GOLD PRICE OUTLOOK:

- Gold prices coiling up in familiar range as traders ponder real rates outlook

- Speculation ahead of key November FOMC meeting might trigger a breakout

- October’s flash PMI data in focus near-term, downside surprise risk hinted

Gold prices continue to tread water in familiar territory as expected, anchored by static real interest rates. Nominal yields are on the rise thanks to a hawkish turn in the Fed policy outlook, which has in turn tracked surging inflation expectations. Recently however, the rise in price growth bets has outpaced nominal rates, capping real yields.

This seems to imply that markets expect the US central bank to fall behind the curve on curbing prices. Not surprisingly, that has kept gold afloat: traders have understandably reckoned that the 0% yield offered by bullion is a better store-of-value prospect than the negative return on cash.

A rethink may be in order. Fed Funds futures imply that markets now price in 130 basis points in tightening through the end of 2024. Chair Jerome Powell and company projected a more spirited 175 basis points in hikes over the same period at last month’s FOMC conclave however.

With this in mind, the spotlight may shift to speculation about the November 3 gathering of the rate-setting committee in the days ahead. It is expected to formally introduce the process of tapering back QE asset purchases, setting the stage for rates to rise in the second half of 2022.

Traders pondering hawkish surprise risk might look to rebalance portfolios accordingly in the days ahead, pressuring bullion. Lasting follow-through seems unlikely for now however, with directional conviction in short supply before policymakers’ guidance can be gleaned and properly onboarded.

October’s flash PMI surveys from the US, UK and Eurozone headline the data docket in the coming hours. Global economic news-flow has increasingly underperformed relative to forecasts recently, which may imply that analysts’ forecasts are rosier than reality supports and set the stage for downside surprises.

That might bode ill for gold if soft headline results come alongside indications of sticky price growth, which may in fact be amplifying the downshift in global output expansion since May. That mix might beckon swifter action from monetary authorities, pulling the metal lower within recent ranges.

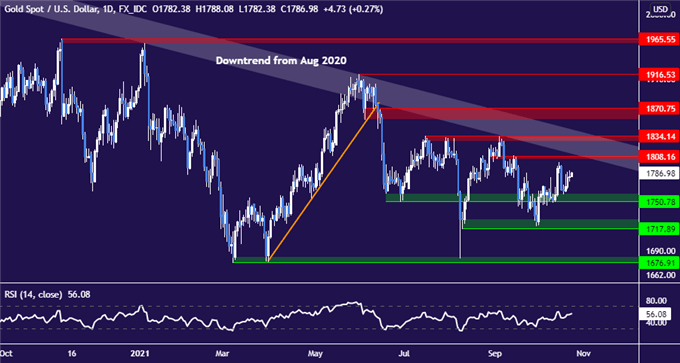

GOLD TECHNICAL ANALYSIS – BEARISH BACKDROP REMAINS DESPITE STICKY RANGE

Gold prices remain locked in familiar territory below the $1800/oz figure, though the bearish bias established from August 2020 remains intact. A break below support at 1750.78 may expose 1717.89 on route to the 2021 floor under $1700/oz. Resistance begins at 1808.16, followed by the range top at 1834.14. A daily close above that seems needed to make the case for upside follow-through.

Gold price chart created using TradingView

GOLD TRADING RESOURCES

- What is your trading personality? Take our quiz to find out

- See our guide to build confidence in your trading strategy

- Join a free live webinar and have your questions answered

--- Written by Ilya Spivak, Head Strategist, APAC for DailyFX

To contact Ilya, use the comments section below or @IlyaSpivak on Twitter