CRUDE OIL & GOLD TALKING POINTS:

- Commodity prices plunge amid reorientation to strong-USD bias

- Crude oil prices may fall further as markets eye OPEC+ meeting

- Gold prices unlikely to find lasting support amid trade war fears

Benchmark commodities plunged on Friday in a move that seemed to reflect a belated response to back-to-back monetary policy announcements from the Federal Reserve and the ECB. The former central bank struck a decidedly hawkish tone while the latter steered in the opposite direction even as it announced plans to unwind its QE asset purchase program.

The divergence made for a sharp US Dollar rally. More broadly, it marked the demise of the “catch-up” narrative envisioning top central banks chasing after the Fed’s hawkish lead amid broadening economic recovery. That this would shrink the greenback’s yield advantage accounted for most of its losses in 2017. Friday, repositioning for the alternative seemed to arrive for USD-denominated commodities.

CRUDE OIL PRESSURED BEFORE OPEC+ MEETING

Looking ahead, crude oil prices may continue to face selling pressure as all eyes turn to Friday’s OPEC+ meeting in Vienna. The gathering of cartel officials along with the representatives of like-minded producer countries – most notably, Russia – will take up the fate of a coordinated output cut regime they put in place to drain overstuffed inventories and boost prices.

The effort worked: global stockpiles are substantially diminished and prices rose nearly two-fold from the lows set in February 2016. Now, with political turmoil in Venezuela and the re-imposition of sanctions on Iran threatening supply disruptions, Saudi Arabia and Russia want to relax output curbs. Smaller but still influential suppliers like Iraq have balked.

That sets the stage for a contentious sit-down that will test the power of Riyadh and Moscow to direct market trends. If they succeed, the prospect of increasing output will probably pressure oil prices. If not, eroding confidence in their influence in the face of swelling swing supply from the US may push the WTI and Brent benchmarks downward all the same.

GOLD MAY STRUGGLE DESPITE TRADE WAR WORRIES

Meanwhile,a lull in top-tier economic news flow might see gold prices battered by risk sentiment trends. Trade war jitters have put markets in a dour mood at the start of the week. To the extent that this weighs on Treasury bond yields, the yellow metal might mount something of a recovery. Any gains may be capped however as the US Dollar reclaims its safe-haven credentials however.

See our guide to learn about the long-term forces driving crude oil prices !

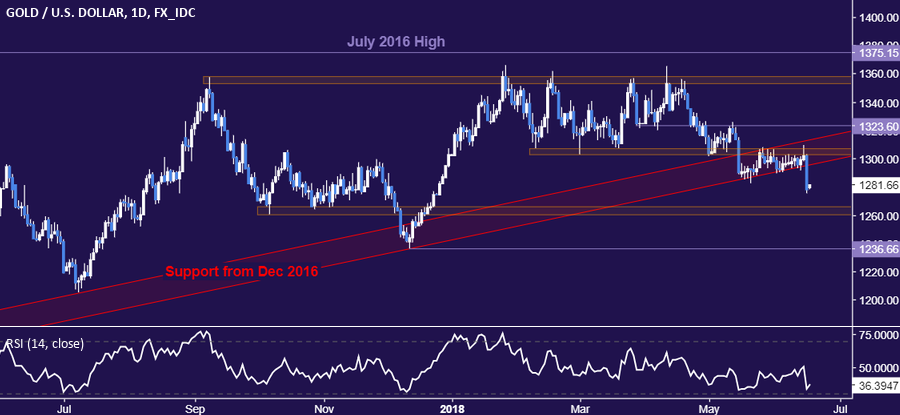

GOLD TECHNICAL ANALYSIS

Gold prices plunged through trend support guiding them higher since December 2016, exposing the next downside hurdle in the 1260.80-66.44 area. A further push below that targets the December 2017 low at 1236.66. Trend line support-turned-resistance is now at 1296.71.

CRUDE OIL TECHNICAL ANALYSIS

Crude oil prices sank through trend support in place since June 2017. From here, a daily close below the 63.96-64.26 area exposes the April 6 low at 61.84. Critical resistance needed to be overcome to negate the bearish bias stands in the 66.22-67.36 area.

COMMODITY TRADING RESOURCES

- Learn what other traders’ gold buy/sell decisions say about the price trend

- Having trouble with your strategy? Here’s the #1 mistake that traders make

- Join a Trading Q&A webinar to answer your commodity market questions

--- Written by Ilya Spivak, Currency Strategist for DailyFX.com

To contact Ilya, use the comments section below or @IlyaSpivak on Twitter