Talking points:

- Global markets are continuing to show risk aversion after voters in the U.K. elected to leave the European Union.

- My colleague, Tyler Yell, discussed Building a Post-Brexit Trading Plan previously, with heavy emphasis on the US Dollar. In this article, we extend that a step further by looking at the prospect of continued risk aversion in Gold and the Japanese Yen.

- If you’re looking for trading ideas, check out our Trading Guides. And if you want something more short-term in nature, check out our SSI indicator. If you’re looking for an even shorter-term indicator, check out our recently-unveiled GSI indicator.

The past two trading days have brought a stark about-face to global equity markets. While much of the free world went into the recent Brexit referendum with the expectation for a ‘remain’ vote winning out, shock and dismay enveloped capital markets in the days after as a vote to leave raised numerous questions about the path of the global economy.

But this pain hasn’t been relegated to the United Kingdom, or even Europe for that matter. We’ve seen signs of risk aversion picking up around-the-world in the wake of the Brexit referendum, and this is highlighting the impact of yet another risk factor that the global economy has to contend with as the world attempts to balance a threatening flurry of risks.

In this article, we’re going to look at three markets that may shine if risk aversion continues to show on the back of the recent Brexit referendum.

Gold

This is a rather obvious option given recent price action. Gold has caught a major bid through much of 2016 as the Federal Reserve has continued to display a dovish tone whilst backing down from the four full rate hikes that the bank was looking at coming into 2016. As we came into the new year, the concurrent risk factors of a meltdown in commodities (namely, Oil) and a slowdown in Asia were being met with the expectation of the Fed to hike rates a full four times in 2016. This flurry of risks was too much for global markets to bear, and in short order we had threatening moves of risk aversion hitting nearly every market on earth.

The one factor that could give there, the Fed backing down, happened in phases. On February 11th, Chair Yellen told Congress that the Fed wasn’t taking the option of negative rates off-the-table, and this was largely inferred as a dovish take from the head of the Fed. And later in March, the Fed moved that expectation down to two hikes in 2016 from the previous four, and this was yet another dovish shot-in-the-arm to global risk trends. And as this was happening, markets began pricing in the expectation for the Fed to do what they’ve been doing all along: responding to global pressure with dovish support for capital markets.

This provided a major bid for Gold as the Fed continued to back down, all the way into May of this year.

Created with Marketscope/Trading Station II; prepared by James Stanley

Throughout the month of May, various members of the Fed talked up the prospect of 2-3 rate hikes in the remainder of the year which, deductively meant that June was likely on the table for a potential rate hike. This created a reversal in the USD-downtrend while softening Gold prices throughout the month. But as we came into June, it became painfully obvious that the U.S. economy wasn’t likely going to be seeing a rate hike anytime soon. After the abysmal Non-Farm Payrolls number in the early portion of the month, the US Dollar drove lower and created an outsized reversal Gold prices.

That reversal has continued throughout the month, spiking higher with extreme strength on the back of the recent Brexit referendum. As uncertainty has hit global markets, investors have rushed to safety in both USD and Gold. This highlights pure risk aversion as investors are loading into the US Dollar despite the fact that rate expectations out of the U.S. continue to dwindle lower on this palette of increased risks.

But this isn’t the only market seeing extreme strength, and as we saw in May, Gold prices could be extremely susceptible to Fed action or even random comments. For traders looking to avoid the constant rollercoaster that have become Federal Reserve rate hike expectations, there is another potentially more attractive market for to draw one’s attention towards.

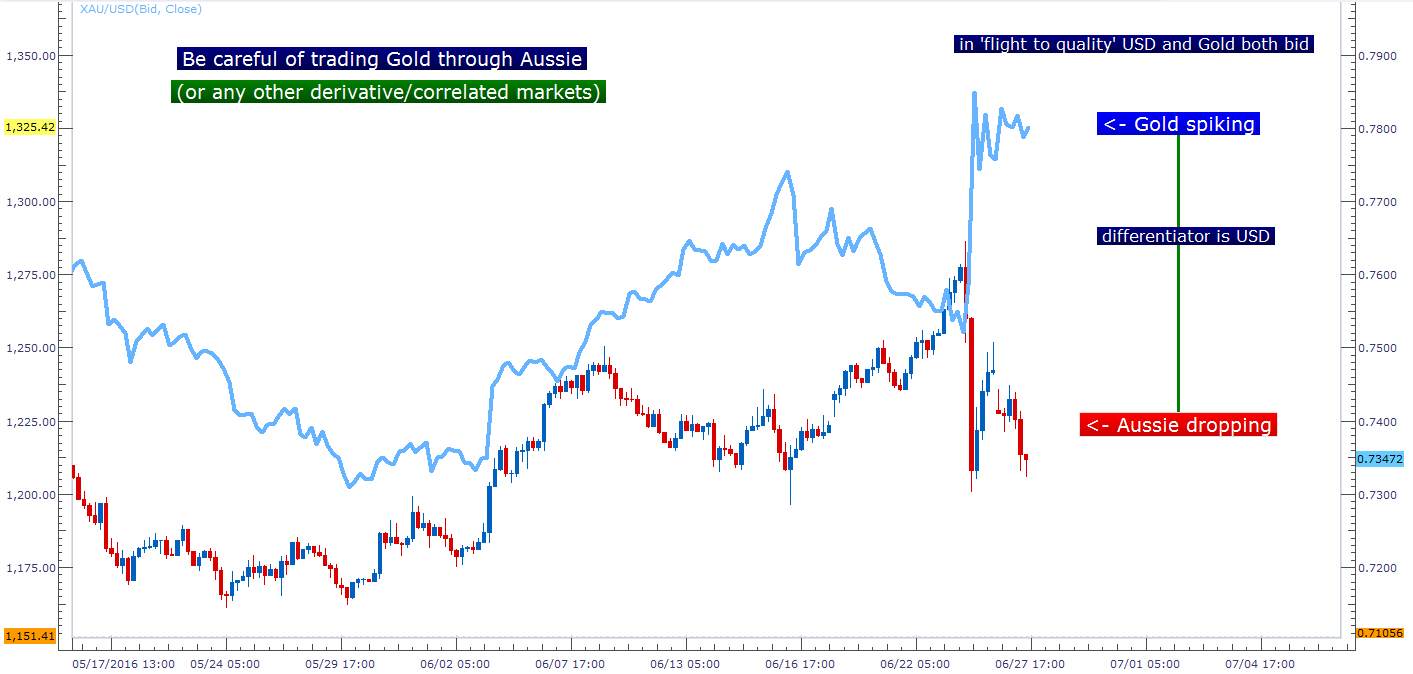

Important Note on Correlations: Before we move on to that other market, there is an important point of note here regarding correlations. Many traders have become accustomed to the correlation between Gold prices and the Australian Dollar. As Australia has significant deposits of natural resources, particularly metals, we can often see similar themes playing out in metals and the Australian Dollar. This is somewhat of the predominant theme from 2008-2011, as QE-driven asset price gains saw the rise in both commodity prices and the Aussie. This only played directly into that implied correlation as a weakening US Dollar lifted all boats.

But more recently, that correlation has become divorced. The Aussie is seeing considerable weakness as the US Dollar gets stronger, and Gold is continuing to pop-higher on enhanced safe-haven flows. On the chart below, we look at the recent divergence in Gold and the Aussie. The differentiator here and the reason that both Gold and Aussie aren’t moving in the same direction is the US Dollar. Gold is stronger than USD, which is stronger than Aussie, and this has classic signs of a ‘flight to quality.’

Created with Marketscope/Trading Station II; prepared by James Stanley

The Yen

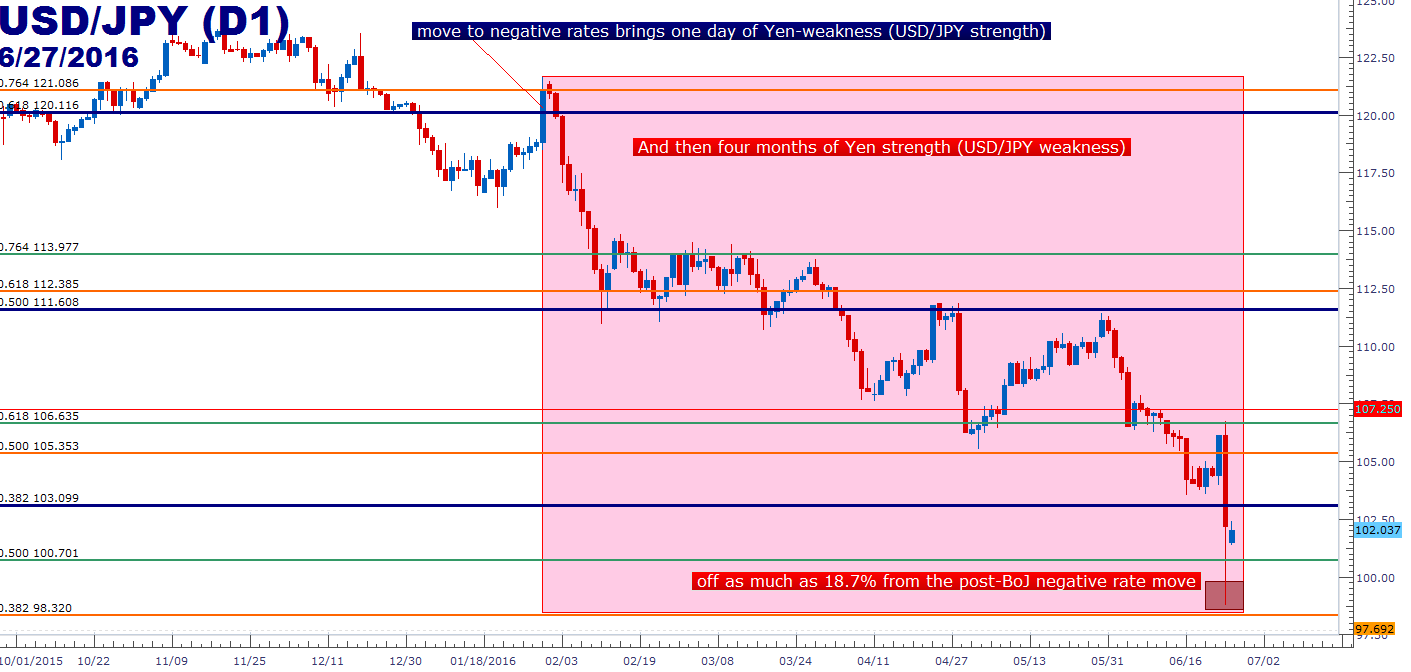

A currency that could be far more attractive than the Australian Dollar in the event of continued risk aversion is the Japanese Yen. We’ve been discussing the preference of the Yen as the ‘safe haven vehicle of choice’ for the better part of the past nine months, and as signs of ‘risk-off’ have continued to flag, Yen strength has remained a pervasive theme. Thickening matters is the fact that each attempt that the Bank of Japan has made to quell this persistent Yen strength has failed, including the most recent movement to negative rates. Such a move was thought to spur capital flows out of the country, thereby bringing in Yen weakness. But that hasn’t happened: Instead we saw the Yen continue its run of strength by as much as 18.7% since that move.

Yen Strength as a Pervasive Theme

Created with Marketscope/Trading Station II; prepared by James Stanley

The Yen, Nikkei and Japanese economy are all very much aligned with global risk themes. As the Japanese economy attempted to turn the tides of 20+ years of deflationary pressure, Abe-nomics became the preeminent economic catalyst for the Japanese economy in 2012, led by Prime Minister Shinzo Abe. At the core of the plan was the prospect of weakening the Yen to remove pressure from exporters, thereby bringing initial signs of growth into the Japanese economy as employers could direct newfound profits (on the back of a weaker Yen) to hiring, which should lead to inflation as competition for workers increases.

This helped to drive the stock market higher, but inflation never showed. So the Bank of Japan continued with intervention until, eventually, they had to start buying stocks after they had cornered their own government bond market. This led to the surprise Halloween decision in 2014 in which the Japanese Government Pension and Investment Fund was to begin buying stocks with QE. That soundly blew up less than a year later.

So, the question persists: What in the world is the Bank of Japan going to do? This is what led to that surprise move to negative rates in January, and as we already saw how markets responded to that.

The one big threat on the long side of the Yen is the prospect of spot market intervention in the event of persistent Yen strength. Finance Minister, Taro Aso has already said that ‘one-sided’ moves in the Yen will not be tolerated, but the big question is one of ability as Japan’s already received condemnation for ‘beggar thy neighbor’ currency weakness strategies. If Japan intervenes in the spot market, well that means other currencies get stronger just through relative pricing. And which Central Banks around the world are actually welcoming exogenous, artificially-driven strength? Probably not very many, and this makes the prospect of prolonged intervention from the BoJ less likely in current conditions.

But this threat of spot market intervention is one that traders need to be cautious around. This means to be really careful as the Yen moves to new highs (or USD/JPY to new lows), as you may get a really big player on the other side of the market. However, traders can look to utilize trend-following strategies by looking to sell at resistance in the effort of avoiding ending up diametrically opposed to the Bank of Japan.

On the chart below, we’re looking at a series of levels that traders may be able to use to look for that next ‘lower-high’ point of resistance in USD/JPY.

Created with Marketscope/Trading Station II; prepared by James Stanley

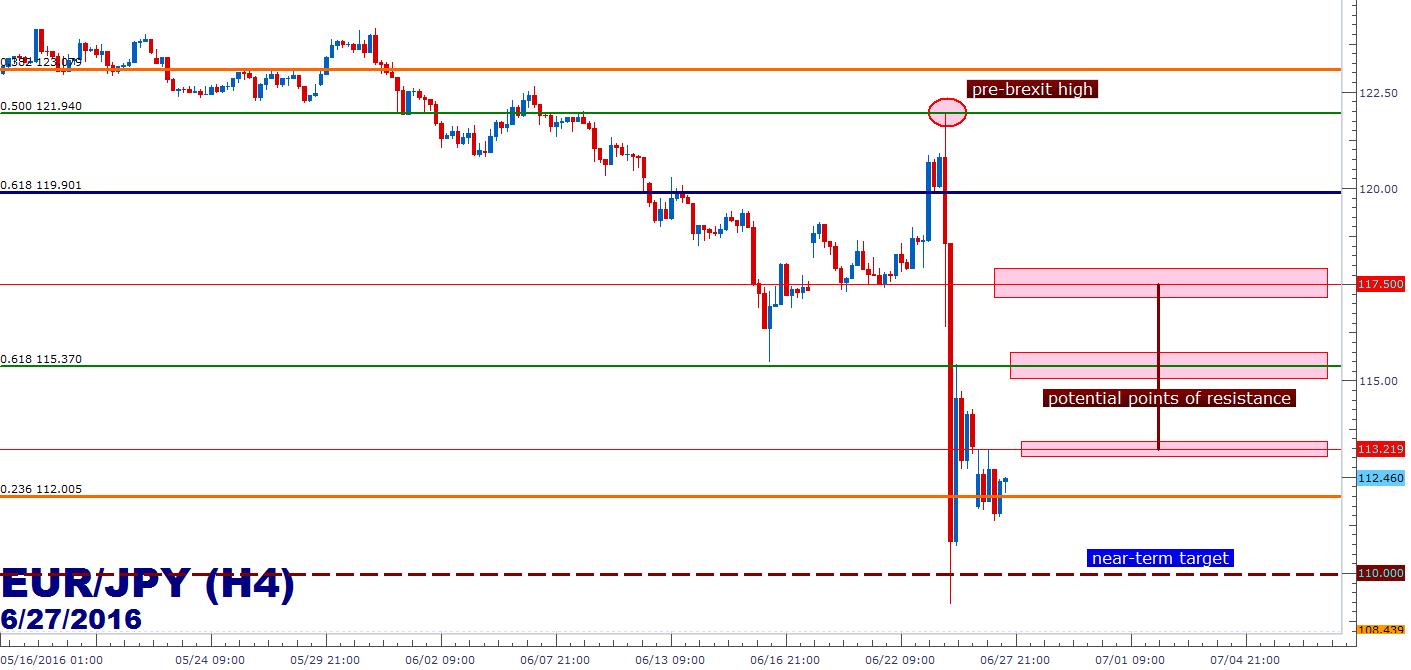

For those that are looking for perhaps even more volatility around the most recent set of events, traders can look at matching up the Yen against the Euro. Should risk-aversion continue to increase on the back of Brexit, the Euro will likely continue to be negatively impacted. And when matching up that potential Euro weakness along with persistent Yen strength, traders may be able to look at a market more amenable to continued risk aversion.

Created with Marketscope/Trading Station II; prepared by James Stanley

--- Written by James Stanley, Analyst for DailyFX.com

To receive James Stanley’s analysis directly via email, please SIGN UP HERE

Contact and follow James on Twitter: @JStanleyFX