Talking Points:

-The events in Paris on Friday provide significant uncertainty for the future; and with markets already on edge, this may be a prelude to a tipping point in the coming weeks/ months.

- Japan went into recession, again, with a -.8% read on Q3 GDP; the second consecutive quarter of contraction.

- The IMF issued a report on Friday indicating a recommendation for the Yuan to be approved as part of the IMF’s SDR (Special Drawing Rights) basket of reserve currencies.

1. The biggest items for this week might not be on the economic docket: The headlines are being dominated by the Friday events in Paris, but for the remainder of this article I’m not going to discuss the topic out of respect for survivors and family members of victims. Perhaps more to the point of the discussion of macroeconomics, nobody really knows what the ramifications will be and it’s not worth blindly speculating how one might make money on such an event when so many innocent people have lost their lives.

But this does raise the possibility for additional conflict in the Middle East, which can certainly have economic consequences, and it also brings into question larger-overall European integration.

The big prospect here is one of risk aversion should events continue to develop, and we saw the initial signs of that on the open last night as the Yen initially strengthened along with Treasury bonds as we had the first signs of a ‘flight to quality,’ taking place. With an economic world already ‘on edge,’ with a deluge of fears, something like this could be a tipping point.

But this is where price action comes in. Price action can be the great differentiator here because it shows us the ‘whats’ from the ‘what nots.’ As in, if something is important, likely, we’ll see markets pricing that in and that will impact supply/demand which will, in turn, impact price. This is why it’s universally accepted that markets are efficient ‘some of the time,’ because, frankly, most of the traders at big banks aren’t stupid and if something is a given, then they’ll price that in. And as a price action trader, I’ll see that on my charts and I’ll be able to incorporate that into my analysis as quickly as its happening.

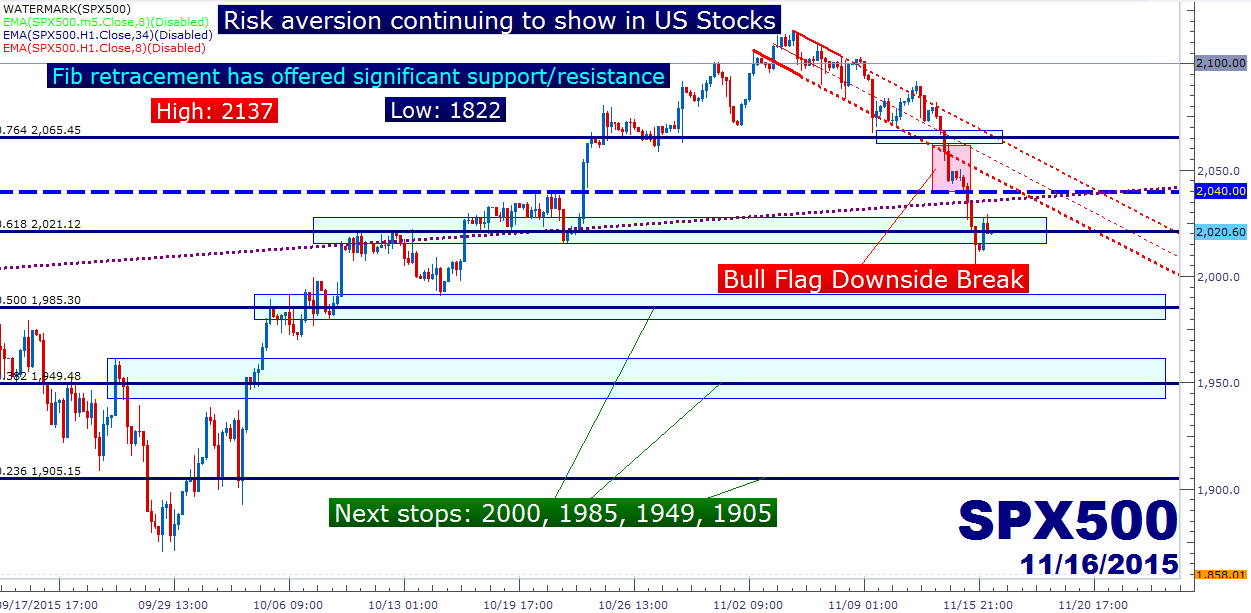

For now, price action in many stock markets is continuing the bearish tone that had come in after the October FOMC statement and then hastened by October’s blowout NFP report. Since that bullish print, risk aversion has continued to run higher in US stocks, and on the chart below, we can see the down-side break of the bull flag formation that was showing the S&P until last week. At this point, we’ve seen price action continue to run to the down-side with prices catching support at each of the Fibonacci intervals that we’ve been discussing over the past few months. To find this Fibonacci retracement, a trader can chart the major move from this year’s high to the low on China’s Black Monday. This produces intervals that have seen significant price action since that low was printed on August 24th, with support/resistance at 1905, 1949, 1985, 2021, and 2065.

Of particular note – this down-trend started well before last Friday, and likely, has more to do with the continued confusion around the Federal Reserve than any other single factor like Chinese/Japanese weakness, the Middle East, or even Oil prices.

Each of these levels could offer down-side entry potential, as well as risk-management levels for lodging stops and scaling out of winners. The chart below has the full setup, and you can click on the below image for a larger view.

Created with Marketscope/Trading Station II; prepared by James Stanley

2. Japan goes back into recession: Three years, two recessions. In the three years since Shinzo Abe stormed (back) into Japanese politics with his ‘three legs’ approach, Japan has now fallen into two separate recessions. This is yet another sign that Abe-nomics is not ‘working,’ at least not yet.

The Japanese economy contracted in the third quarter by an annualized .8%, which follows a .7% drop in the second quarter; giving us two consecutive quarters of slower GDP growth to meet that technical definition of ‘recession.’ The expectation was for a .2% contraction, so this -.8% print was quite a bit wider than what markets were looking for.

The big scourge of weakness in this GDP report was weakness in business investment, which is likely related to the larger-overall slowdown taking place in China, and in-turn, the rest of Asia. This flies directly in the face of Shinzo Abe’s demand for Japanese companies to reinvest more of their cash into capital investments. As QE-fueled Yen weakness brought cash hordes to Japanese exporters (who were essentially given a competitive advantage with an extremely weak Yen), Abe wanted to see this cash get reinvested into the Japanese economy. This is somewhat of the central tenet of using QE to recapitalize an economy, and if companies aren’t reinvesting these new-found profits back into the economy, QE is, essentially, for naught. The whole prospect of export-driven growth is that profits can be redirected into an economies capital structure to further grow the consumer-segment of the economy. This is somewhat like what China has been doing for the past 20 years, using exports to further build out their middle class to create more consumer spending that can act as a buffer during future recessionary periods in markets.

This is not happening in Japan, as further seen from this most recent GDP report.

Given the scope of this weekend news, price action in the Yen today is pivotal, as outlined by our own Christopher Vecchio in his morning piece today. The initial reaction on the open incorporating this most recent print saw Yen strength on the back of risk aversion (although this may have something to do with the Paris attacks on Friday night). But since the open, we’ve seen Yen weakness continue to permeate markets as the expectation for even more easing from the Bank of Japan continues to increase. After all, the one thing that the BOJ has been able to do successfully over the past three years has been to weaken the Yen; so expectations are for that to continue happening until it no longer works.

Big picture, the fight that the Bank of Japan is facing is likely un-winnable; as this is more of a mathematics/sociological issue; not unlike what China will be facing over the next 30-40 years with an aging population.

For now, follow the techs, as this is what will offer trade setups and allow a trader to manage their risk as these points of uncertainty continue to provide risk-ammunition to markets.

Bull Flag Breaking on USD/JPY with expectation of ‘looser for longer’ (click below for larger image)

Created with Marketscope/Trading Station II; prepared by James Stanley

3. It looks like the Yuan is about to become a reserve currency: On Friday, the IMF staff made the formal recommendation for the Yuan to be included in the IMF’s Special Drawing Rights reserve-currency basket, joining the US Dollar, the Euro, the British Pound and the Japanese Yen. This recommendation means that approval is pretty much a certainty, as the most of the major stakeholders in the IMF, including the United States, have already said that they will support inclusion if the Yuan met the IMF’s criteria which Friday’s approval signifies.

The big change from this move would be the fact that that other countries will now be more likely to include the Yuan in their Foreign-Exchange holdings; thereby serving to move towards China’s goal of opening up their economy to the rest of the world.

In a note from Christine Lagarde, she mentioned that Chinese authorities have addressed all operational issues that were mentioned in an initial analysis in July. There were no caveats to this statement, nor were there any over-hanging issues. This was a clear endorsement, and from here – it seems to be a foregone conclusion that approval will be granted.

The next steps will begin on November 30th at a meeting planned to consider this issue. The IMF Executive Board that represents the 188-member nations that it represents will make their decision based upon the report.

Once included, member countries will be able to access the Yuan like any of the other four reserve currencies in the SDR basket to meet balance-of-payment needs.

What does this mean for the Yuan? On its face, this should equate to Yuan strength as global central banks re-allocate holdings into the Currency. This should lead to additional demand that sees prices rise; and longer-term, this could add even more pressure on exports from the economy as a stronger Yuan makes these goods less competitive in the international marketplace.

But perhaps more to the point, this further necessitates China’s conversion to a consumer-based economy that isn’t as reliant on those exports as an industrialized country often is.

But the big question is how this might impact China’s Open Market Activities. That is, intervention, which was one of the big points mentioned in the IMF’s initial analysis in July and as China develops into a more consumer-oriented economy, this has been a key sticking point that has allowed the government to continue to exhibit an element of control in markets. In July, the meltdown in Chinese stocks had just begun, and regulators hustled to stem the declines by rolling out new policies and measures. This was at the center of the feedback that the IMF had delivered in July when it looked like China might have to wait for the next SDR review from the IMF in five years.

But since finding a bottom in the middle of October and as Chinese stocks have risen again, regulators have rolled back reforms and have let markets trade more ‘freely.’ This has led to lessened government action and, in return, the IMF has tentatively granted approval for the Yuan’s inclusion into the SDR basket.

The big question is what Chinese regulators might do during the next market scare, and whether they’ve had some flexibility removed by this IMF decision.

Curiously, the currency isn’t showing many signs of excitement. Since the open last night, we’ve essentially put in a range, although a huge move of Yuan strength at around 1:00 AM last night had quelled the initial signs of weakness in the currency. But we’ve ended up just about where we started, creating that doji candlestick formation that will so often be coupled with indecision at a potential turning point in a market.

(click below for larger image)

Created with Marketscope/Trading Station II; prepared by James Stanley

--- Written by James Stanley, Analyst for DailyFX.com

To receive James Stanley’s analysis directly via email, please SIGN UP HERE

Contact and follow James on Twitter: @JStanleyFX