Talking Points:

- The Federal Reserve’s long-awaited meeting is here: The bank is finally expected to hike rates at this afternoon’s meeting. The statement is released at 2:00 PM ET, followed by the presser at 2:30.

- Given that this hike is largely expected, it’s rationale to expect that it’s mostly priced-in right now. But the peripherals of today’s meeting will likely determine price action trajectory. If the Fed takes a dovish approach towards inflation expectations or the dot-plot matrix, we could see USD-weakness even though the bank hiked.

- This is one of the biggest news events in years. The world has never seen what happens after rates move up after six years of global stimulus. Neo-Keynesian economics is about to face its toughest test yet. So, be careful. If you don’t know what to do for today’s news announcement, now is a good time to work on that approach. To that end, we have the 360° course as well as our Traits of Successful Traders research series. These could certainly be nice additions to the approach.

The long-awaited Federal Reserve meeting is finally here. We’ve seen this discussed in financial media for much of this year, and for a while there, it really looked like we might have to wait until 2016 or 2017 for that first hike in 9 years; but alas, we are here, and most economists/analysts are going into this Federal Reserve meeting with the full expectation that we’re going to finally see a hike.

It’s all About the Dots

It’s the surrounding details around this afternoon’s meeting that will likely shape price action moving forward. And since today’s hike is largely a foregone conclusion that’s likely already priced-in to many markets, the next obvious focus becomes the Fed’s Dot Plot Matrix. This is the chart in which each Fed member can voice their opinion on where interest rates will be in coming years. For much of this year, these dots (Fed expectations) have remained quite divorced from market expectations, with the Federal Reserve expecting four hikes next year. Markets are currently pricing in two. Given the pandemonium that we’ve seen around the world this year around ONE rate hike, expecting four may seem to be a little on the aggressive side.

So, the dot plot matrix becomes the initial focus after a rate hike because this sets the stage for the Fed’s stance going into 2016. Should the Dots happen to fall (Fed members expectations for higher rates moves lower), this could be perceived by the market as a ‘Dovish Hike,’ not too different from the ‘hawkish hold’ that we had back at the September Fed meeting when the bank backed off of that long-awaited decision. Under this scenario, we could see stocks and risk assets move higher initially as Fed expectations merge more towards market expectations with a softer stance towards 2016 rate hike trajectory. The biggest takeaway from this development would likely be seen in weakness in the Dollar. While the market is only expecting two rate hikes next year, the fact that the Fed has continued to hold on to this ‘four-hike’ theme has kept bullish bets in the Greenback. If the dot plot matrix moves lower, we’ll likely see some of those USD-bets come out of the market, and that could lead to USD-weakness.

So don’t be surprised if EUR/USD ratchets higher in the dovish-hold scenario, driven by USD-weakness as 2016 rate hike bets recede out of the market (we discuss EUR/USD specifically with more detail below). On a technical basis, traders can look to the 12,050 zone in the greenback. This zone has seen support for three of the past four trading days, and this is also a projected trend-line that had defined the prior symmetrical wedge in the Dollar.

But should this support hold (or for those that want to get long USD ahead of FOMC), this could be a critical zone for managing risk on dollar positions. Traders can look to lodge stops below 12,050 so that as long as higher-highs continue coursing through the Dollar, they can remain in the position (and if you’d like to learn more about risk management, check out our Traits of Successful Traders research). And if you’d like to look at additional USD-setups ahead of today’s meeting, check out my colleague Christopher Vecchio’s morning report, entitled ‘Trade Setups in USD- pairs Ahead of FOMC.’

Created with Marketscope/Trading Station II; prepared by James Stanley

Inflation

The Fed has said for a long time that rate hikes would be data dependent. But every barometer they’ve given markets thus far for that dependency has been shifted. Do you remember the 6.5% unemployment rate threshold? Well, we’ve been at 5% for two months now, and many economists consider this ‘full employment’ in the United States; so if anything, those pledges for data dependency have introduced more risk than they’ve offset in markets, because if the Fed doesn’t do what they say they’re going to do, they start to lose the confidence of market participants, and in a fiat-based system, confidence is all that really matters. It’s what keeps consumers consuming and markets moving. Without it, we risk catastrophic failure that requires the emergency-like policies that we have in place today.

But on the front of ‘data dependency’ we can look to the second of the Fed’s two mandates for clarity, as inflation has been that differentiator that allowed the bank to back off of hikes once we saw unemployment below 6.5%. This has been the boogeyman of this most recent recovery, as inflation has remained subdued for the better part of six years since ZIRP came into play in the Financial Collapse. The Fed targets 2% inflation, and by most metrics, we’re far from that.

The Fed’s favored inflation metric is the Personal Consumption Index, which you’ll commonly see referred to as ‘pce.’ The most recent print there was at .2% (not 2%, but .2%, or 1/10th of their target). We did see core CPI finally move to 2% in November, but this strips out food and energy, so many question its effectiveness towards actually reading price pressures in an economy and this is why the Fed looks to ‘pce.’

With policy being shifted from ‘emergency action’ to more normalized, these inflation reads will become even more important in coming quarters. Should inflation move lower after this rate hike, we probably won’t be seeing as much motivation from the Fed to hike in 2016, and this, again, can equate to USD-weakness.

But don’t look for the Fed to give away any much needed flexibility here. While they will likely mention ‘data dependency,’ it’s unlikely that they will give us a rigid framework with which rate hikes will be enacted in the future. With this ever-important turn in policy, it would make sense for the Fed to try to retain as much flexibility as humanely possible.

Expect the Unexpected

If the ECB reiterated anything to markets, it’s the fact that you don’t know until you know. What makes markets great (uncertainty) is the same thing that makes markets dangerous (risky). There is a lot of grey area for the Fed to work with here, namely what the bank may do with that $4.5 trillion portfolio that’s been collected through 6 years of QE. We’ve never seen a bank start a rising-rate environment with questionable underlying fundamentals after six years of ZIRP-driven asset flows. We are setting the precedent here, and neo-Keynesian economics is about to face a whole new range of tests. The Fed isn’t taking this lightly: Markets aren’t taking this lightly; and its very likely that we’re going to get something today that is impossible to expect with given facts right now.

So as always during news announcements, keep the risk light. This one, especially, could present significant risk across markets. We will see history made today (and in coming days as markets react). What the future holds, nobody knows: But you probably don’t want to risk your entire trading account into that uncertainty.

The Euro

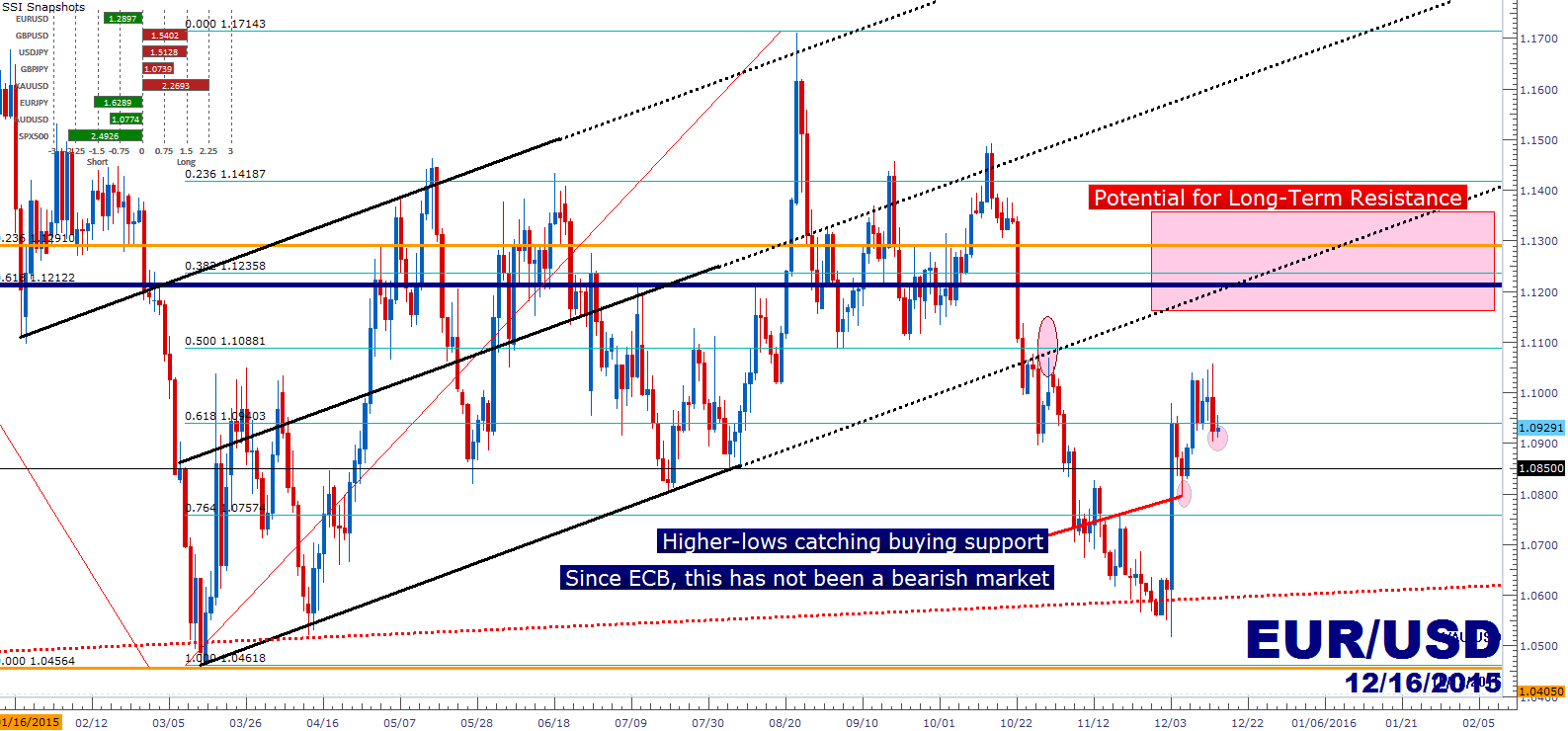

So, on that topic of the Euro, don’t be surprised if EUR/USD makes a new high should the Fed take on the dovish-hike approach. Retail traders have moved to a net-short position since that ECB-disappointment two weeks ago, but traders should urge caution: EUR/USD is still looking bullish on the Daily chart as we’re seeing higher-lows supported with buying interest. On the specific topic of EUR/USD, what’s happening here isn’t without precedent. We talked about this ahead of the ECB disappointment in December, in the article entitled The ECB Fires a Warning Signal, but Will They Deliver in December. We basically just referred back to last year when the ECB initially announced their QE policy. In May of 2014, Mario Draghi announced that an announcement would be forthcoming. So everyone jumped in the short Euro trade expecting a bazooka in June. But that didn’t happen; the ECB disappointed and then the EUR/USD rallied from ~1.3500 to ~1.3700 in short order. In July, the ECB finally delivered and this started the nine month march lower in the pair.

From a purely strategic standpoint, it made a ton of sense for the ECB to not over-extend themselves ahead of this Fed meeting; and it certainly could prelude additional action down-the-road from the ECB. But for now, the pair is bullish and should be treated as such. For those that do want to look for longer-term short positions in EUR/USD, look to the 1.1200-1.1300 zone. There are a couple of key Fibonacci retracements in that vicinity combined with the under-side of the bear-flag that’s defined price action for much of the year in the pair.

Created with Marketscope/Trading Station II; prepared by James Stanley

--- Written by James Stanley, Analyst for DailyFX.com

To receive James Stanley’s analysis directly via email, please SIGN UP HERE

Contact and follow James on Twitter: @JStanleyFX