US Recession Watch Overview:

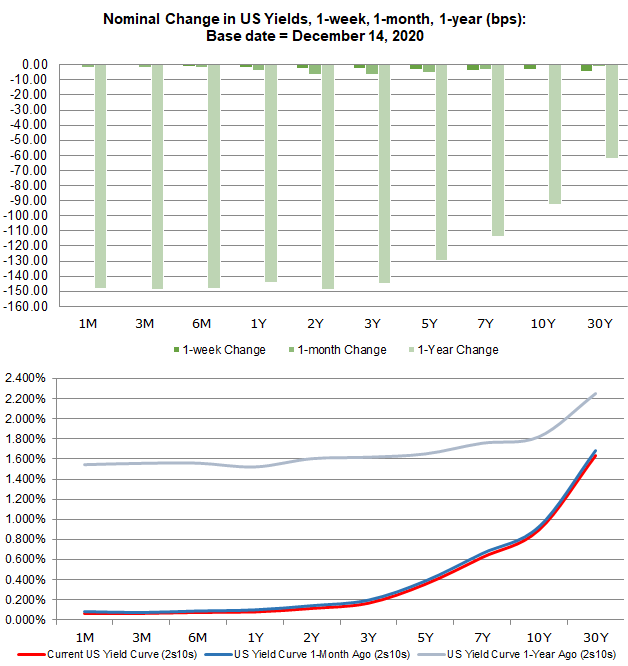

- The US Treasury yield curve has steepened in recent weeks (long-end rates rising faster than short-end rates), but that might not mean that the US economy is out of the woods from the coronavirus pandemic.

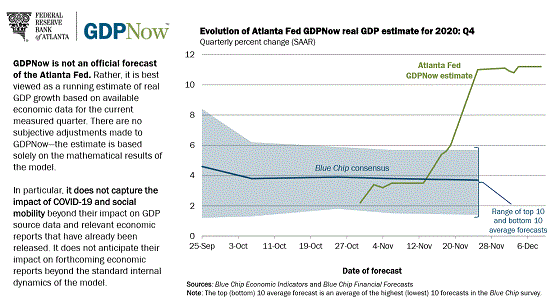

- Q4’20 Atlanta Fed GDPNow projects an +11.2% real quarterly growth rate, but data momentum is slowing, and it’s possible that failure by the US Congress to agree to fiscal stimulus will handicap the economy in Q1’21.

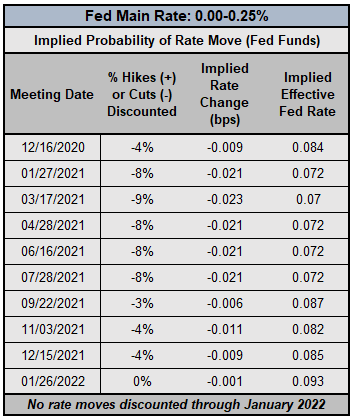

- Traders continue to anticipate no change in interest rates by the Federal Reserve through January 2022; the Fed has promised to keep rates low through 2023.

Making Sense of US Economic Data

The US economy is in the midst of a record-setting recovery, or is about to fall back into recession – depending upon who you ask. Timeframe matters. With only a few weeks left in Q4’20, it appears that another strong quarter is in the books: the Atlanta Fed GDPNow growth tracker is suggesting that we could see a real quarterly growth rate around +11.2%, per available data through December 9. Amid the initial coronavirus vaccine deployments, the US Treasury yield curve is at its steepest place in weeks.

And yet, something is amiss. US economic data is moving in the wrong direction. The Citi Economic Surprise Index, a gauge of economic data momentum, is currently sitting at +75.8, down by more than -72% from its high set in July at +270.8. For the first time since early-October, US initial jobless claims are back above 800K per week. The November US jobs report was much weaker than anticipated.

Atlanta Fed GDPNow Q4’20 US GDP Estimate (December 14, 2020) (Chart 1)

The trope “winter is coming” may be overused, but its an apt turn of phrase here. The window with which to positively impact Q1’21 GDP is slowly closing as US political leaders remain stuck in gridlock in Washington, D.C. Hopes of a ‘blue wave’ have floundered, and along with them, faith in a signficant fiscal stimulus package during the interregnum.

Instead, the US Congress can barely pass a budget to keep the lights on for more than a week. The fiscal spending package, if it comes together, looks like it will clock in around $900 billion at the high end, a far cry from the $2 trillion that President-elect Joe Biden was promising on the campaign trail (although, if Senate Democrats pull out a miracle in Georgia, that big stimulus push may come after all; stay tuned).

Fed May Be Influencing Price Action

The December Fed policy meeting set to conclude on December 16 brings about the potential for another adjustment to their stimulus program, given that we will see the quarterly Summary of Economic Projections. While a coronavirus vaccine deployment may be reducing risk over the long-run, the upfront economic outlook has soured. But that doesn’t necessarily mean that the Fed will act again.

Federal Reserve Interest Rate Expectations (December 14, 2020) (Table 1)

With no negative rates on the horizon and a FOMC that has said explicitly that interest rates will be low through 2023, it may be the case that traders have pushed up US yields – steepening the yield curve – in anticipation over forthcoming disappointment on the policy front. Expectations for an enhancement to the Fed’s QE program have subsided; it was previously anticipated that a shift to buying more long-dated bonds might occur in December. As this expectation of a major buyer in bond markets has subsided, prices have fallen, and yields have risen.

Using the US Yield Curve to Predict Recessions

The US Treasury yield curve remains normalized – long-end yields are higher than short-end yields – but we maintain that the yield curve is not an accurate reflection of the state of the US economy. Historically, the relatively faster rise by long-end yields compared to short-end yields occurs during times of expected economic expansion, so traders may be prone to interpret the yield curve movements as a sign that market participants believe that the worst period of uncertainty around the coronavirus pandemic is over.

US Treasury Yield Curve: 1-month to 30-years (December 14, 2020) (Chart 2)

The Fed’s efforts to flood the market with liquidity have depressed short-end yields, helping keep intact an artificially steep of the US yield curve. The degradation of US economic data momentum coupled with the alarming surge in COVID-19 cases, in aggregate of daily tests, deaths, and hospitalizations, suggests that the US yield curve is lying, again. That the US yield curve is steepening and the net-result is a weaker US Dollar is a major red flag that something is amiss.

After all, that sounds a lot like a sovereign debt problem akin to what was seen during the height of the Eurozone crisis, no? The soundbites at the time were, “Italian/Spanish/Portuguese yields spike, Euro falls.” Time will tell if the US yield curve is not signaling higher growth, but instead risk of sovereign credit stress.

A Refresher: Why Does the US Yield Curve Matter?

Market participants use yield curves to gauge the relationship between risk and time for debt at various maturities. Yield curves can be constructed using any debt, be it AA-rated corporate bonds, German Bunds, or US Treasuries.

A “normal” yield curve is one in which shorter-term debt instruments have a lower yield than longer-term debt instruments. Why though? Put simply, it’s more difficult to predict events the further out into the future you go; investors need to be compensated for this additional risk with higher yields. This relationship produces a positive sloping yield curve.

When looking at a government bond yield curve (like Bunds or Treasuries), various assessments about the state of the economy can be made at any point in time. Are short-end rates rising rapidly? This could mean that the Fed is signaling a rate hike is coming soon. Or, that there are funding concerns for the federal government. Have long-end rates dropped sharply? This could mean that growth expectations are falling. Or, it could mean that sovereign credit risk is receding. Context obviously matters.

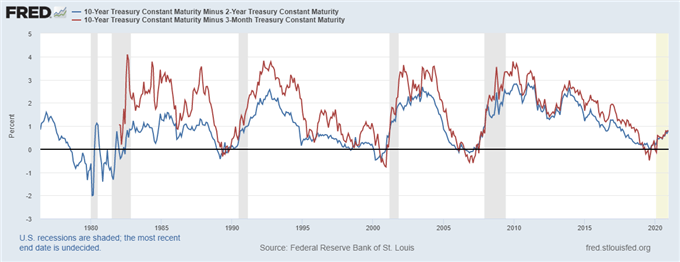

US Treasury Yield Curves: 3m10s and 2s10s (1975 to 2020) (Chart 3)

There is an academic basis for yield curve analysis. In 1986, Duke University finance professor Campbell Harvey wrote his dissertation exploring the concept of using the yield curve to forecast recessions. Professor Campbell’s research noted that the US yield curve needs to invert in the 3m10s for at least one full quarter (or three months) in order to give a true predictive signal (since the 1960s, a full quarter of inversion has predicted every recession correctly).

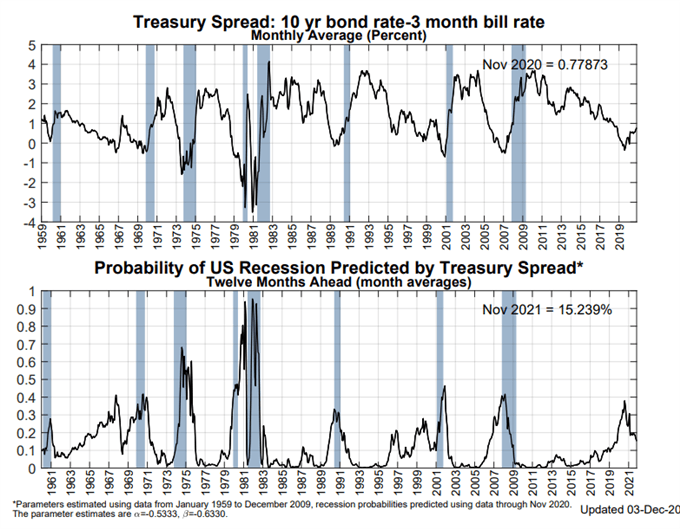

NY Fed Recession Probability Indicator (December 14, 2020) (Chart 4)

In aggregate, there is currently a 15.2% chance of a US recession in the next 12-months, per the NY Fed Recession Probability Indicator. This tracker never eclipsed 40% during the spring, even as Q2’20 GDP was literally the worst quarter in US economic activity. Once more, the US yield curve is hiding the truth, masking what will likely be more weakness in Q2’21.

--- Written by Christopher Vecchio, CFA, Senior Currency Strategist