The upcoming bull market will have a slow and steady start, centred on industrial and labour force recovery after 8 years of stagnation. Low interest rate, inflation, and oil price will benefit consumers and encourage firms to increase productivity. Against this backdrop, high yield equity and fixed income in developed market will continue to flourish. Nevertheless, downside risk remains inherent as we have seen in 2015, at any chain reactions caused by emerging market meltdown, commodity rout, or departure of risk appetite.

Growth in emerging Asia may solidify for the first time since 2010 while China sets for a steady 6.5% annual growth target with supportive interventions to stem volatility and stimulate the economy. In Australia, interest rate will remain accommodative as the country shifts from mining into technology. Commodities are likely under pressure as low price and ample supply offset output cuts. Investors in Asia Pacific could find opportunities for moderate returns in developed stock markets and/or short of commodities.

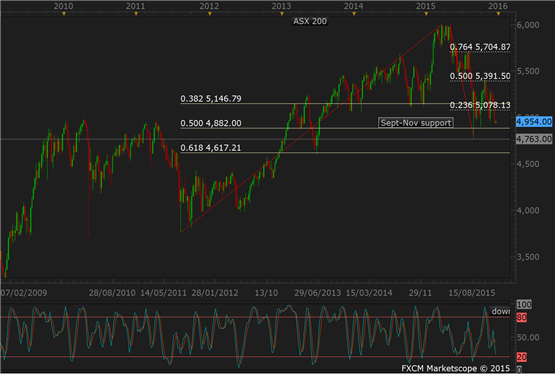

Weekly technical chart of the Australian stock index ASX 200 shows support levels ahead, where dip buying may occur in anticipation of a rebound. The index has risen consistently since 2009, with recent disruption caused by commodity and Chinese stock routs.