US Dollar, Singapore Dollar, Indonesian Rupiah, Malaysian Ringgit, Philippine Peso – Talking Points

- US Dollar losses slowed against ASEAN currencies this past week

- Rising Covid cases in the US, fiscal stimulus woes remain key risks

- ASEAN data: Indonesian and Philippine central banks are on tap

US Dollar ASEAN Weekly Recap

The anti-risk US Dollar cautiously weakened this past week as ASEAN currencies, like the Singapore Dollar and Philippine Peso, slightly outperformed. Their 5-day performance, on the chart below, saw strength slow compared to the previous week. Then, Emerging Market assets rejoiced Joe Biden’s projected win for the White House over incumbent Donald Trump as investors priced in calmer waters ahead for foreign policy. A notable standout last week was the Indian Rupee in the South Asia region. USD/INR gained alongside the Nifty 50 as India’s government announced an INR9 trillion fiscal package.

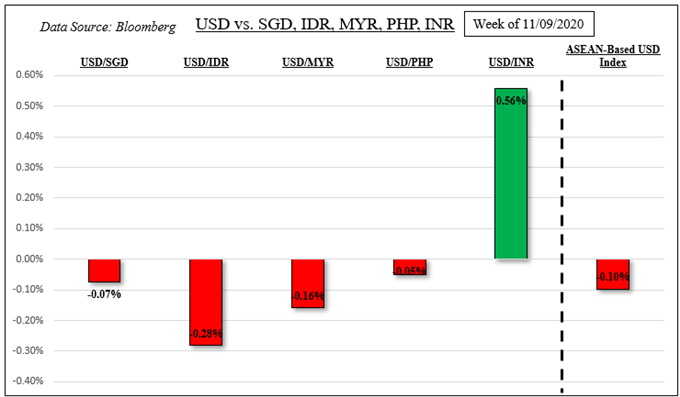

Last Week’s US Dollar Performance

*ASEAN-Based US Dollar Index averages USD/SGD, USD/IDR, USD/MYR and USD/PHP

External Event Risk – Covid Cases, US Fiscal Stimulus Woes and Retail Sales Data

There is welcoming news for global growth and ASEAN currencies, which are sensitive to external factors. Investors rejoiced when Pfizer reported that their Covid vaccine was 90% effective in containing the disease. More updates from other trials may send USD/SGD, USD/IDR, USD/MYR and USD/PHP lower. White House adviser Dr. Moncef Slauoui noted that vaccines could be in use by December if approved by the FDA.

However, this is as local coronavirus cases and hospitalizations hit record highs and at an exponential pace. That has opened the door to isolated lockdowns to help contain the spread. Meanwhile, ongoing gridlock between policymakers around another fiscal package likely means that it won’t arrive until early next year. These could keep ASEAN currencies under pressure.

An external factor that may keep risk appetite intact is Brexit talks. Last week, UK PM Boris Johnson’s top aide, Dominic Cummings, resigned and will step aside by the end of the year. This could be a sign that the two sides are inching closer towards a deal than previously expected. That would end up clearing another element of uncertainty in a highly-uncertain environment.

Meanwhile, University of Michigan Sentiment unexpectedly dipped last week. In fact, the Citi Economic Surprise Index tracking the US dipped to its lowest since early June and around pre-Covid levels. This shows that the level of rosy surprises compared to economists’ expectations have been fading considerably since the peak in July. This may open the door to disappointing local retail sales on Tuesday, denting sentiment.

ASEAN, South Asia Event Risk – Bank of Indonesia, Philippine Central Bank

In the ASEAN region, the Indonesian Rupiah and Philippine Peso are eyeing interest rate decisions from their associated central banks. They are on tap for Thursday. The Bank of Indonesia is anticipated to hold its 7-day reverse repo rate unchanged at 4%. It should be noted that the central bank hinted that there is room to ease further back in October, adding that the timing would depend on global developments.

Policymakers may reiterate commentary about an undervalued IDR and continue upholding efforts to support it. For USD/PHP, the Philippine Central Bank (BSP) is also anticipated to maintain its overnight borrowing rate unchanged at 2.25%. October’s inflation report unexpectedly surprised to the upside, and may keep the BSP on the sidelines, keeping PHP focusing on external risks.

For USD/SGD, there is a chance that finalized third-quarter Singapore GDP could cross the wires. However, the exact date and time is unspecified, with the window ranging between November 18th and the 25th. The country’s Straits Times Index (STI) recently surged 12 percent, benefiting from the rotation trade sparked by hopes of a Covid vaccine. More of the same may keep USD/SGD under pressure.

The ASEAN For other data on, check out the DailyFX economic calendar.

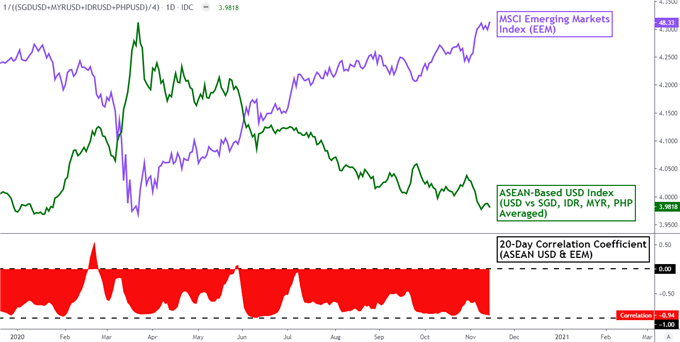

On November 13th, the 20-day rolling correlation coefficient between my ASEAN-based US Dollar index and the MSCI Emerging Markets Index rose to -0.94 from -0.86 from last week. Values closer to -1 indicate an increasingly inverse relationship, though it is important to recognize that correlation does not imply causation.

ASEAN-Based USD Index Versus MSCI Emerging Markets Index – Daily Chart

Chart Created Using TradingView

*ASEAN-Based US Dollar Index averages USD/SGD, USD/IDR, USD/MYR and USD/PHP

-- Written by Daniel Dubrovsky, Currency Analyst for DailyFX.com

To contact Daniel, use the comments section below or @ddubrovskyFX on Twitter