Trading Experience Talking Points:

- In a poll I conducted in August, 80 percent of those that responded said they had under 10 years experience

- The last significant, global bear market ended in early 2009, over a decade ago

- Willingness to suspend fear in flimsy growth may be just one side effect of an inexperienced market

What kind of trader are you? Take our DNA FX quiz to gather insights on how to improve your analysis technique.

The global capital markets will eventually take a serious tumble. This will be the kind of dive that handily surpasses the technical definition of a ‘bear market’ which is qualified as a drop of over 20 percent from highs. What’s more, given the circumstances of speculative build up in the late, halcyon years of the record-breaking climb through the 2010s – including a prevalence of central bank stimulus and wide deviation from traditional value metrics – the eventual capsizing will likely turn into a disorderly affair to some extent. Matching the problem in intensity, the backdrop that has supported our current position will likely translate into a broad collapse, spreading across asset classes and regions. It is those collaborative elements that will prove the self-reinforcing cycle of a speculative route.

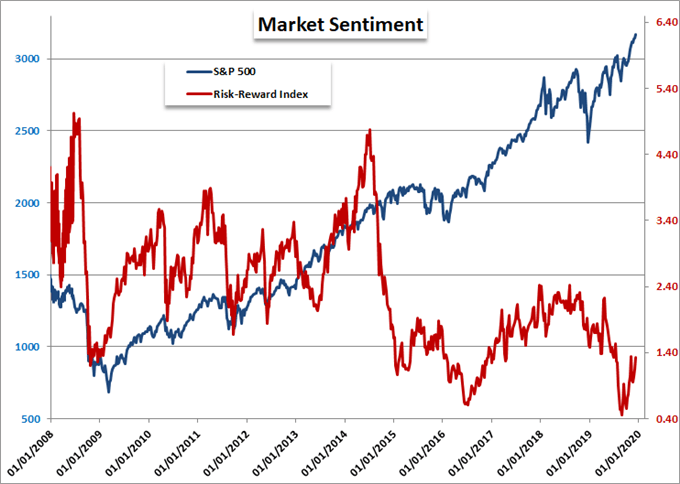

Chart of S&P 500 and a Risk-Reward Index of G10 10yr Yields Over FX VIX (Weekly)

Manufacturing Growth In the Wrong Places

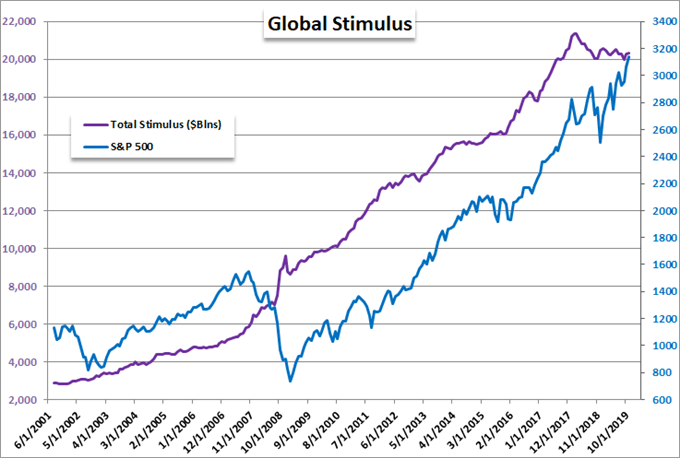

Why is this troubled prophecy inevitable? Because markets and economies naturally fluctuate through cycles of expansion and contraction. These regular currents don’t have to destructive, but certain environmental factors can inadvertently raise the risk. In the past decade, we have seen a successful bid by the world’s largest monetary policy authorities to pull the globe out of an endemic. Pushing benchmark lending rates towards zero (in some cases negative) and deploying massive stimulus programs staved off what many feared was a genuine risk of utter financial collapse. Yet, as the risk faded, the temporary provisions wouldn’t ebb in turn. With a implicit aim to accelerate growth or restore a target inflation rates, most of the largest central banks seemed to always falls short of the goal; but they did spur enthusiasm in one very obvious area: the markets.

Chart of the S&P 500 and Aggregate of Largest Banks’ Balance Sheets in $Blns (Monthly)

Some would chalk this relationship up to ancillary or happenstance. I think that is fanciful thinking given the tepid underlying growth that we have experienced and the exceptionally low rates of return in assets (in part a byproduct of the same effort to support the economy). In turn, an argument could be made that this we will simply see the underlying market and economy grow to transition asset valuation from the central banks’ responsibility to reasonably balanced market exposure. Yet, that is exactly what we have not seen happen in the past decade as the efforts were redoubled multiple times. Furthermore, the central banks cannot continue at their present clip indefinitely, and they don’t have the necessary to fend off new troubles that arise in these supposedly stable conditions.

A New Generation of Traders That Haven’t Experienced a Panic

In assessing the market’s departure from traditional valuation metrics, the full blame cannot be placed on the central banks, nor governments that shifting to competition instead of cooperation, financial institutions lowering their guard, or corporations hording cash. Market participants – investors and traders like you and I – bear a fair share of the responsibility for the growing distortion. As a large source of collective sentiment, smaller market participants have normalized the drift away from financially or economically-defensible risk-taking to allow for a collective delusion of proportional return.

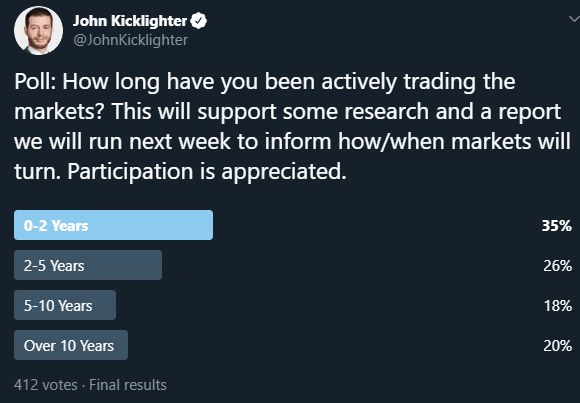

It is easy for bears to label this a self-dealing, convenient illusion; but I view it as more of a complacency. I use that term, ‘complacency’, a lot to describe the state of the markets. It is a relationship to risk that describes more an ignorance of risk borne of the simple fact that many in the market simply have not experienced an all-consuming deleveraging event. Consider, the last time we witnessed a systemic tumble was over 10 years ago. That said, I took to Twitter (referred to as FinTwit in the trader community) to see how much experience there was in this readily accessible group. As you can see, the majority (35%) of those that responded reported 0 to 2 years of trading experience. Far more troubling, only 20% of the 412 respondents. That means most of those that participated weren’t even in the markets during the last serious downcycle.

Now, one could argue that traders who are active in social media may not be indicative of the entire financial system. While their rank may not account for a majority of total traders or assets available for investment, there is inordinate influence through this group. Just as financial media headlines can spur speculative movement one way or another, the same happens in popular open social spaces. This can speak to the unflattering – and often inaccurate – deviation between ‘smart money’ and ‘dumb money’. These are just terms to differentiate professional financial managers from the self-directed, but there have been multiple high-profile stories this past year reflecting on the skew in favor of extreme capital withdrawal from the professional grade while the markets continued to climb – presumably by the ‘rest of us’.

| Change in | Longs | Shorts | OI |

| Daily | 6% | -5% | 1% |

| Weekly | 7% | -10% | -2% |

What Tips Us Over the Edge?

Next to the time spent in trying to develop an ‘edge’ in trading, the majority of a trader’s effort in the market is often spent on determining what the ultimate catalyst for a significant volatility event will be. There are a myriad of all-consuming risks that could rear their ugly head in 2020, with a resurgence of trade wars, recognition of a stalled global economy and the collapse in confidence around monetary policy being the most familiar candidates. It is hard to tell which of these will preemptively prove the spark to a global fire, and we should instead simply remain vigilant. However, the truly important thing not to forget is the consequences that come with an exceptional build up in risk. Eventually, reality will override complacency.

.