Talking Points:

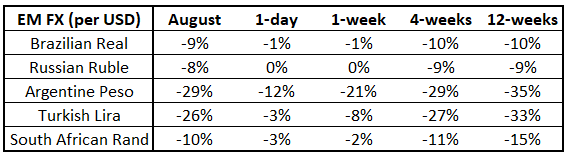

- The BRATS - Brazil, Russia, Argentina, Turkey, and South Africa - have all seen their currencies slump by at least -8% in August.

- Concerns over trade wars, lower expectations for global growth, and the withdrawal of central bank stimulus have fed concerns over the stability of emerging market currencies.

- Issues in Argentina, Turkey, and South Africa likely to persist through September.

See our longer-term forecasts for the US Dollar, Euro, British Pound and more with the DailyFX Trading Guides

The US Dollar (via the DXY Index) is posting a modest turnaround on Thursday, once again driven by factors away from its shores. A shallow pullback by equity markets is helping the dollar post only its second gain in the past ten sessions, as it continues to behave as a quintessential safe haven currency (rallying when stocks fall, falling when stocks rally).

Although US economic data this week has remained positive - earlier today, the August US Core PCE reading showed the Fed's preferred gauge of inflation back at its +2% medium-term target for the first time since April 2012 - the US Dollar rally has nothing to do with the Federal Reserve's rate hike timeline. There is a strong argument to be made that US Dollar price action since mid-June has been largely disconnected from speculation on the Fed's rate hike timeline.

DXY Index Price Chart: Daily Timeframe (January to August 2018) (Chart 1)

Instead, as was the case driving the US Dollar's early-August surge, the major factor today is the revival of concerns over emerging markets, particularly among those that share some less-than-appealing qualities: high inflation, elevated external debt-to-GDP ratios, current account deficits, and/or political instability are (among others) the hallmarks of a currency on the verge of facing a crisis. Enter the BRATS.

Like the European PIIGS, the emerging market BRATS are those countries that share the aforementioned qualities that put their currencies on the path to crisis. Whatever calm may have transpired in recent weeks was seemingly wiped out today with several key developments:

- the Argentinian Peso is now down nearly -30% month-to-date after Argentinian President Mauricio Macro asked the IMF to release $50 billion in loans, followed up by the central bank raising its key rate to 60% (the Fed's key rate is 2-2.25%, for comparison)

- the Turkish Lira is now down over -26% month-to-date after reports emerged that the central bank's deputy governor, Erkan Kilimci, would be leaving his post, a sign that the government is taking more steps to tighten its grip on monetary policy (markets prefer central banks independent of political considerations)

- the South African Rand is now down over -10% month-to-date after a goverment spokesperson said that the government could "collapse" if reforms are not taken up at a fast enough pace

Performance of BRATS versus US Dollar (Table 1)

There are two key takeaways from today's price action. First, the mid-month calm that we saw in emerging market FX was misleading; volatility is indeed here to stay. Second, the longer these emerging market currencies stay weak, the greater the likelihood of crises developing down the road. At the current exchange rates (particularly for USD/ARS and USD/TRY), it's only a matter of time before defaults occur and financial insitutions start eating losses - fully expect focus to remain on emerging markets throughout September.

Accordingly, we should learn soon as to whether or not the European Central Bank will be forced to alter its preordained policy path (ending QE in December 2018, hiking rates by "summer 2019") in order to help shore up an overly-exposed European banking system, or if the Fed will back off its current plans for gradual rate hikes over the next year (25-bps hikes priced-in for September 2018, December 2018, and June 2019).

Read more: USD/TRY Sustains Incredible Gains - What EM Currency Could Be Next?

FX TRADING RESOURCES

Whether you are a new or experienced trader, DailyFX has multiple resources available to help you: an indicator for monitoring trader sentiment; quarterly trading forecasts; analytical and educational webinars held daily; trading guides to help you improve trading performance, and even one for those who are new to FX trading.

--- Written by Christopher Vecchio, CFA, Senior Currency Strategist

To contact Christopher Vecchio, e-mail cvecchio@dailyfx.com

Follow him on Twitter at @CVecchioFX