Weekly Fundamental Crude Oil Price Forecast: Neutral

- As the Russian invasion of Ukraine presses into its second month, there are no signs that energy supply chain concerns are going to abate.

- A new Iran nuclear deal could be reached in the coming days, but the impact of new energy supplies has been mostly discounted by markets.

- The IG Client Sentiment Index suggests thatcrude oil prices have a bullish trading bias.

Energy Prices Week in Review

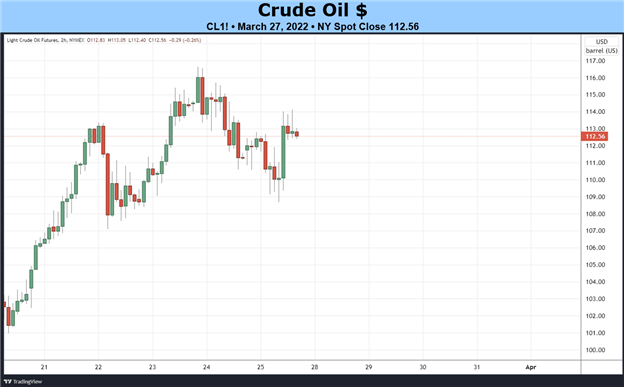

Volatility in energy markets is a feature of current trading conditions and likely won’t dissipate anytime soon. Having already traded in a 38% range over the past four weeks, crude oil prices swung higher last week, adding +10.5% to its second highest close of the year at 112.56/brl. Brent oil gained +17%, posting its highest close of 2022 and its highest since April 2012 at 120.21/brl. Elsewhere, natural gas prices tallied their highest close of 2022 and their highest since the end of September 2021 at 5.571 MMBtu, a gain of +14.6%.

Supply and Demand Concerns Seesaw

There are a litany of factors that are feeding into volatility across energy markets. The European Union’s proposed ban on Russian oil imports in response to the ongoing invasion of Ukraine has spurred concerns of even more constrained global energy supplies, to which OPEC has already warned against. Canadian officials have suggested that the country is able and willing to increase energy production to offset Russian supply losses, but questions remain over how quickly such a goal could be accomplished.

A new Iran nuclear deal may be on the verge of being completed, but given how long rumors have persisted that a deal was close to the finish line, one has to imagine that new oil supplies coming onto the market have more or less been priced-in already. Attacks on Saudi Arabian oil distribution facilities are doing no favors for quelling concerns that energy supplies are on stable footing, either.

The fact of the matter is that there are several stories unfolding in the energy space that could easily provoke more volatility across markets, none of which are likely to find any permanent resolution anytime soon.

Economic Calendar Week Ahead

The final week of March sees a generally lighter economic calendar from the world’s major economies, but several inflation reports will underscore the impact that higher energy prices are having on sustained higher price pressures around the globe. As is the case every week, and particularly of recent, mid-week energy inventories figures should prove among the most impactful for crude oil prices – beyond the headlines du jour.

- On Tuesday, March 29, the weekly US API crude oil stock change figures will be published.

- On Wednesday, March 30, the preliminary March German inflation rate report (HICP) will be released at 12 GMT. At 12:30 GMT, the final 4Q’21 US GDP report will be published. At 14:30 GMT, the weekly US EIA energy inventories data are due, with further drawdowns expected.

- On Thursday, March 31, the March Chinese NBS manufacturing PMI is set for release at 1:30 GMT. The final 4Q’21 UK GDP report is scheduled for 6 GMT. March German jobs data are due at 7:55 GMT. The Federal Reserve’s preferred gauge of inflation, the February US PCE report, will be published at 12:30 GMT.

- On Friday, April 1, the flash March Euroarea inflation rate report (HICP) will be released at 9 GMT. The March US nonfarm payrolls report and March US unemployment rate are in focus at 12:30 GMT. The March US ISM manufacturing PMI will be published at 14 GMT.

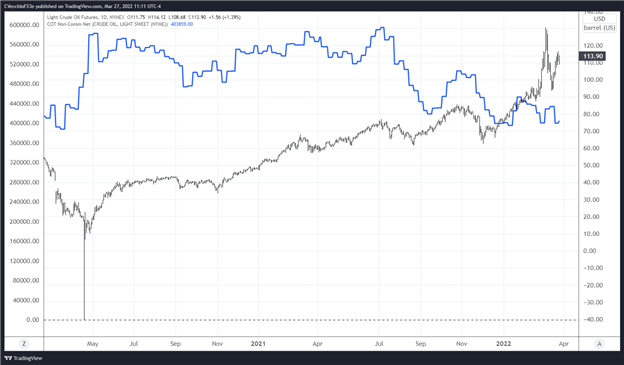

CRUDE OIL PRICE VERSUS COT NET NON-COMMERCIAL POSITIONING: DAILY TIMEFRAME (March 2020 to March 2022) (CHART 1)

Next, a look at positioning in the futures market. According to the CFTC’s COT data, for the week ended March 22, speculators increased their net-long oil futures position to 403,859 contracts, up from the 399,892 net-long contracts held in the week prior. Despite the volatility in energy prices – and in particular, the rapid gains seen – speculators have not increased their net-long positioning dramatically; net-longs are -32% below their high in July 2021.

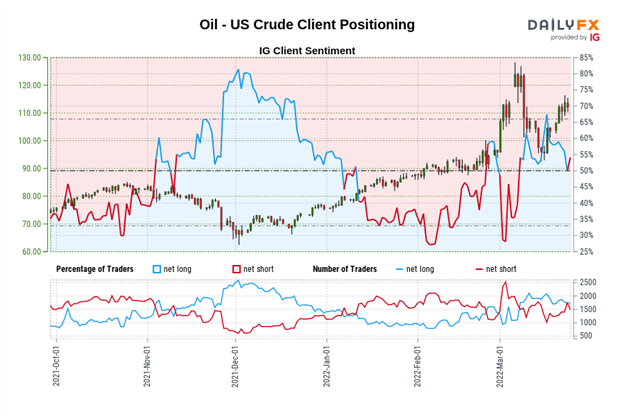

IG CLIENT SENTIMENT INDEX: CRUDE OIL PRICE FORECAST (MARCH 25, 2021) (CHART 2)

Oil - US Crude: Retail trader data shows 47.96% of traders are net-long with the ratio of traders short to long at 1.08 to 1. The number of traders net-long is 8.00% lower than yesterday and 14.62% lower from last week, while the number of traders net-short is 4.11% higher than yesterday and 26.93% higher from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-short suggests Oil - US Crude prices may continue to rise.

Traders are further net-short than yesterday and last week, and the combination of current sentiment and recent changes gives us a stronger Oil - US Crude-bullish contrarian trading bias.

Trade Smarter - Sign up for the DailyFX Newsletter

Receive timely and compelling market commentary from the DailyFX team

--- Written by Christopher Vecchio, CFA, Senior Strategist