Central Bank Watch Overview:

- Russia’s invasion of Ukraine has provoked a dramatic pricing in rates markets for both the Bank of England and the European Central Bank over the past week.

- Rates markets are discounting the first rate hike from the ECB in September, while the odds of a 50-bps rate hike by the BOE in March have all but evaporated.

- Retail trader positioning suggests both EUR/USD and GBP/USD rates have a bearish bias.

The Best Laid Plans…

In this edition of Central Bank Watch, we’ll cover the two major central banks in Europe: the Bank of England and the European Central Bank. Both central banks have seen a dramatic repricing in rate hike expectations over the past week, solely due to Russia invading Ukraine, which threatens to upend the COVID-19 pandemic economic recovery. Whereas at the start of February focus was on when the BOE and ECB would raise rates, the question has emerged if either central bank will be able to move forward with normalization – at all.

For more information on central banks, please visit the DailyFX Central Bank Release Calendar.

BOE Hike Odds Narrow

Russia’s invasion of Ukraine has proved to be an accelerant to the pullback in BOE rate hike odds, initially catalyzed in early-February by BOE Chief Economist Huw Pill. On February 9, he noted that he worried “that taking unusually large policy steps may validate a market narrative that Bank policy is either foot-to-the-floor on the accelerator or foot-to-the-floor with the brake.” These comments were an attempt to dampen market expectations that the BOE would hike rates by 50-bps. At their peak in mid-February, rates markets were discounting greater than a 50% chance of a 50-bps rate hike in March.

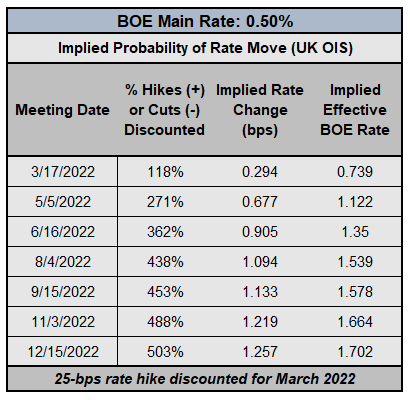

Bank of England Interest Rate Expectations (March 2, 2022) (Table 1)

The combined influence of the Russian invasion plus BOE Chief Economist Pill’s commentary has dashed speculation of a 50-bps rate hike significant. UK overnight index swaps (OIS) are discounting a 118% chance of a 25-bps rate hike in March (a 100% chance of a 25-bps hike and an 18% chance of a 50-bps hike). Assuming Russia’s aggression towards Ukraine doesn’t spill across other European borders, the spike in energy prices will still push the BOE to raise rates over the coming months, with 25-bps rate hikes priced-in for each of the three meetings following March.

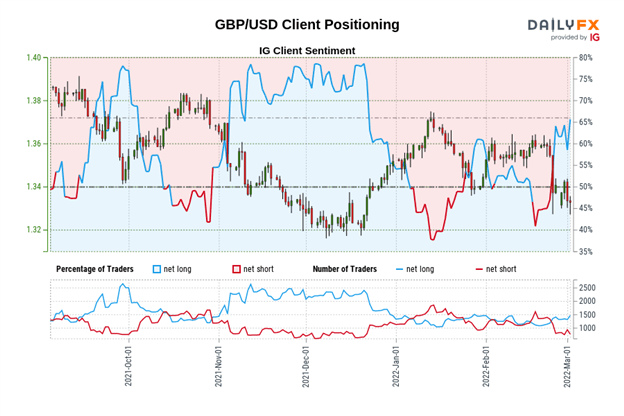

IG Client Sentiment Index: GBP/USD Rate Forecast (March 2, 2022) (Chart 1)

GBP/USD: Retail trader data shows 65.02% of traders are net-long with the ratio of traders long to short at 1.86 to 1. The number of traders net-long is 12.97% higher than yesterday and 16.49% higher from last week, while the number of traders net-short is 21.60% lower than yesterday and 39.72% lower from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-long suggests GBP/USD prices may continue to fall.

Traders are further net-long than yesterday and last week, and the combination of current sentiment and recent changes gives us a stronger GBP/USD-bearish contrarian trading bias.

Back to Reality

For several weeks, we’ve noted that “there still seems to be a disconnect between ECB policymakers and rates markets. Rates markets are expecting at least one rate hike in the first half of 2022, whereas several officials are still suggesting that the ECB will be slow to respond to excess inflationary pressures.” Russia’s invasion of Ukraine may be providing the cover ECB officials need to justify keep their asset purchase program in place through 3Q’22, and interest rates lower for longer; there is a non-zero chance that the EU and US sanctions on the Central Bank of Russia provokes a liquidity crunch for European banks.

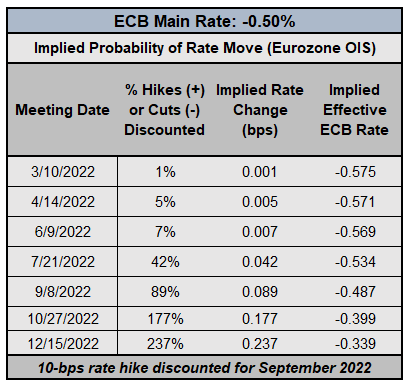

EUROPEAN CENTRAL BANK INTEREST RATE EXPECTATIONS (March 2, 2022) (TABLE 2)

Accordingly, rate hike odds have taken a significant step backwards over the past week. Eurozone OIS are discounting a 10-bps rate hike in September (89% chance), down from their February high of an 85% chance in June. €STR, which replaced EONIA, is priced for 20-bps of hikes through the end of 2022, and roughly 80-bps of hikes through the end of 2023. That said, there is growing reason to believe that the ECB doesn’t raise rates at all, which will further draw a juxtaposition between the ECB and other major central banks, weighing on the Euro.

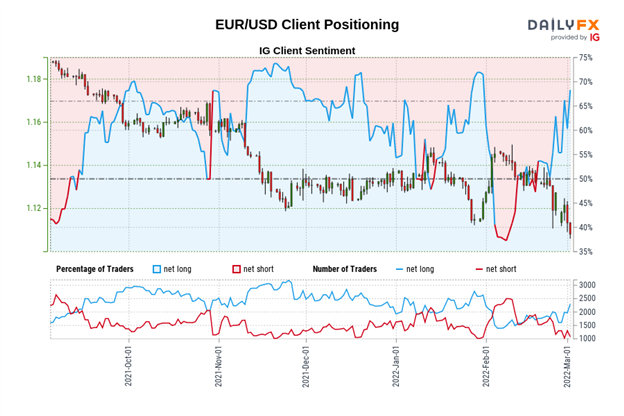

IG Client Sentiment Index: EUR/USD Rate Forecast (March 2, 2022) (Chart 2)

EUR/USD: Retail trader data shows 66.36% of traders are net-long with the ratio of traders long to short at 1.97 to 1. The number of traders net-long is 9.42% higher than yesterday and 29.62% higher from last week, while the number of traders net-short is 5.23% lower than yesterday and 35.77% lower from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-long suggests EUR/USD prices may continue to fall.

Traders are further net-long than yesterday and last week, and the combination of current sentiment and recent changes gives us a stronger EUR/USD-bearish contrarian trading bias.

--- Written by Christopher Vecchio, CFA, Senior Strategist