Talking points:

-Nobody in this world really knows what the Fed is doing, even the members of the Fed.

- What they have successfully done over the past three months has provided vexing commentary on the scope of the global economy.

- Monetary policy is not a panacea; nor should it be treated as such. And right now, the Fed is teetering on the brink of disaster.

- The attractiveness of cash over the next 2-3 months cannot be understated, as we may be at a capitulation point as we near that December Fed meeting.

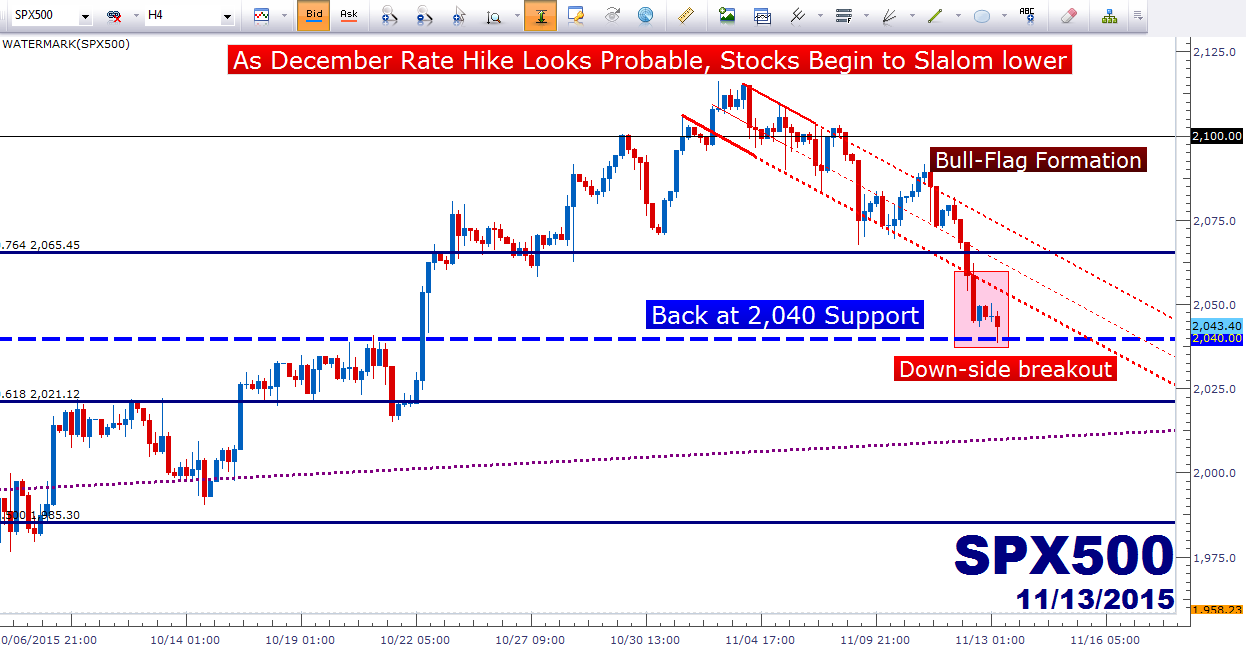

Stocks don’t seem to be enjoying the December lift-off theme: We discussed the multiple Fed members offering commentary in yesterday’s morning piece, and it became glaringly obvious that this was part of a ‘perception campaign.’ As in, numerous Fed members were talking about the pace of tightening rather than the timing of the first interest rate hike. It was quite obvious that there was some degree of coordination here, as the whole theme of ‘lift-off’ has taken on a life of its own in markets. But the big takeaway is that now that we’ve seen expectations for a December rate hike move higher, hastened by last week’s blowout NFP report, Global stocks are teetering lower on the prospect of fear.

(click below for larger image)

Created with Marketscope/Trading Station II; prepared by James Stanley

Discussing the pace of tightening seems logical, especially when you’re talking to a market full of investors that are expecting (or fearful of) a Financial Collapse 2.0, and have been loading up on risk assets for six years as markets were fueled by Zero Interest Rate Policy and Quantitative Easing; but this is probably what is providing so much confusion to the markets: Forward guidance.

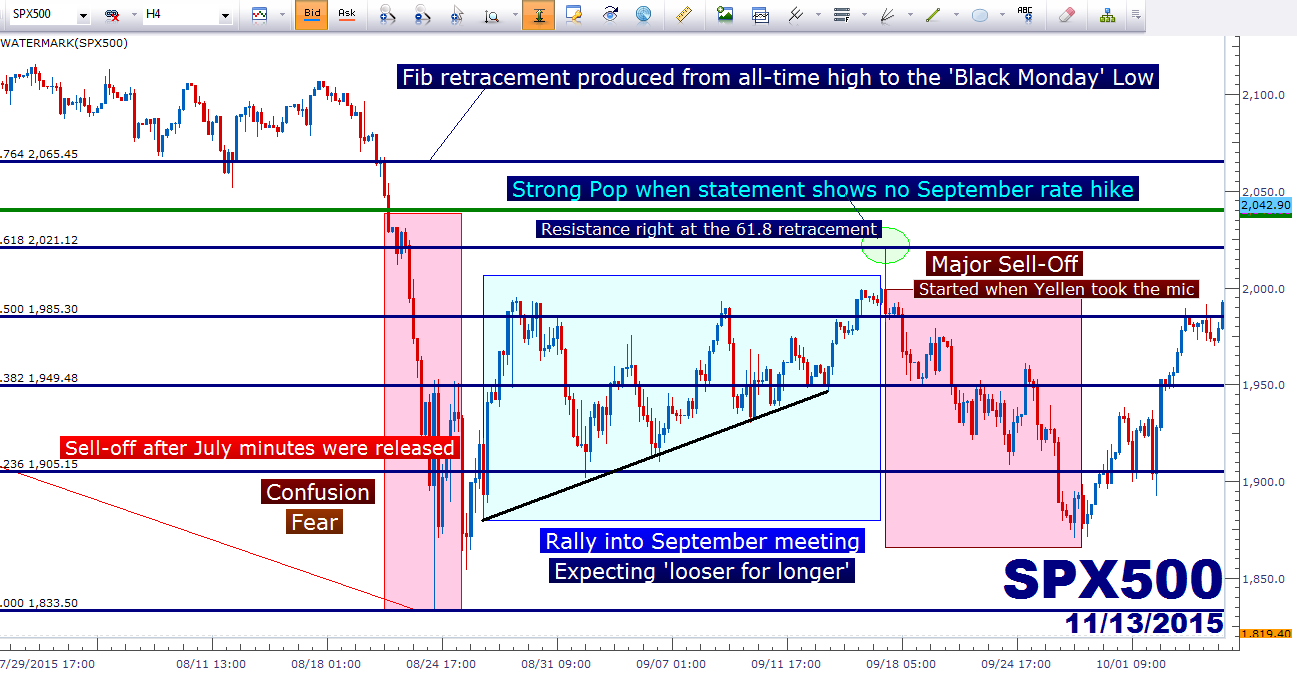

After all, the July Fed minutes that were released in August are what really started the pain in the S&P. This is when we finally broke below the vaulted 2,040 level that had provided support in the index for much of the year. And it was the release of these minutes that really began to confuse investors, as Ms. Yellen and the Fed had been talking up a September rate hike for most of the year, including at the July meeting, only for the release of these minutes to show a significantly more dovish tone. The release of these minutes actually made a September rate hike look questionable, and further, provided questions as to how bad the slowdown in Asia and the meltdown in commodity prices might impact the United States.

(click below for larger image)

Created with Marketscope/Trading Station II; prepared by James Stanley

This was a glaring signal from the Fed to the rest of the world that the global economy was slowing down, and we may need to brace for impact.

Somewhat relevant – even the release of those Fed minutes was a deterrent to confidence. The minutes were leaked a full 23 minutes early! So, in an environment in which investors are already skittish about what the Central Bank might do next, we see a leak of a pivotal set of meeting minutes. The entire thing just smelled ‘amateurish,’ especially for the largest national Central Bank in the world (even though the leak technically wasn’t their fault).

But on that topic of confusion, within the Fed release is a ‘dot plot matrix.’ This is a simple chart that shows each Fed member’s guess of where rates will be in coming years. This is a part of the larger overall ‘forward guidance’ that was implemented in 2011 at Jackson Hole as an effort to provide more clarity to investors. The goal was to let investors get a better idea of what is going on within the Fed. And in an emergency-like environment, this might be a good thing. But in terms of larger overall macroeconomic policy, this ‘extra information’ appears to be too much for markets to bear as it just serves to provide mass and utter confusion as people are trying to make important investment decisions; and we saw evidence of that at the September meeting.

After the August meeting minutes began to chip away at expectations for a September hike, investors rode into what was arguably one of the most important Central Bank meetings of the last five years. This was supposed to be lift-off, and we had heard from some Fed members for as long as three years that September 2015 would be the date. So we went into this meeting not really knowing what might happen.

The statement was released, as usual, at 2 PM, and there was no leak this time. The statement showed that the Fed was not going to hike in September, and the initial response in stocks was bullish. The dot plot matrix also came out dovish, as we even saw one Fed member vote for negative rates by the end of this year (which is probably super-dove Narayana Kocherlakota). The S&P rallied up to an important Fibonacci level of 2,021 to cheer this dovish stance, almost a full 2% from the low that was set not a month earlier as China’s ‘Black Monday’ roiled through markets.

(click below for larger image)

Created with Marketscope/Trading Station II; prepared by James Stanley

But at 2:30, Ms. Yellen took the mic for the press conference, and this is when things began to get ugly. Ms. Yellen continued to talk up a rate hike in 2015 despite the fact that the Fed just took a step back by holding in September. Of particular importance, the Fed mentioned that they wanted to monitor developments abroad (with an eye cast towards China), before they kicked up that first hike in nine years.

This was confusion. Investors hated it, and stocks sold off, en masse. And not just in the United States, this triggered an aggressive move lower all-around-the-world.

So, if we take a birds-eye view on matters, it looks like stocks sold off after a dovish Fed; but that would be intellectually disingenuous because that isn’t really what happened. Stocks actually went up on the dovish statement from the Fed (and the more dovish dot plot matrix); but they went back down after Ms. Yellen told markets the exact opposite of what the Fed just said; that a rate hike in 2015 was still on the table when this is obviously what nobody in the world really wanted.

This is utter confusion from what has become the lifeline for the global economy: Because we’re all in this together, whether we like it or not, and if China blows up or if the United States goes back into a prolonged recession, this would not be an isolated event that would stay relegated to the troubled economy. This stuff spreads, as the Financial Collapse and the European Debt Collapse have shown us. This is globalization, or somewhat of a microscopic transmission of the same problem being seen in Europe (nationalized interests in what is supposed to be an integrated economy).

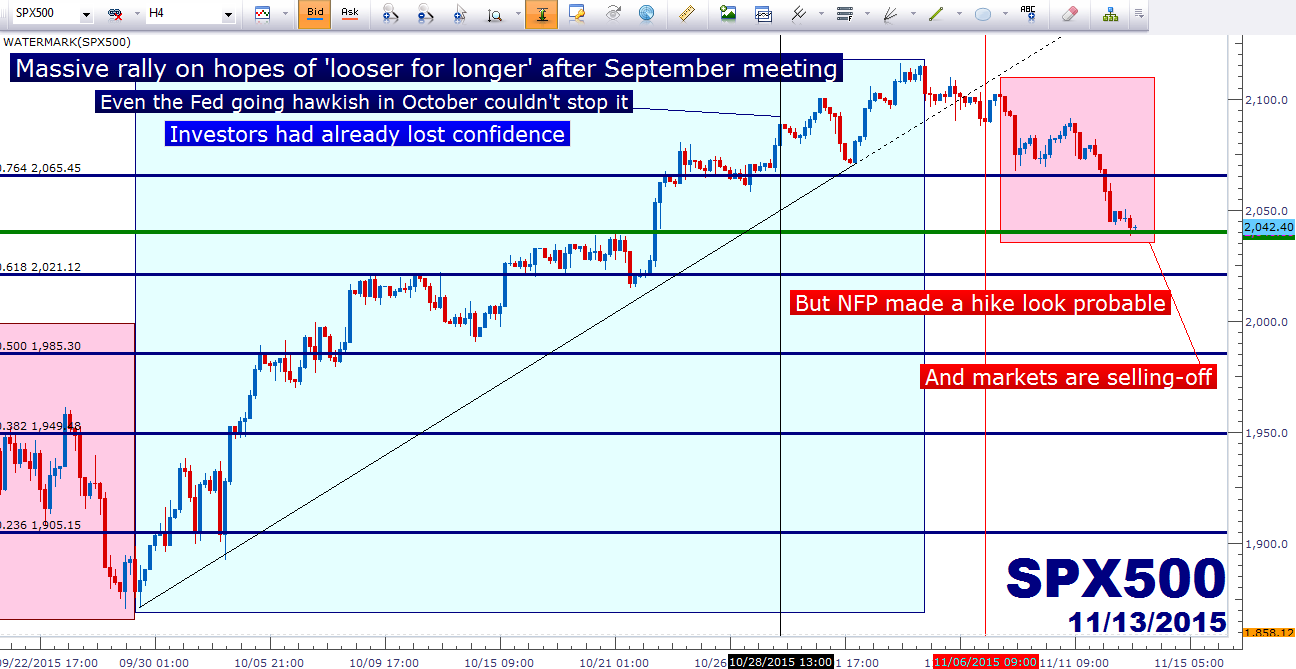

The sell-off after the September Fed meeting lasted for two weeks. But support began to come in as multiple Fed members offered dovish commentary along the lines of ‘well, if the world is melting down, we don’t have to hike.’ This saw rate expectations for that first hike get kicked all the way into the middle of 2016, and stock prices continued to surge on this expectation of dovishness and ‘looser for longer.’

This bought enough time for China to roll out a veritable artillery of stimulus designed to arrest the major market correction being seen there, and then Europe joined the additional-stimulus fray in October when Mr. Mario Draghi pledged to ‘re-examine’ the banks QE-outlay at their December meeting, largely inferring that the bank would increase their program if need-be.

So, as has become normal over the past six years, risk assets began rallying under the premise that Central Banks around-the-world would provide looser monetary policy for longer in order to keep markets from correcting. To further this theme, much of the economic data that we saw during this period would best be classified as ‘bad,’ so this further triggered those hopes of looser monetary policy for longer.

But something funny happened: Stocks didn’t just rally, they absolutely took off. The Shenzhen Composite in China is up over 33% from the lows. The S&P was up over 15% from their August lows in a little over two months… just outlandishly strong moves. And as this strength began to come back into stock prices, the Fed began to talk up that December rate hike again.

It was the October Fed meeting that really put that December hike prominently back on the table, as the Fed indicated that they were no longer as concerned about global economic pressures and were ‘on pace’ for a hike by the end of the year unless something unexpected happen. It was these caveats that provided an asterisk to this more-bullish forecast, and we noted in our post-mortem Market Talk of that meeting that “they haven’t done anything for nine years, and they’ve backed off of a rate hike now multiple times with any slight indication of economic weakness; so if we get to December and the global economy is still teetering on the brink of disaster, then we probably won’t be getting a rate hike then either.”

This provided enough reasonable doubt with just enough confidence (from their more hawkish forecast) for markets to continue their rally.

But things got real last Friday, when a blowout NFP report made that December rate hike actually look like it’s probable. The Fed has used the linchpin of ‘data dependency’ as their argument towards rate hikes for the past six years, saying that when the data is strong enough, they will hike. Last Friday’s NFP print will be hard to ignore under that premise, and rate expectations for December have moved up.

(click below for larger image)

Created with Marketscope/Trading Station II; prepared by James Stanley

But perhaps more troubling – stock prices have moved down somewhat aggressively. This can be vexing for traders because the Fed has constantly been changing their tune. In actuality, they don’t know what they want to do. There is no historical example for where we’re at, and nobody really knows how badly a rate hike may impact the global economy.

The elephant in the room is the scope of policy. Put yourself in the position of someone that will be retiring in the next 10 years. Logically speaking, you don’t want your retirement portfolio in 100% stocks, because that would probably lead to too much volatility for any retirement scenarios. More likely, you’re going to embark on an asset allocation model that sees a lower percentage of stocks and a higher percentage of bonds the effort of decreasing the volatility of your retirement funds. After all, who wants to lose their entire retirement account by investing in a pets.com or an eToys.com?

But, if you’re close to retirement right now and you need bonds, what are you to do? Rates are really low, so you’ll be looking at lackluster returns on your portfolio, so you need to take on slightly more risk right now than you normally would to account for those lower rates. But – if you invest in all bonds, now you’re basically looking at a prolonged period of pain – as rising rates mean that bond prices go down, because those 2% and 3% coupons you’d have to buy today look utterly unappealing when rates move up to 5 or 6%. So if you buy that low-yielding bond today, you’re sitting under-water (in a losing position) in a rising rate environment. So that’s not a good idea.

So what is an investor to do? Buying bonds exposes you to a rising rate cycle that could last 10-20 years (throughout most of your retirement), and buying stocks exposes you to massive swings, not unlike we saw in August when the S&P went down by over 10%. Realistically, we could see stocks get a haircut of 20-30% by the end of next year should the panic theme continue to develop, which it certainly can given the multiple pressure points being seen in the global economy. And while sitting on the sidelines while prices rise may be annoying, there aren’t many feelings in this world that are greater than being flush with cash with the ability to buy quality names like Google or Apple trading at multiples that are a fraction of where they’re at right now. I mean, not every company in this world can carry at 900x earnings multiple like Amazon is right now.

As an investor – you have to look at both the risk and reward. And arguably, the rewards right now are minimal. What type of top-side return might we expect on stocks? Maybe 5 or 10% more? We’re already at all-time highs. What is the down-side? Well, if August is any guide, it could be significant. On the bonds front – what is the upside of investing in bonds right now? 4% or 5% coupons? Coupons that, again, will be worth far less in a rising rate environment, which no matter how you cut it, the Fed is wanting to make happen, whether it starts in December or March or even 2017. Buying any long-term bond exposes you to something that you KNOW will happen at some point. So again, the reward doesn’t warrant the risk.

In the six years since the Financial Collapse, we’ve seen the Fed roll out a ton of new measures in an effort of shoring up the economy. The one thing that we know is that many of them did not work, and some of them may have helped. But we don’t yet know which are which, and this whole prospect of forward guidance, while logically beneficial during a painfully down-trending market, has questionable benefits in the ‘normal environment’ that the Fed is striving so hard to bring back.

One thing that the Fed has done successfully has been providing a confusing environment for one of the largest sociological demographic groups in the world (US Baby-Boomers) as they enter retirement. If you’re an investor looking to retire in the next 10 years, and if you’d ridden the last six years of QE-fueled gains in your retirement portfolio, would you really want to wait around for another 2000-like, or 2007-like collapse? Would you really want to lock yourself into a bond that would likely be trading at 80% or 90% of its par value in three years?

Probably not: This is an environment where cash looks optimal. Not too indifferent than the Great Depression. The Fed has successfully coagulated the market to a degree of confusion so grand that even the riskiest of investors should take caution.

--- Written by James Stanley, Analyst for DailyFX.com

To receive James Stanley’s analysis directly via email, please SIGN UP HERE

Contact and follow James on Twitter: @JStanleyFX