What Effect will Brexit have on Pound, FTSE, and other London Stocks?

- The Brexit talks between the EU and the UK could result in several different solutions or no deal at all

- UK Prime Minister Theresa May’s cabinet is due to meet next week before the two-day EU summit

- Here’s how the British Pound, the FTSE 100 index and Gilts might respond

Brexit Scenarios

The Brexit negotiations between the EU and the UK could lead to several possible outcomes, ranging from the UK remaining in the bloc to no deal at all, resulting in the UK crashing out of the EU on Friday March 29, 2019.

Traders in GBP (British Pound), the FTSE 100 index of London stocks, UK government bonds (Gilts) and other assets therefore need to be aware of the various alternatives and decide which assets to buy and which to sell.

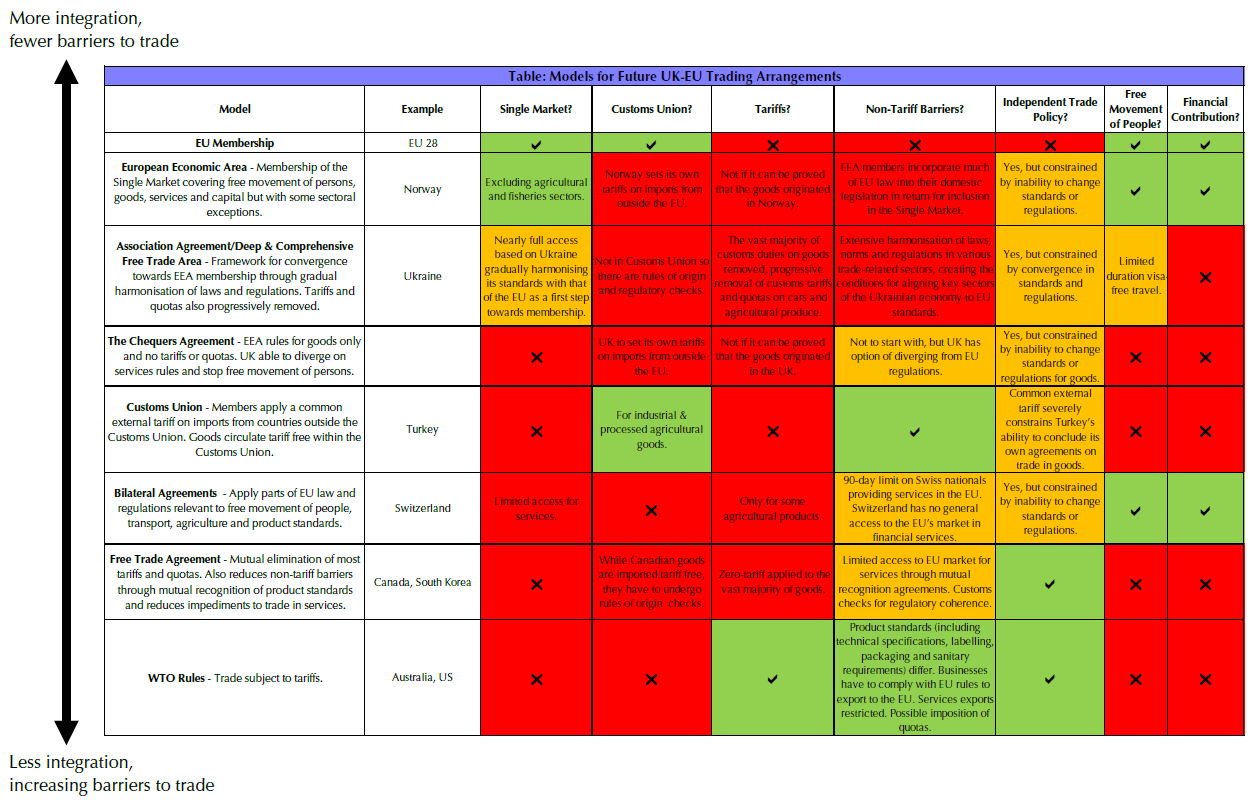

At Capital Economics, a London-based consultancy, analysts have produced the following detailed table listing the known possibilities:

Source: Capital Economics. You can click on the table for a larger image.

Market moves so far have shown that GBP tends to strengthen when the possibility of a “soft” Brexit increases and weaken when a “hard” or “cliff-edge” becomes more likely. The FTSE 100 index of the major London-listed stocks has tended to move inversely to the Pound, rising when GBP falls and vice versa, although there is no guarantee this will last.

Therefore, if the softer alternatives at the top of the table become more plausible, GBP would likely strengthen and London shares weaken. In the case of the harder alternatives at the bottom of the table – particularly the WTO-rules no-deal outcome – GBP would likely decline and London shares advance.

Here, therefore, are the Brexit possibilities that traders need to watch out for:

- The UK remains in the EU, perhaps after a proposed deal is rejected by the Westminster Parliament, a second referendum or “people’s vote” is held and the British electorate reverses its previous decision to leave. A capitulation by the EU, allowing the UK to leave but keep most of the benefits of membership, is possible but highly unlikely.

View our Economic Calendar to stay up to speed with important Brexit dates.

Depending on market sentiment at the time, a decision to remain in the EU or leave on highly attractive terms could potentially lift GBPUSD back to levels around 1.4300, where it traded before the result of the June 23, 2016 referendum was announced.

GBPUSD Price Chart, Weekly Timeframe (November 2015 – October 2018)

- The worst outcome for GBP would be no deal, in which case the UK would crash out of the EU and revert to World Trade Organization rules. This could happen if the British Parliament rejected a proposed deal and there was no second referendum, if a second referendum was held but the decision was again to leave or if the two sides simply fail to agree on terms.

View our GBP page here.

Potentially, UK Prime Minister Theresa May could be replaced as leader of the ruling Conservative Party, and therefore as PM, and/or there could be a snap UK Election won by the opposition Labour Party. A new Conservative Prime Minister would either give the party a boost or prove unpopular with the electorate, putting the Labour party leader Jeremy Corbyn in pole position to win.

Conservative rivals to May, including former Foreign Secretary Boris Johnson, are already jockeying for position in any leadership battle.

By and large, the markets prefer the Conservatives to Labour, and Corbyn is on the left-wing of his party, which is likely to make him particularly unattractive to the markets, where GBPUSD has dropped back after recovering strongly from its fall in the immediate wake of the Brexit referendum.

Note too that one of the major sticking points throughout the talks has been the border between Northern Ireland, which is part of the UK, and the Irish Republic. May has no overall majority in the UK Parliament and relies on Northern Ireland’s Democratic Unionist Party to pass legislation. The DUP has said it will vote against the Government if any of the ties between Northern Ireland and the UK are loosened, potentially bringing down the Government.

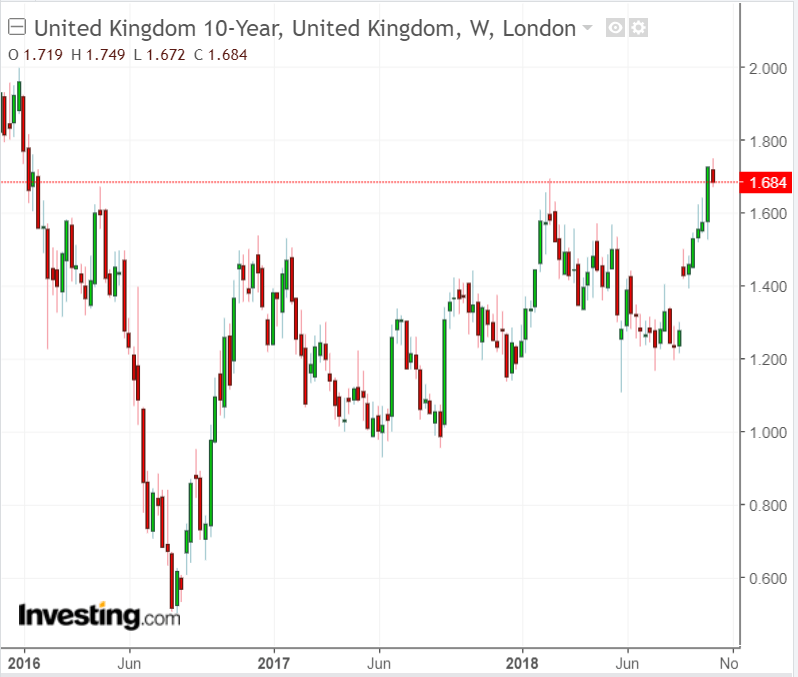

In these cases, the Bank of England might well lower UK interest rates if it foresees a potential economic meltdown, GBPUSD could drop back to its post-referendum lows around 1.1800 and UK Gilt yields might fall in line with Bank Rate as investors switched to the relative safety of bonds.

It is also possible, though, that investors might demand a higher risk premium for holding Gilts so a rise in yields cannot be ruled out, particularly if the central bank decides against a rate cut.

UK 10-Year Gilt Yield Chart, Weekly Timeframe (November 2015 – October 2018)

Source: Investing.com

Moreover, the inverse correlation between GBP and the FTSE 100 index might end, with London stock prices falling too. Here, a reasonable target might be the pre-referendum levels around 6,000.

FTSE 100 Price Chart, Weekly Timeframe (November 2015 – October 2018)

Between the two extremes of no-deal or the UK remaining in the EU, there are a number of possibilities, of which the ones most talked about are known as Norway, Chequers and Canada-plus.

- The neutral outcome could be the Chequers plan, named after the country retreat of UK Prime Ministers where May brought together members of her Cabinet in an attempt to reconcile the differences between the Eurosceptics against the EU and the Remainers in favor.

By and large, the meeting failed to narrow the gap between the ministers and was followed by the resignation from the Cabinet of the controversial Boris Johnson. Moreover, there has been little support for it in Brussels, where it has been rejected.

This makes it a rather unlikely outcome, although any agreement loosely based on it would likely lead to a relief rally in GBP, albeit not the surge that would follow a UK decision to stay in the EU.

- The Norway option is the closest to remaining in the EU. Like Norway, the UK would be in the so-called European Economic Area (EAA) and would remain in the single market without any internal borders or other regulatory obstacles to the free movement of goods and services, although agriculture and fisheries would likely be excluded.

Norway, Iceland and Liechtenstein are the only EEA members not in the EU and joining them would likely infuriate the Eurosceptics as there would be freedom of movement for people within the area and a continuing UK financial contribution to Brussels. Like the Chequers option, it would be positive for GBP but, also like Chequers, it would be unlikely to gain enough support as many British people voted for Brexit precisely because they wanted to reduce immigration to the UK and end the UK’s contribution to the EU budget.

However, the Labour Party – which like the Conservatives is split on Brexit – appears to be moving towards this option so an election victory by Labour might bring Norway back into focus and offset the otherwise negative market reaction to a Labour government. It would also be welcomed by the EU, which is in favor of a “bold” free-trade deal without tariffs or quotas.

- The Canada option is the closest to no deal so would almost certainly be negative for GBP. There would simply be a free-trade agreement between the UK and the EU, although those who argue for it have used the term ‘Canada+++’, suggesting a rather closer relationship than the current one between Canada and the EU.

This is the solution supported by pro-Brexit Conservatives like Johnson and would leave the UK free to strike bilateral deals with countries like the United States, India and perhaps even China and other growing Asian economies. However, a free-trade deal between the UK and the EU would not necessarily solve the Irish border question as the UK might well be outside the EU customs union.

Summary of the Effect of Brexit on Pound and London Stocks

- No deal or Canada option: GBPUSD could reach 1.1800

- UK remains in EU or Norway option: GBPUSD could reach 1.4300

- Chequers or similar option: GBPUSD little changed to modestly higher

More to read on Brexit and the financial markets:

Resources to help you trade the forex markets

Whether you are a new or an experienced trader, at DailyFX we have many resources to help you:

- Analytical and educational webinars hosted several times per day,

- Trading guides to help you improve your trading performance,

- A guide specifically for those who are new to forex,

- And you can learn how to trade like an expert by reading our guide to the Traits of Successful Traders.

--- Written by Martin Essex, Analyst and Editor

Feel free to contact me via the comments section below, via email at martin.essex@ig.com or on Twitter @MartinSEssex