Talking Points – HKMA, USD/HKD, HONG KONG DOLLAR

- A rising US Dollar has placed HKMA’s USD/HKD peg again under pressure

- Hong Kong’s aggregate balance is poised to decline to 2008-lows very soon

- In the event of a de-peg, this outcome risks stoking severe market volatility

Have a question about the consequences of this development to the markets? Join a free Q&A webinar and have it answered there!

Back in April 2018, fears of monetary tightening from the Hong Kong Monetary Authority amidst a weaker HKD initially triggered a temporary bout of marketwide panic. Chinese stocks declined and the sentiment-linked AustralianandNew Zealand Dollars fell. A couple of days later, the HKMA upheld efforts to maintain their currency peg. USD/HKD pulled back and shares in the Asia/Pacific region rejoiced.

Since then, a stronger US Dollar has been adding pressure to not just its Hong Kong counterpart, but to others as well. Broadly speaking, you can attribute this to persistent efforts from the Fed to raise interest rates amidst a strengthening economy. More recently (as of early August 2018), USD has been further lifted by aggressive risk aversion amidst fears of Turkish contagion.

Thanks to the gains in the greenback, attention has been refocused on the HKMA and their currency peg. This entity largely conducts monetary policy by maintaining the stability of the Hong Kong Dollar. Back in 2005, it established a range for USD/HKD to trade in as part of its “three refinements” to help stabilize its currency.

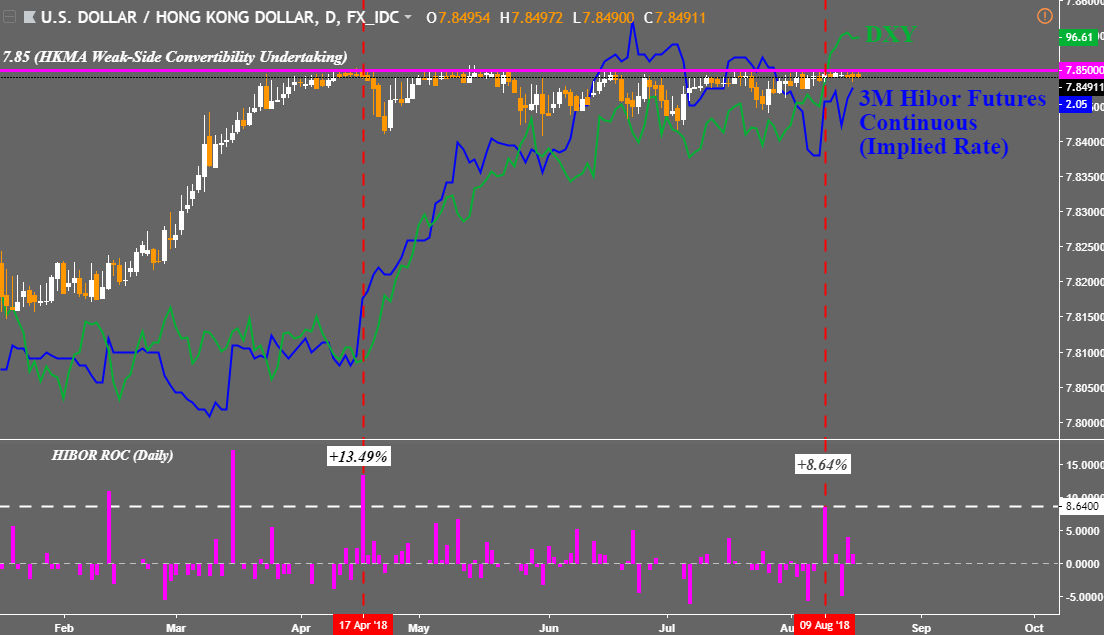

This included a “strong-side convertibility undertaking” (CU) at HK$7.75/USD and a “weak-side CU” from 7.80-7.85. Looking at the chart below, you can see that for most of this year thus far, USD/HKD has been precariously hovering under the outer limit (7.85). Simultaneously, we also had a spike in the three-month HIBOR lending rate which was its largest in a single day since April 2018.

Chart created in TradingView

HIBOR is the Hong Kong Interbank Offered Rate, which is essentially the benchmark interest rate for lending between banks within the autonomous territory. It is determined by the Hong Kong Association of Banks. It often moves in parallel with actions from the HKMA as it adjusts liquidity in the market to help stabilize its currency.

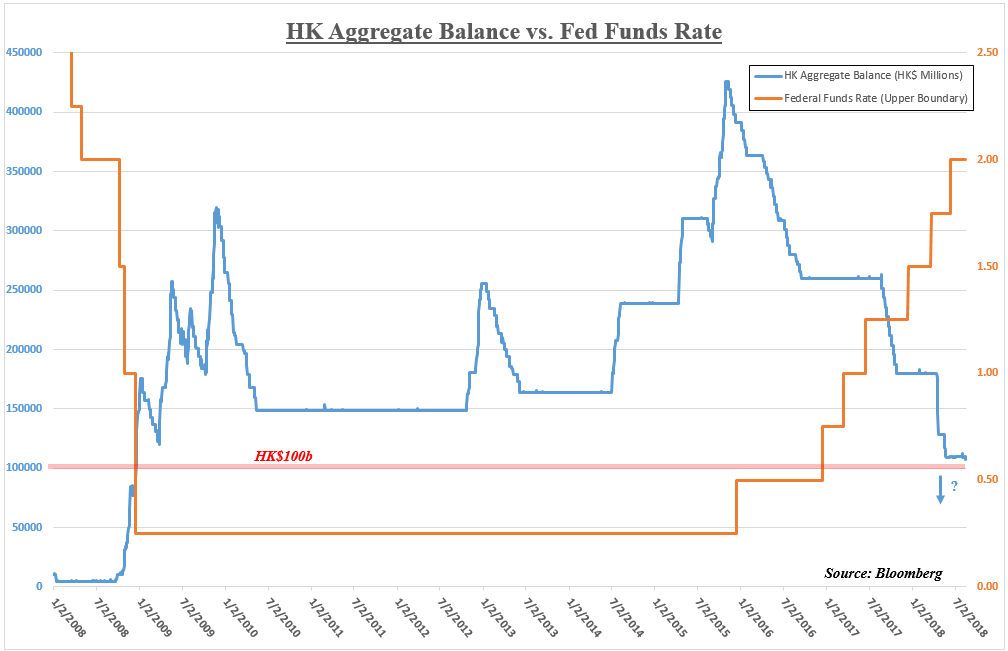

So what’s the deal with the recent spike in HIBOR then? Looking at the next chart below, you can see Hong Kong’s aggregate balance, which has been falling from over HK$400b back in 2015 to just a hair over HK$100b as of August 2018. This has also occurred simultaneously with rising interest rates in the US. The upper boundary of the federal funds rate stands at 2.00% as of this report. This is up from 0.25% in 2015.

Essentially, the aggregate balance is part of Hong Kong’s monetary base, which is made up of the sum of balances of banks’ clearing accounts. It varies depending on the flow of funds in and out of the HKD. Lately, the HKMA has been spending it in an effort to uphold their currency. Projections are calling for it to fall under HK$100b, which would be the first time since 2008.

In some ways, this has increased fears that the monetary authority won’t be able to keep USD/HKD under 7.85. But on August 16th 2018, the HKMA once again reiterated efforts to maintain the peg, which improved market mood to a certain extent (similar to what we saw back in April). But signs that the monetary authority will continue facing pressure to stabilize its currency could perhaps reignite aggressive risk aversion.

At the moment, the Fed is still projected to continue raising rates by an additional two times in 2018. This would bring total increases to four this year. However, that fourth rate hike by the beginning of 2019 is not fully priced in quite yet. In addition, trade wars and Turkish fears were recently reignited. Both of these outcomes can have the potential to keep the US Dollar appreciating in the near-term. This begs the question, what will the HKMA do?

BACKGROUND: A Brief History of Trade Wars, 1900-Present

FX Trading Resources

- Just getting started? See our beginners’ guide for FX traders

- Having trouble with your strategy? Here’s the #1 mistake that traders make

- See our free guide to learn what are the long-term forces driving US Dollar prices

- See how the US Dollar is viewed by the trading community at the DailyFX Sentiment Page

--- Written by Daniel Dubrovsky, Junior Currency Analyst for DailyFX.com

To contact Daniel, use the comments section below or @ddubrovskyFX on Twitter