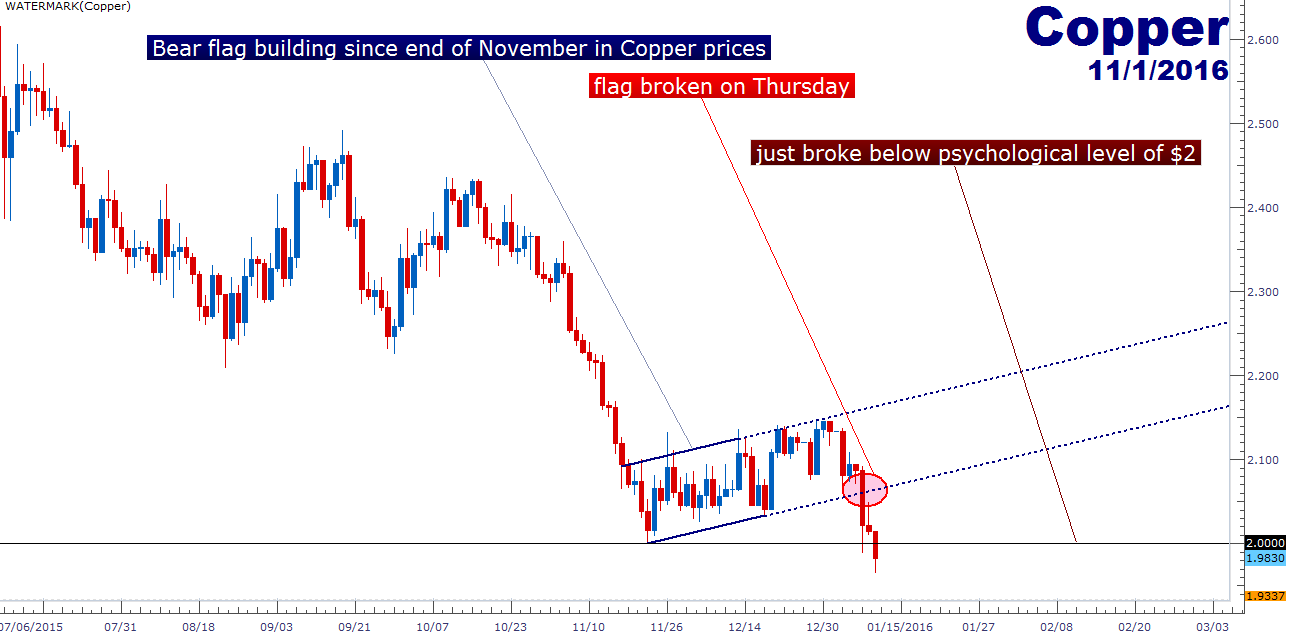

More troubling on the early week is the movement being seen in commodities: Back in November we discussed this theme, as stocks around the world were shooting higher in a run that looked like a 2011-ish bull market, there were still some very real structural problems underneath the surface; primarily the continued bleeding in commodity prices.

In many cases, commodities can exhibit some degree of correlation with other assets, currencies especially, as an economy molds itself around a point-of-strength. Think of the CAD correlation with Oil as a strong example of this theme, but perhaps more interesting are the potential leading qualities that some commodities might be telling us about the economy.

We’re speaking of Copper, which has huge industrial usages and can often be a strong indicator of future growth. Because as an economy grows they’re probably going to need to build; and to build, they’ll likely need electricity, and for that, Copper will be a necessity. So as global growth is picking up, so do copper prices. And as global growth is slowing, copper prices move lower to reflect this lessened demand. The chart below illustrates the recent moves in Copper prices, with the recent acceleration lower:

Created with Marketscope/Trading Station II; prepared by James Stanley

This is basically what has been happening in Copper for the better part of six years. Sure, stocks were shooting higher and risk assets were taking off, but global growth was slowing for most of the time, led in large part by China. What was once a 10% growth target for China is now looking more like a 6.5% marker, and even that looks like it might be difficult to attain from here.

But the fact that Copper has been selling off for most of the time has shown that not all is well. The one differentiating factor between this year and last (when copper prices were still going lower, but stocks were staying strong) is the Fed, and the fact that the world’s largest national Central Bank is now actively tightening policy with rate hikes.

So, while a slowdown in growth may have been forgivable or insignificant to investors last year or the year before, with the Fed now tightening policy, these risks have become massively magnified.

This morning has already seen a significant move: Copper fell below the psychological level of $2, for the first time since March of 2009. Just four-and-a-half years ago, Copper prices were twice where we’re at now, and this just highlights how profound this slowdown has been despite the Fed’s easy money policy keeping most equity bourses artificially high.

So this theme of slowdown appears to be far from over, despite any near-term strength that might be seen in stocks.

--- Written by James Stanley, Analyst for DailyFX.com

To receive James Stanley’s analysis directly via email, please SIGN UP HERE

Contact and follow James on Twitter: @JStanleyFX