ASEAN Fundamental Outlook

- US Dollar mixed vs ASEAN FX such as SGD, IDR, MYR and PHP

- US-China trade deal boosting emerging markets and capital flows

- On the other hand, 2020 Federal Reserve rate cut bets are fading

US Dollar and ASEAN FX Weekly Recap

The US Dollar edged cautiously higher this past week and some of its strength flowed into ASEAN and emerging market Asia currencies. The Malaysian Ringgit and Philippine Peso weakened as the Singapore Dollar and Indonesian Rupiah held their ground. Sentiment improved in the aftermath of the US-China “phase one” trade agreement after the two countries withheld from raising tariffs against each other, as expected.

Simultaneously, the outlook for easing from the Federal Reserve in 2020 has been fading. The markets are the least-dovish since March with one rate cut no longer being fully priced in for next year. As a result, ASEAN FX are increasingly contending with a delicate balance between prospects of not-as-lose lending conditions and optimism that perhaps global growth could be revived. What could these expect into the new year?

For timely updates on ASEAN currencies, make sure to follow me on Twitter here @ddubrovskyFX

ASEAN FX Vs Emerging Market Index

The close inverse relationship between my ASEAN-based US Dollar index and the MSCI Emerging Markets Index (EEM) remains strong. The 20-day rolling correlation is now at -0.86 where a value at -1 indicates perfectly opposing trading dynamics. Yet it should be noted that while the EEM closed at its highest since July as it rallied 0.45% last week, its rise paled in comparison to the S&P 500 (+1.65%).

On average, the MYR, SGD, PHP and IDR remain little changed from the prior week. This could continue being the case into 2020 as liquidity eases amid year-end holidays before volatility resurfaces come January. There is more room for the markets to continue pricing out 2020 Fed rate cut bets, the central bank has alluded to maintaining benchmark borrowing conditions unchanged in the year ahead.

ASEAN-Based USD Index Created Using TradingView

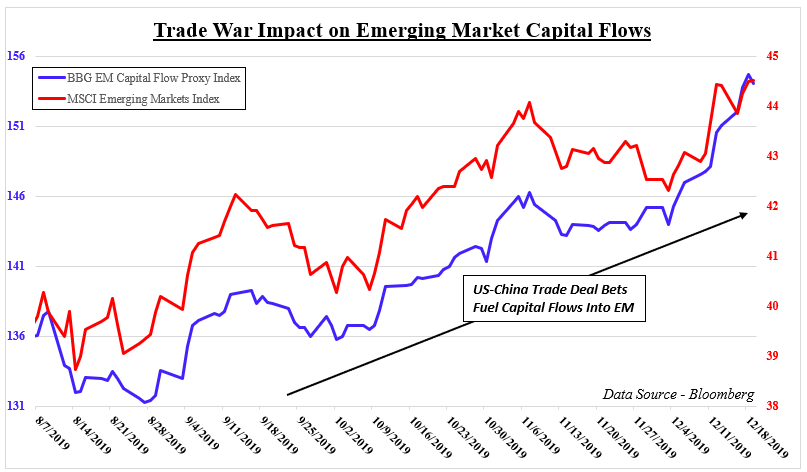

Emerging Markets Vs Capital Flows

Yet, to overlook the impact of the US-China trade deal for capital flows into emerging markets is a mistake. Looking at the next chart below, the EEM has been rising since August alongside an uptick in regional capital flows. The latter is at its highest since April 2018 and may continue supporting exotic currencies that tend to be sensitive to sudden shifts in foreign investment streams.

Event Risk – Singapore CPI and Industrial Production, China PMI, ASEAN PMI

As the new week begins, November Singaporean CPI data will cross the wires with headline inflation anticipated to rise 0.6 percent y/y. Then on Thursday local industrial production will be due. USD/SGD may see some near-term volatility on these data prints, but follow-through will likely be determined by how sentiment behaves in the coming weeks.

A key event risk to watch towards the final moments of 2019 is Chinese manufacturing PMI data on December 31. There may be an uptick to be had in this survey amid progress in trade talks. If that fuels confidence in the global growth outlook, we may see the US Dollar aim cautiously lower against the SGD, PHP, IDR and MYR.

Then in the new year on January 2, the markets will be watching how manufacturing PMI surveys unfold from Malaysia, Indonesia and the Philippines. At an unspecified time between January 2-3, inflation data out of the latter will cross the wires. Singapore will also release its annual GDP print for 2019.

Check out my Singapore Dollar currency profile to learn about how the MAS conducts monetary policy!

US Event Risk – Durable Goods, ISM Manufacturing

The improving outlook for the Fed puts the focus for the US Dollar on local event risk such as durable goods orders this Monday. Then on January 3, ISM manufacturing will cross the wires for the December period. More rosy outcomes will likely continue ebbing dovish bets for the United States, and that may counteract gains ASEAN currencies see on improving sentiment.

--- Written by Daniel Dubrovsky, Currency Analyst for DailyFX.com

To contact Daniel, use the comments section below or @ddubrovskyFX on Twitter