THE CHINESE YUAN: WHAT TRADERS SHOULD KNOW ABOUT CHINA’S CURRENCY

- What is the difference between the RMB and the Yuan?

- What are onshore and offshore RMB?

- What is PBOC’s CNY Fixing?

- Is China’s exchange rate fixed or floating?

- Is the Yuan pegged to the USD?

- The role of China’s Central Bank, SAFE and CFETS

WHAT IS THE DIFFERENCE BETWEEN THE RMB AND THE YUAN?

The Chinese currency, widely called the Yuan, has multiple names with different purposes or functions.

The Yuan is simply the name of a basic unit of account in China, similar to the ‘Dollar’ in the United States. The Chinese currency used in mainland China is called the Chinese Yuan, or ‘CNY’. Just like the Dollar can be broken down into quarters and dimes, the Yuan can be broken down into smaller units as well, such as Jiao (.1 of 1 Yuan), Fen (.01 of 1 Yuan) and etc.

Reminbi is another common name of the Chinese currency. It can be loosely translated as “people’s currency”. RMB is the abbreviation of Reminbi.

WHAT IS THE DIFFERENCE BETWEEN ONSHORE AND OFFSHORE RMB?

China’s capital markets are not fully opened yet. This means the Yuan has different features in domestic and international markets.

Onshore Yuan

In the onshore market, which is within Mainland China, the Yuan is used mainly for two purposes:

- Interbank settlements.

- Corporates selling and purchasing foreign exchange for business purposes.

The Yuan exchange rate in the onshore market is given a ticker, CNY.

Offshore Yuan

Yuan’s offshore market is outside of Mainland China. This includes traditional centers, such as Hong Kong, Singapore and London, and newly-developed centers like Luxembourg. The Yuan in the offshore market is given a separate ticker, CNH, such as USD/CNH. In the offshore market, the Yuan trading is normally more active and market-driven than in the onshore.

Follow the DailyFX Economic Calendar for live events that can drive Yuan movements.

WHAT IS PBOC’S CNY FIXING?

For each Yuan pair, there is a third rate in addition to the onshore rate and the offshore rate. It is called the Yuan reference rate, also known as the mid-point rate, the central parity rate or the daily fixing. All these names refer to the benchmark rate set by China’s Central Bank.The Central Bank, with the full name as People’s Bank of China (PBOC), issues the reference rate on a daily basis.

In specific, the PBOC refers to three factors to determine the reference rate:

- The closing rate on the previous trading day, quoted by China’s interbank participants.

- Changes in demand and supply in the foreign exchange market.

- Moves in major currencies.

IS CHINA’S EXCHANGE RATE FIXED OR FLOATING?

China implements a managed-floating exchange rate regime, which is neither free-floating nor fully controlled. If we say a free-floating system is the white color and a fully-controlled system is black, the Yuan’s color is grayish-white. Currently, the Yuan exchange rate system is moving towards the direction of free-floating, under the reforms by the PBOC.

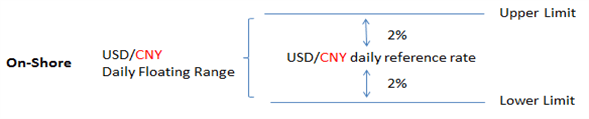

IS THE YUAN PEGGED TO THE USD?

In the onshore market, the Yuan rate is allowed to float within 2% above or below the reference rate. The trading band is determined by the PBOC as well. It is expected to stay unchanged for a long time once it is set, unlike the daily reference rate.

The band was first introduced and set to be 0.3% in 1994. It was raised to 0.5% in 2007 and then to 1% in 2012. The current 2% limit was set in 2014.

THE ROLE OF CHINA’S CENTRAL BANK IN YUAN EXCHANGE RATE REGIME

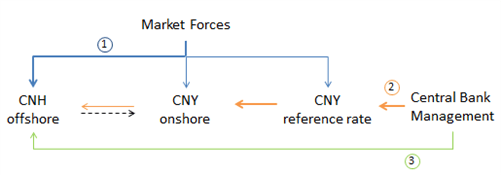

Yuan’s onshore rate (CNY) and offshore rate (CNH) can impact each other under the current managed-floating exchange rate system. China’s Central Bank can also impact the Yuan prices through policy tools.

- Market forces can impact all three rates but may in different degrees. As China’s financial markets are not fully-opened, external factors could bring a reduced impact to the onshore CNY market than they may do in a fully-opened market. As China continues to open up its financial markets and promote the Yuan’s globalization process, the onshore CNY could move towards a free-floating currency further.

- The PBOC can directly guide the onshore CNY rate through the daily reference rate and the trading band. As the CNY and CNH are correlated, the impact will be passed to the offshore Yuan too.

- When the CNH market is extremely volatile, the central bank can intervene the market using uncommon measures, such as hiking the CNH borrowing costs to squeeze out Yuan sellers. An example is that on January 12, 2016, the overnight Hong Kong Interbank Borrowing Rate (HIBOR O/N) jumped to 66.82% from below 3% on average.

As market forces and the PBOC’s influence may work differently in the onshore and offshore markets, we may see discrepancies between the CNY and CNH prices from time to time.

Follow the DailyFX Central Bank Calendar for the latest update on central bank rates.

THE ROLE OF SAFE AND CFETS

Most traders may have heard of the PBOC, but it is not the only regulator with a say on Yuan rates. There is another regulator and one subsidiary of the PBOC that can impact the Yuan’s exchange rate.

State Administration of Foreign Exchange (SAFE) is an administrative agency that develops foreign exchange policies and regulates the foreign exchange market. It is a deputy-ministerial-level agency and half-level lower than the PBOC; the latter is a ministerial-level state agency. The PBOC and SAFE combined is equivalent to the Federal Reserve in the US.

As stated above, the PBOC releases the reference rate on a daily basis. The rate is not released directly by the headquarters in Beijing. Instead, it is announced by China Foreign Exchange Trade System (CFETS) Center, a subsidiary of PBOC in Shanghai. Besides the daily reference rate, the CFETS reports other important rates, such as swaps, bonds and Yuan indices.

READ MORE ON THE YUAN

- For Yuan trading ideas and technical analysis, view the latest CNH weekly forecast report.

- Find out more about the Chinese currency, with our in-depth guide on CNH vs CNY: Differences Between the Two Yuan.

-- Written by Renee Mu, DailyFX Research Team