US Midterm Elections Outlook:

- Unless gas prices drop further and US inflation rates pull back sharply, odds are that Democrats lose control of at least the House of Representatives to Republicans.

- The prospect of gridlock returning to Washington, D.C. has profound implications for the Federal Reserve and the US Dollar.

- The Federal Reserve could quickly become ‘the only game in town’ again, much like what happened from 2011 to 2016, and again from 2019 to 2020.

Gridlock Back in D.C.?

In How Record Inflation Will Impact US Midterms, we explored how record inflation could impact the US midterm elections this fall. We concluded that unless gas prices drop further and US inflation rates pullback sharply in the coming weeks, odds are that Democrats lose control of at least the House of Representatives to Republicans, bringing about a divided Congress and gridlock back to Washington, D.C.

Such a development will have profound implications for both US fiscal and monetary policy over the coming years, and directly impact the US Dollar, US equities, US Treasuries, gold prices, oil prices, and cryptocurrencies. All these impacts will flow through the Federal Reserve, primarily.

Turn Back the Clock

A walk down memory lane is necessary to grasp the potential earthquake coming to US policy – both fiscal and monetary – over the coming months.

In 2010, after former US President Barack Obama and a Democratic majority in the Senate and the House of Representatives passed The Affordable Care Act during the Global Financial Crisis, there was a wave of backlash from voters across the country. To save the banking system, housing market, and automobile industry, several rounds of federal government spending were announced to help stimulate the economy.

But the backlash was fierce as most American households continued to face financial difficulties and a weak labor market. The US unemployment rate was still near double digits as the housing market remained in shambles. The 2010 US midterm elections saw Democrats lose control of the House of Representatives. Gridlock arrived in Washington, D.C., as a divided Congress refused to push forward more government spending.

Gridlock was the defining feature of the next few years. Republicans, emboldened by their gains in the 2020 US midterm elections, demanded budget austerity to reign in government spending. Bickering ensued, leading to budget sequestration and the US losing its AAA credit rating from Standard & Poor’s in August 2011. By 2014, midway through former US President Obama’s second term, Democrats lost control of the Senate.

While the federal government was effectively paralyzed by a divided Congress, and then with a Democrat in the White House while Republicans controlled all of Congress, there was only one game in town to help provide support for the US economy: the Federal Reserve.

Fed Policy During Gridlock

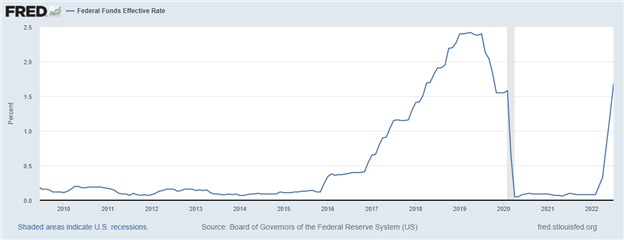

From 2011 to 2016, a paralyzed federal government unable to pass any additional stimulus left the Federal Reserve with few options: raise interest rates and snuff out the nascent post-Global Financial Crisis recovery; or keep interest rates near zero and hope that the US economy continued to recover. The Federal Reserve chose the second option:

The 2011 to 2016 period was not the only time with gridlock in Washington, D.C. in recent years. The same can be said of the 2019 to 2020 period during former US President Donald Trump’s sole term. Limited federal government spending until the coronavirus pandemic meant that the Federal Reserve had to back away from its interest rate hike cycle, bringing forth rate cuts to help buoy asset prices. Even when Congress passed its coronavirus stimulus packages, the Federal Reserve lowered its main rate to 0.00-0.25% again while restarting asset purchases.

Implications for US Midterms

If the 2022 US midterm elections deliver gridlock in Washington, D.C. – Republicans controlling just the House or both chambers of Congress while a Democrat is in the White House – it means that the Federal Reserve will quickly become the only game in town once more.

Should US inflation rates subside over the next few months, which would have nothing to do with the composition of the Congress, it means that the Federal Reserve may tack back to preventing a more significant economic downturn, something that is already on its radar now that the US economy has contracted for two consecutive quarters.

If the Federal Reserve does shift gears and move towards interest rate cuts, and at the extreme, reinstitutes asset purchases once more to incentivize investors to change their risk preferences (thereby reducing yields on safer assets, forcing allocation to riskier, growth-sensitive assets) the impact will likely be no different than what happened from 2011 to 2016 or from 2019 to 2020. Such a shift portends a weaker US Dollar; lower US Treasury yields; higher gold prices; higher oil prices; higher cryptocurrency prices; and a float higher by US equity markets.

Trade Smarter - Sign up for the DailyFX Newsletter

Receive timely and compelling market commentary from the DailyFX team

--- Written by Christopher Vecchio, CFA, Senior Strategist