Talking Points:

- As we near the end of the year, we’re addressing the top 3 themes that the economic world faces going into 2016.

- On Tuesday, we looked at the risk of a larger slowdown in Asia.

- Yesterday, we examined the continued carnage in commodities and how that may play out next year.

- Today, we look at the elephant in the room of the global economy: Rates.

We’re in the midst of one of the largest economic experiments that the world has ever seen conducted. And while it would be fantastic to be able to look back at a similar period in history so that we could find a comparable scenario to see how it’s played out before, we simply do not have that luxury right now. Never has the world seen this much stimulus jammed into the financial system, and never has the world seen so much coordination between Central Banks around-the-world. This is the underbelly of globalization, and we’re all in the same mess together.

Interest rates play a critical role in the successful operation of a fiat currency system. Interest rates drive investor behavior, and this is and will always be the ‘most operative’ tool for a Central Bank to accomplish their goals. Interest rates are to a Central Bank what an equity line is to a trader: Their primary tool for accomplishing their job. If a Central Bank wants to slow down the transmission of capital throughout the system, raise rates. Higher rates attract capital in safer, more structured fixed-income investments while also taking capital away from riskier activities. After all, if rates are higher, opportunity costs for investors go up. This has an amazing ability to slow down the money supply as rates are moving higher.

On the flip side – if an economy is facing pressure, Central Banks can cut rates and that makes fixed-income investments look utterly unattractive. So now there is far less of an opportunity cost to invest in those riskier activities. And on top of that, with rates moving lower those riskier businesses can borrow money more cheaply, thereby giving them a higher probability of actually ‘making it.’ So this drives capital into riskier asset classes as investors a) have to seek out higher yields/returns and b) makes for a more amenable operating environment for corporates. Investments in stocks or junk bonds get really attractive around this stage of the business cycle because investors are essentially getting Central Bank support behind their investments.

A good example of this at work was housing in the United States leading up to the Financial Collapse. The technology bust that started in the year 2000 was brutal. The stock market declined for a full two years on a path from over 1,500 to just above 750. So we saw the S&P split in half over this two-year period. That was an anemic, depressing environment. So in an effort to offset this hangover from the tech bubble collapsing, the Federal Reserve continued to move rates lower until, eventually, economic activity began to increase. What was interesting here was WHERE that activity was taking place: With rates at record lows (at the time) this compelled many folks to go out and buy a home. After all, if the cost of capital just moved lower, it’s now more advantageous to buy v/s rent with all other factors held equal. This created demand for housing, which eventually brought home prices higher. As home prices moved higher, the attractiveness of investing in real estate increased massively. One could simply go to the bank, borrow funds cheaply, invest in real estate and then wait and print a profit with a decent degree of profitability.

This is when folks started flipping houses, and this led to near pandemonium in home prices. Eventually the American economy was no longer weak. Interest rates had to move up to try to slow the growth in home prices to a reasonable level. But it was already too late, the bubble had started to build and home prices were ratcheting higher regardless of any rate hikes out of the Fed.

Eventually – anyone that wanted to buy a home had one. Or maybe even two or three that they were looking to flip. And there was no one left to buy. So prices went down. Pretty standard stuff really, just the business cycle at work.

The chart below illustrates the relationship between real estate (using the ETF of ‘IYR’) and stock prices (using the S&P) during this most recent interest rate ‘cycle.’

Created with Tradingview; prepared by James Stanley

The problem here was that mortgages were such a traditionally staid asset class that many didn’t see the risks in the environment. After all, who wants to default on their mortgage? Who actually wants to be homeless? Not many people, so likely, folks will do whatever they have to do to pay the mortgage. This led many banks and trading desks to push the leverage on these types of investments far beyond reasonable levels, in many cases over 30-to-1, which from a risk management standpoint is just insane (at least with hindsight being 20/20).

So when that bubble broke, we saw far worse than just a standard ‘correction’ to the business cycle: We saw a full-scale collapse because of the massive leverage that was taken on the back of low rates. Banks that traditionally were a key cog to the financial system were now, all of the sudden, worth negative values on paper with these horrific mortgage-based investments being marked to market. And when these banks started to blow up – that’s when the real fright began because of counter-party risk. Few outside of finance understand how much these banks depend on each other. So much so that if one of the major banks blows up, it will likely create a ripple effect throughout other major banks. If Bank A can’t pay on their investments to banks B, C and D – well, Banks B, C and D are going to be really careful towards taking any further risk on, if they’re able to take on any more risk at all.

This is contagion. One bank gets sick and then infects the entire financial system. This is the fear, because this could lead to ‘depression-like symptoms’ as risk-aversion causes everyone to just decide to go to cash for fear of getting hit by a falling bank or a bursting bubble. So when the Financial Collapse hit, the Fed had to respond in a very big way in order to keep matters from becoming significantly worse; because for a while it seemed as though the entire global economy was on the brink of a long-term disaster.

So ZIRP, at least initially, was a necessity. By taking rates to near-zero as an emergency measure, the Fed essentially prodded banks to continue lending and taking on risks. Not only was the Federal Reserve injecting liquidity into the system (basically giving banks fresh capital to work with), but they were also changing the investment landscape significantly. With rates moving to near-zero for the first time in American history, there had never been a worse investment environment for bonds. So banks, investors, you and I were all compelled to absorb more risk in the riskiest financial environment of our lifetimes. And it worked! At least so far and perhaps has even worked ‘too well.’ Because the same type of thing that happened leading into the Financial Collapse (low rates driving huge asset price gains) is happening today.

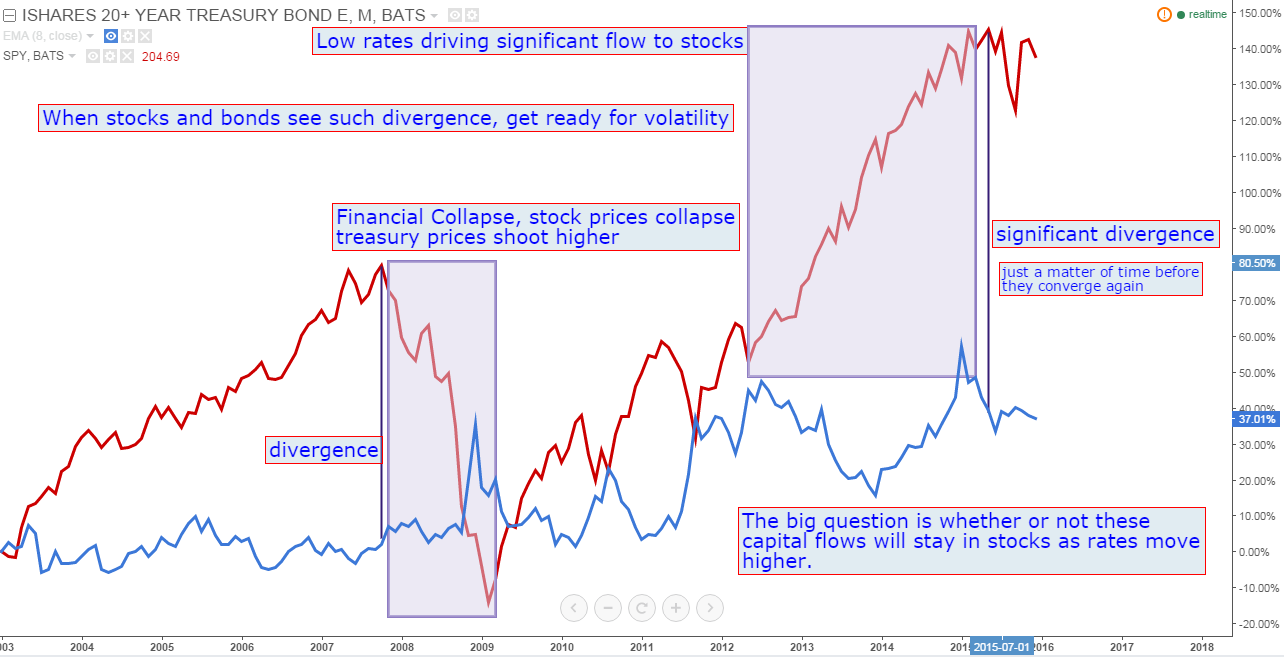

On the chart below, we’re again looking at the S&P but this time comparing it to long-dated treasury bonds as voiced through the ETF of ‘TLT.’ Notice the divergence that we saw in 2007 and how these themes converged as stock prices, inevitably, faced a correction. But this time – that disconnect is far more profound. Low rates have driven massive price gains to levels that we’ve never seen (not too different from real estate in 07).

ZIRP worked well to compel risk-taking behavior, perhaps a little too well

Created with Tradingview; prepared by James Stanley

So this has the Fed (and much of the world) worried. Ms. Yellen alluded to this fact in December when she said that she saw a higher probability of a recession if the Fed didn’t raise rates. So, to put this into a logical statement, Ms. Yellen (who has a remarkable track record as a forecaster) thinks that tightening monetary policy and slowing down the money supply will actually help the business cycle. This is a sign of just how distorted rates have become after six years of ZIRP. The Fed can’t stay on ZIRP forever, and this is what the rate hike in December was all about. This is why the Fed wants to continue raising rates, and is looking at as many as four rate hikes next year when the market is expecting only two: They want to prevent a massive bubble (or series of bubbles) like we saw in 2008. And to prevent a bubble – prices need to come down rather than continuing to shoot higher. So it feels like 2016 will be the year that the Fed engineered a correction in order to avoid a larger break-down should these risk-taking behaviors continue to drive bubble-like capital flows into many key asset markets. The question is whether or not the bubble has already been blown, and that’s what has investors so utterly fearful.

As the Fed walked towards rate hikes this year, stocks finally softened

Created with Trading Station; prepared by James Stanley

As the Fed continues down the hawkish path towards additional interest rate hikes, expect to see capital coming out of those previously high-flying markets as investors get more risk averse around-the-world. We’ve already seen junk bonds get hit. After the fright of a meltdown in Asia tagged most equity markets in August and September, we saw stocks recover but junk bonds just continued to be sold off. These assets are generally going to display a direct correlation given that they have similar prospects, both doing well in a ‘growing environment’ and poorly in a ‘slowing environment,’ so the divergence between these two assets since August is significant. Something is going on here. The big question is which is ‘right.’ In most cases of market history, the bond market leads the way because stock investments are just far more speculative than what smart money is doing in bonds.

Commodities have been another ZIRP-fueled asset class that’s begun to face significant headwinds as higher rates have entered the discussion; and this can carry some very troubling connotations as a larger slowdown in commodities will continue to impact corporates around-the-world, which will then spread to the banks and investors that had lent them money at extremely low rates. And if these banks get hit – just like in 2008, they won’t be too active in the ‘risk-taking’ department as their other business lines are taking outsized losses.

The troubling scenario about this theme around rates is that we’re in a very similar spot as we were in 2008, just this time, the potential bubbles aren’t relegated to real estate. The bigger and potentially more troubling situation is the bubble(s) that have developed in debt markets around the world, as low rates for six years have massively distorted investor’s risk-taking behavior. As rates go up, the entire world is going to get really very honest really very quickly.

This doesn’t necessarily spell doom-and-gloom: Central Banks won’t go down without a fight, and it’s unlikely that Ms. Yellen will keep jacking up interest rates should headwinds be seen. And it’s not out of the realms of possibility for rates to come back down should the environment get significantly more unfriendly. And we may even see negative rates come into the question before too long, who knows? If the past six years have taught us anything, it’s to expect the unexpected. And should rates go negative in the United States, we’ll all be likely dealing with way bigger issues down-the-road.

So, the question comes down this, and this is likely what Ms. Yellen is looking at: Do we go for a ‘milder correction’ right now, or do we risk a massive collapse down-the-road by keeping the liquidity cannons firing at full steam? It appears as though Ms. Yellen and the Fed has already shown their hand towards their preference with the expectation for four hikes in 2016, and this is what makes interest rates such a pivotal component of next year’s financial environment.

--- Written by James Stanley, Analyst for DailyFX.com

To receive James Stanley’s analysis directly via email, please SIGN UP HERE

Contact and follow James on Twitter: @JStanleyFX