Talking Points:

- Gold, the 10-year US Treasury yield, and the Japanese Yen have all moved in lockstep for the past three months.

- Meanwhile, US Dollar weakness is providing cover for otherwise weak currencies like the British Pound and New Zealand Dollar.

- Retail crowd positioning has blown back out to extreme levels in USD-pairs once again.

Upcoming Webinars for Week of August 27 to September 1, 2017

Tuesday at 9:45 EDT/13:45 GMT: Live Event Coverage: US Consumer Confidence (AUG)

Wednesday at 6:00 EDT/10:00 GMT: Mid-Week Trading Q&A

Thursday at 7:30 EDT/11:30 GMT: Central Bank Weekly

See the full DailyFX Webinar Calendar for other upcoming strategy sessions

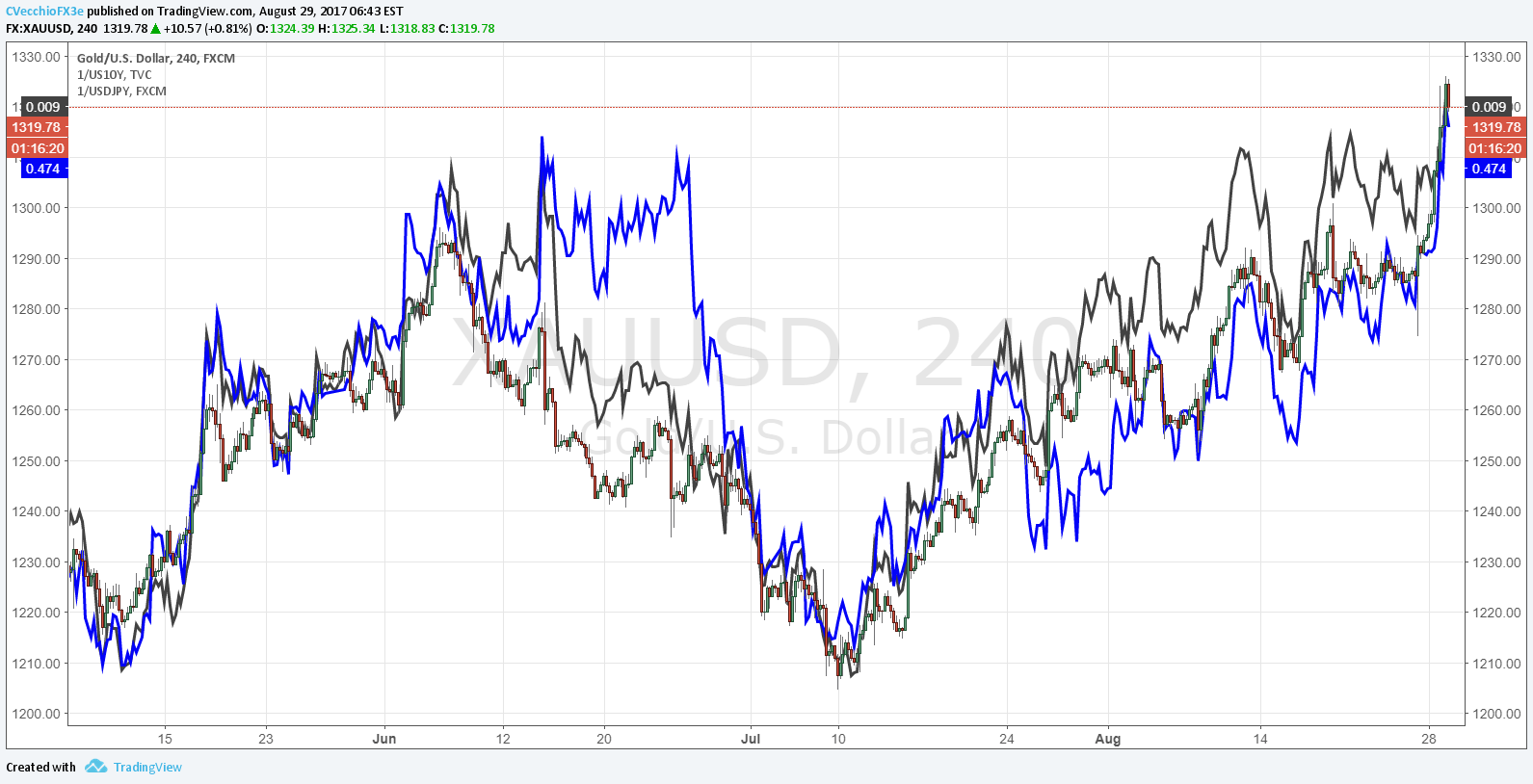

The US Dollar (via DXY Index) fell to fresh yearly lows today, and its lowest level since January 2015, as a North Korea missile test over Japan sparked a fresh shift to safe haven assets across the globe. With investors seeking shelter in US Treasuries, US yields have fallen; and, given the strong relationship among US yields, Gold, and the Japanese Yen in recent months, it's no surprise that Gold and the Yen are doing quite well today.

Chart 1: Gold versus USD/JPY (inverse) versus 10-year US Yield (inverse) 4-hour Timeframe (May 7 to August 29, 2017)

The 10-year US Treasury yield is at its lowest level since mid-June, and with it, US real yields have fallen as well. Real yields are inflation-adjusted yields: in this case, the US Treasury 10-year yield minus the core inflation rate. Why does this matter? Investing is all about asset allocation and risk-adjusted returns. On the risk-adjusted side, for example: if asset X has an expected return of 10% with a standard deviation of 8%, and asset Y has an expected return of 12% with a standard deviation of 15%, asset X is the superior choice given the risk trade-off.

On the asset allocation side, it’s about achieving required returns given the investor’s wants and needs. If inflation expectations are rapidly increasing, you would expect to see fixed income underperform: why would you want to have a fixed return when prices are increasing? On a real basis, your returns would be lower than otherwise intended.

Falling US real yields means that the spread between Treasury yields and inflation rates are decreasing, decreasing the penalty for holding a low yielding asset. If Gold yields nothing, has an estimated cost of carry of -2.4%, and only can return capital appreciation, it would best suited to rally when US real yields fell.

Accordingly, Gold is a desirable asset in a falling real yield environment, which is what we’ve been seeing develop over the past several weeks. The US 10-year real yield (Treasury yield minus core inflation) has fallen from 0.698% on July 7 to 0.411% today. This is a poor environment for the US Dollar to rally in, and as long as US real yields are dropping, Gold and the Japanese Yen can still outperform versus the US Dollar.

See the above video for technical considerations in the DXY Index, EUR/USD, GBP/USD, USD/JPY, GBP/JPY, EUR/GBP, the S&P 500, and Gold.

Read more: FX Markets Turns to Euro-Zone Inflation, Canadian GDP, US NFPs

--- Written by Christopher Vecchio, CFA, Senior Currency Strategist

To contact Christopher Vecchio, e-mail cvecchio@dailyfx.com

Follow him on Twitter at @CVecchioFX

To be added to Christopher's e-mail distribution list, please fill out this form