I normally take a systematic approach to these top trade installments. With a heavy focus on FX I’ve found a system that works for me. See, most of the time when I’m working with FX I’m following major pairs, like EUR/USD or AUD/USD. In many cases, I’m looking to hedge some element of risk while focusing my exposure in somewhat of a calculated manner. For top trades, I’ll often look at cross pairs as the themes that I’ve been working with in majors can often filter out into longer-term opportunity in a cross. So like GBP/JPY, for instance, from Q4 of last year. I was basically just looking to play the strength trend in GBP against the expected weakness that I was pricing-in for JPY and, rather than setting up GBP/USD and USD/JPY separately, just cut-out the middle man and go right for GBP/JPY. My Top Trade from Q1 of this year was far simpler, just bullish USD as I saw a burgeoning confluence of fundamentals and techs that were difficult to ignore.

For this quarter, however, there’s really only one area that I want to look at for a top trade and that’s equity weakness, specifically in the Nasdaq 100 and the S&P 500.

I know that the fear from rate hikes appears to be overplayed. The Fed, after all, does get to choose how quickly to hike rates. And when this has been an issue in the past, they’ve erred on the side of caution and equity strength. And even today, stocks have still continued to trade with strength amidst a number of worrying factors that market participants appear to just be shrugging off. And, in reality, this isn’t all too different from the past 13 years, is it? Ever since the Global Financial Collapse it’s felt like one crisis after the other. It feels like there’s been a million reasons for stocks to crater and yet, bears have faced a constant stream of disappointment as equities have put in a historic run over the past decade-plus.

But, I’m going to evoke one of the most dangerous phrases in financial markets and something that I rarely say, if ever: I think this time is different.

What’s different this time is the Fed. We haven’t really had to worry about inflation since the 1970’s, before my lifetime. And while the Fed was careful with QE right after the implosion of the banking sector on the back of housing in 2008, a lack of inflation allowed them to get really aggressive with policy. So much so that markets had a difficult time operating without it, even in times of positive economic headwinds, such as 2018.

But after Covid and armed with the lack of fear from employing QE for a decade without too much direct negative impact, the Fed went really wild and didn’t even start to reign that in before it was far too late. Inflation has spiked and this is something that has caught the Fed off guard even though they continued to say that inflation was transitory throughout last year. And now they have to play catch up.

Just as the Fed has started to hike interest rates in effort of arresting 40-year high inflation rates, there’s another major problem on the horizon and that brings even more inflation potential from the spike in raw materials that’s emanated from the Russian invasion of Ukraine. The global economy had become quite dependent on free trade and relatively open flow of commerce. That no longer exists, and add to that a bit of antagonism that can create even more problems; like Russia blocking ships carrying wheat which creates and even larger supply crunch. From an economic point of view, it does feel like we’re already in a Cold War 2.0 and the undoing of trade ties is unlikely to bring much benefit to either side. This can create an even sharper trend for inflation.

And all of this really spells one thing: The Fed put seems dead, or at least it feels dead until a thousand handles is shed from the S&P 500. And this would, technically, be the first time that it’s really happened in such a manner since the global financial collapse. There’s even been comments from Fed members about engineering a ‘soft landing,’ which sort of sounds like they want stock prices to come down from current valuations.

In summation – inflation is out of control and we’re on the verge of or, perhaps, already in the midst of an economic war with another nuclear power whom the world depended on for trade. This can lead to a food shortage around the world which can put even more pressure on the world’s most disadvantaged nations and people. This can give rise to further conflict, such as the Arab Spring that began in 2010. And the Fed, who has been very supportive through a number of economic ills over the past 13 years, doesn’t have the ability to support markets in the way that everyone has become accustomed to. They’re going to have to hike and this will only increase the pressure.

Collectively, this points to both US Dollar strength and equity weakness. USD strength was my top trade for Q1 of 2022 and I think the short equity idea can get more run, it’s also the more challenging backdrop; so I’m going with short stocks for my Q2 2022 Top Trade.

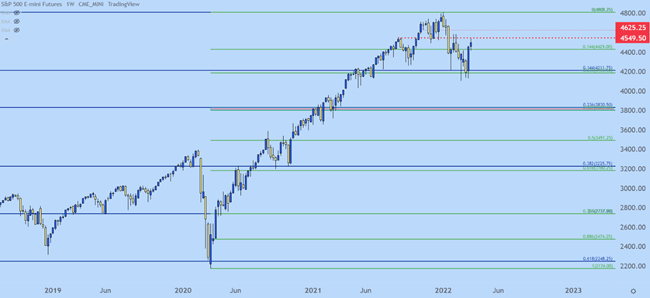

S&P 500

At this point the S&P 500 has retraced as much as 23.6% of the pandemic trend. The index could theoretically peel down to the 38.2% retracement of that same major move whilst still retaining some longer-term bullish qualities. This area projects to around 3800, and at that point the drawdown from the January high would hit the 20% bear market territory number. This seems a reasonable support target for pullback themes in the S&P 500.

S&P 500 Weekly Price Chart

Chart prepared by James Stanley; S&P 500 on Tradingview

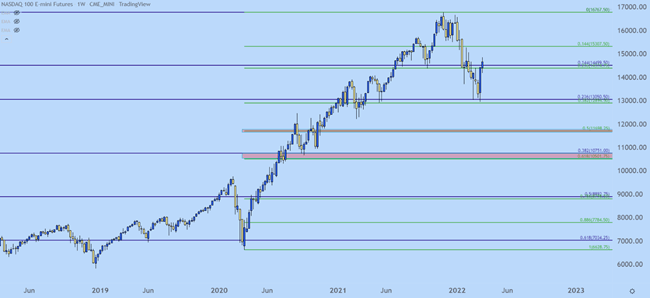

Nasdaq 100

The Nasdaq 100 has already had a trip into ‘bear market territory’ albeit a quick trip. The index traded below the -20% drawdown marker for a short period of time in Q1 and that compares with the max drawdown in the S&P 500 of -14.69%.

If the rates theme is going to push a larger correction, I still like the Nasdaq for greater bearish potential than the S&P 500 and I think we could see a larger sell-off here.

The 50% marker of the pandemic move is around 11,700 and this would be a total drawdown of 30% from the all-time-high set in January. And there’s a larger zone of interest that’s a bit a bit deeper, from around 10,501 to 10,750. This would be a 35% drawdown from the November high and if we’re in a true correction type of theme, that sounds like not a completely unreasonable support target, although something like that may take some time to build so it may not end up showing up until the second-half of this year in a larger overall market correction.

Nasdaq 100 Weekly Price Chart

Chart prepared by James Stanley; Nasdaq 100 on Tradingview

Trade Smarter - Sign up for the DailyFX Newsletter

Receive timely and compelling market commentary from the DailyFX team