Having trouble trading the Euro? This may be why.

World stock markets ended the second quarter on a sobering note and are set to begin the third quarter with reasons for investors to be concerned. Given the interconnectedness of the world’s economies, a number of factors could reflexively spark significant investor angst and continued selling in the third quarter.

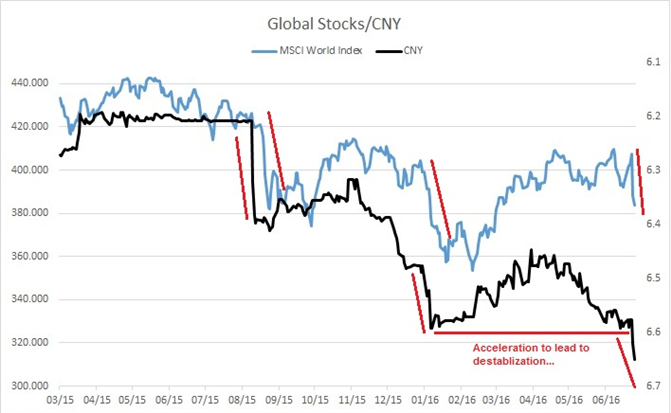

Weakening Chinese yuan

A development which is at the forefront of our minds as we enter the third quarter of 2016 – the depreciation of the Chinese yuan versus the US dollar. On two occasions in the past year a rapid depreciation of the yuan hit global markets as fears spread over just how weak the world’s second largest economy really is. The first major decline in August of last year was state-induced and caused a dramatic spike in risk aversion. The other instance of the yuan rapidly declining occurred prior to the sell-off in global stocks to start the year.

The CNY has been trending lower since April, but the risk of acceleration is rising as it trades to fresh multi-year lows following the ‘Brexit’ vote, and threatens the stability of global financial markets. Can the People’s Bank of China stem the decline of the yuan and capital outflows, or will they be at the mercy of market forces?

Graph Created by Paul Robinson, Market Analyst.Data Source: Bloomberg,

BoJ and ECB Losing Impact

Further easing measures established during the first-half of 2016 by the European Central Bank and Bank of Japan have yet to have any impact on boosting their economies, inflation, and stock markets. While it takes time for fresh stimulus to feed through the economy and financial markets, there has been no forward-looking upward repricing in their respective stock markets. Just the opposite. And why not? So far, prior efforts have not yielded long-lasting results.

The Nikkei 225 recently traded to its worst levels since the fourth quarter of 2014. The expectation on this end is the latest rounds of measures aren’t likely to gain traction in the coming quarter, if at all, which should result in the continuation of the trend lower dating back to the 2015 highs.

And since the ECB is turning Japanese, the same principles apply to European markets as well. While global indices are highly correlated across the board, the Eurostoxx 50 and Nikkei 225 have a whopping 94% correlation since the April 2015 highs.

Graph Created by Paul Robinson, Market Analyst.Data Source: Bloomberg,

The UK and ‘Brexit’

Fears regarding ‘Brexit’ were weighing on the UK economy long before the ‘leave’ vote became official on June 24. Economists’ forecasted impact of leaving the EU is in the ‘we really have no clue’ range, with estimates spanning from only a 2% negative impact on GDP to as much as 10% over the next few years. We won’t pretend we know what is in store in the longer-run, but it is reasonable to conclude that uncertainty, an enemy of markets, will keep investors on edge in the intermediate-term. This favors at the least, stagnant, and likely lower prices for UK stocks for the foreseeable future.

A potential silver lining in the interim is a weaker British Pound, which should help bolster exports and multi-national corporate profits, but looks unlikely to be enough to stave off the negatives of other domestic and global developments.

The risk of a ‘leave’ contagion could become a reality as other EU members become inspired to act on what they believe to be in their own country’s best interest. Looking out over the next quarter this may not be a theme which gains substantial traction, but could certainly be a damper on investor sentiment as this becomes viewed as a viable threat to the cohesiveness of the Eurozone.

US Rate Hike off the Table, Labor Market Conditions Weakening

Following the ‘Brexit’ vote, expectations for a rate increase by the Fed at any of the upcoming meetings through November dropped to 0 via Fed Fund futures, even going so far as to price in a rate cut out to February 2017. Even though odds of a reduction in rates are low, and this pricing mechanism is quite volatile, it demonstrates how skeptical the market is of the Fed’s intentions to increase rates in the foreseeable future. With that said, probability of a rate hike diminishing to zero is not viewed as a positive given the reasoning which keeps the Fed sidelined, which could very well be the same catalysts that takes a big bite out of world markets – domestic and global economy weakening, falling CNY/China, uncertainty spurred by ‘Brexit’, and skepticism over the effectiveness of stimulus in Japan and Europe.

The Fed has a dual mandate – maximum employment and price stability – of which the former was at the heart of the Fed’s case for “lift-off’ back in December. However, conditions in the labor market have since turned, potentially painting a sobering picture for the American economy.

The Labor Market Conditions Index (LMCI) is a Federal Reserve born index which measures changes in the labor market. It peaked back in December and has been falling since. As far back as data goes (1977) the LMCI turned lower prior the beginning of 4 of the past five recessions. The one time it didn’t provide much warning, only three months, was before to the double-dip recession in the early 1980s. There was a false signal during both the mid-1980s and 90s; and the current downturn could certainly be another head-fake, but given the US economy is now entering its seventh year of expansion – one of the longest on record – we should heed its caution.

The lag-time from when the LMCI turned lower to the onset of a recession was 3 to 17 months, of which we are now moving well into that range. We will continue to monitor this development as we progress into the third quarter along with other factors which may point to a growth scare or worse. This isn’t a call for an imminent recession, but risk is rising, and should the US economy be headed towards a recessionary environment the stock market is almost certain to price it in with double-digit negative returns prior to its arrival.

Graph Created by Paul Robinson, Market Analyst.Data Source: Bloomberg

Technical Outlook

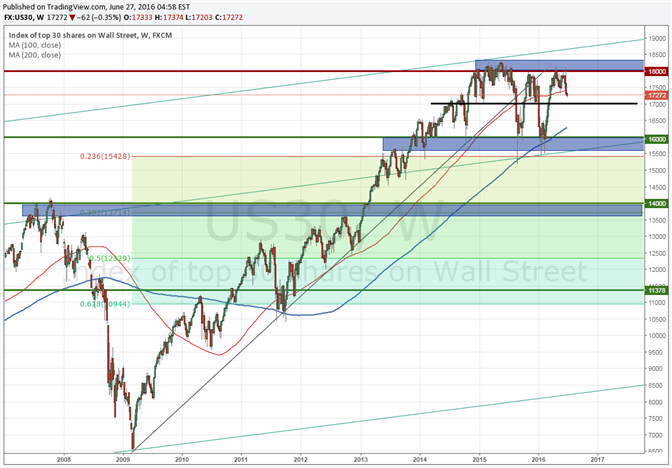

US30 Weekly

The Dow Jones Industrial average is showing signs of weakening after failing to set new highs this past quarter.The index has been trading sideways between well-defined technical levels since the Dow established all-time highs above the 18,000 handle before breaking below the QE induced up trend-line.

At this stage, the technical outlook appears clear. Further weakness could put the spotlight again on a support zone below the 16,000 figure. The index has rejected lower prices up until this point and the “line in the sand” looks to be around the 15,500 figure, which coincides with the 0.236 Fib of the post GFC recovery. A failure to hold prices higher seems likely to put the spotlight on the 2008 top around the 14,000 figure, but Q3 support seems likely around the 16,000 handle.

For any real upside conviction, the Dow will need to set, and hold, new all-time highs.

US30 Weekly Chart - Created by Oded Shimoni, Junior Aanlyst with Trading View Charts on DailyFX.com

SPX500 Weekly

Unlike the Dow Jones, The S&P 500 rally from 2009 has yet to see a break below the uptrend-line support. The index bounced from range lows around the 1800 handle and the trend line support after the January scare, but has since failed to break above resistance at around 2100-2137. Indeed, as the Dow, the S&P seems to be “stuck” in a well-defined technical range that might suggest that a fundamental catalyst might be required to see a clear shift in trend or upside continuation.

Further weakness seems likely to put the focus again on the support zone around 1835-1800. A break below this zone combined with the trend line and the 200 day SMA, will break the current “structure” of the market and might see aggressive selling that could put the focus on the 1600 handle. With that said, Q3 support seems likely to be around the 1835-1800 area.

For any real upside conviction, the S&P will need to set, and hold, new all-time highs.

SPX500 Weekly Chart - Created by Oded Shimoni, Junior Aanlyst with Trading View Charts on DailyFX.com

GER30 Weekly

After topping in April 2015, the DAX has been trading in the confines of a down trending channel within the longer term uptrend from 2009. The index found support around the 9000 handle in Q2, which coincides with the 0.382 Fib of the post GFC recovery, and retraced higher only to fail at establishing new highs before falling sharply following the “Brexit” decision.

Further downside might initially put the focus on the 9000 handle again, but the failure to move above 10400 could suggest that the price may move lower before buyers come into the market again with any conviction. This seems to make the 8500 level the likely support for Q3, while a break lower could see the 2008 highs (and the 0.50 Fib) around 8000 retested for possible support

For any real upside directional bias, the DAX will need to break, and hold above the 10400 resistance.

US30 Weekly Chart - Created by Oded Shimoni, Junior Aanlyst with Trading View Charts on DailyFX.com

UK100 Monthly

We take a slightly longer term view for the FTSE since it represents a clearer view. A failed breakout to a record high in April 2015 led to significant losses for the index that eventually saw a bounce higher from around the 5500-5700 area which coincided with the 0.383 Fib of the post GFC rally. Previous V shaped tops late 1999 and 2007 saw sharp declines to around the 3500 level followed by V shaped bottoms recoveries. In both other topping events, the index saw clear price rejections around 5500-5700, as in the current price action (see arrows). In the past events, once this zone broke down, a rapid downward spiral has transpired. Estimated support forQ3 is 5600, while a break lower seems likely to see further movements to 4800-5000.Resistance might be found around 6400-6500 followed by the 6750-6800 area if the index manages to find some positive momentum.

US30 Weekly Chart - Created by Oded Shimoni, Junior Aanlyst with Trading View Charts on DailyFX.com

Nikkei 225 Weekly

The Nikkei 225 is approaching what appears to be a crucial area of support. The index saw a sharp move lower, and moved below its 200 day moving average, following the “Brexit” decision, but has since held the 15,000 handle support. The 14,347-14,000 zone has been a criticalarea of support on a number of occasions since 1992 and coincides with two trend line resistance levels turned support from 1997 and 2010, as well as the 0.50 Fib from the 2009 lows. This confluence zone might provide ample support in Q3, while a move lower opens the door to the 13,000 and 12,000 handles. Resistance might be found around the 17660 to 18000 area, which will need to be cleared for bulls to really be back in control.

US30 Weekly Chart - Created by Oded Shimoni, Junior Aanlyst with Trading View Charts on DailyFX.com

Disclaimer

DailyFX Market Opinions

Any opinions, news, research, analyses, prices, or other information contained in this report is provided as general market commentary, and does not constitute investment advice. DailyFX will not accept liability for any loss or damage, including without limitation to, any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

Accuracy of Information

The content in this report is subject to change at any time without notice, and is provided for the sole purpose of assisting traders to make independent investment decisions. DailyFX has taken reasonable measures to ensure the accuracy of the information in the report, however, does not guarantee its accuracy, and will not accept liability for any loss or damage which may arise directly or indirectly from the content or your inability to access the website, for any delay in or failure of the transmission or the receipt of any instruction or notifications sent through this website.

Distribution

This report is not intended for distribution, or use by, any person in any country where such distribution or use would be contrary to local law or regulation. None of the services or investments referred to in this report are available to persons residing in any country where the provision of such services or investments would be contrary to local law or regulation. It is the responsibility of visitors to this website to ascertain the terms of and comply with any local law or regulation to which they are subject.

High Risk Investment

Trading foreign exchange on margin carries a high level of risk, and may not be suitable for all investors. The high degree of leverage can work against you as well as for you. Before deciding to trade foreign exchange you should carefully consider your investment objectives, level of experience, and risk appetite. The possibility exists that you could sustain losses in excess of your initial investment. You should be aware of all the risks associated with foreign exchange trading, and seek advice from an independent financial advisor if you have any doubts.