S&P 500 OUTLOOK, POWELL TESTIMONY, EU SUMMIT, COLOMBIAN ELECTION RUNOFF - TALKING POINTS

- S&P 500 volatility could rise on geopolitical risks in Europe ahead of the EU summit

- Price oscillations likely to be amplified by Fed Chairman Jerome Powell testimonies

- French equities, Colombian Peso may rise as market-friendly outcomes appear likely

Trade Smarter - Sign up for the DailyFX Newsletter

Receive timely and compelling market commentary from the DailyFX team

COLOMBIA ELECTION RUNOFF

After the first round of voting in the Colombian presidential election yielded inconclusive results - that is, no candidate was able to secure a majority - a second round was scheduled. The day after the tally was announced, the Colombian Peso surged against emerging markets and G10 FX. On May 31, USD/COP fell over 3.20%, the largest one-day decline since August 2015.

On Sunday, Colombians went to the ballot box again to cast their votes between the left-wing populist Gustavo Petro and construction magnate Rodolfo Hernandez. Analysts attributed the rally to an “anyone but Petro” bet. His policy proposals include overhauling the private pension system, phasing out oil and coal, and raising taxes.

READ MORE: How to Trade the Impact of Politics on Global Financial Markets

Some of the candidates who were not able to make it to the second round started to throw their support behind Hernandez, echoing broader anti-Petro sentiment. If prevailing trends continue, USD/COP may continue to take a hit, despite the Greenback’s strength against most G10 and emerging market FX. The currency cross may rise if Petro manages to win, however. See my thoughts in greater detail here.

FRENCH LEGISLATIVE ELECTION

In the first round of legislative elections, total voter turnout was just 52.49 percent, which smashed the prior record low set in 2017. Among its European neighbors, France now has the same amount of domestic political participation as Poland, Romania, and Croatia. See a breakdown of the first legislative election here.

For more updates on geopolitical risks, follow me on Twitter @ZabelinDimitri.

As for the second round, the voters’ demographic composition suggests that Emmanuel Macron’s center-right coalition Ensemble! has the advantage. His challengers, Jean-Luc Melenchon and the NUPES coalition, are typically powered by younger voters who are generally less likely to appear at the ballot box in proportion to their older counterparts.

If Mr. Macron is able to secure a majority, French equity markets will likely inch higher on the back of the comparative certainty and consistency in policy that the incumbent will bring. Markets do not like major shifts in policy, particularly if they come from candidates who are characterized by a nationalist or populist disposition.

Trading Strategies and Risk Management

Global Macro

Recommended by Dimitri Zabelin

EU SUMMIT ON UKRAINE

On June 23, European Union leaders will convene in Brussels to discuss the war in Ukraine and the multi-iterated ripple effects it is having on the regional and global economy. Policymakers will also discuss whether to grant Ukraine EU candidacy status, to the consternation of Russian President Putin who has adamantly opposed the country’s move toward the Western sphere of influence.

French and German heads of state both spoke with Putin and urged him to hold direct and serious talks with his Ukrainian counterpart. The Kremlin stated that it is open to “renewing dialogue with Kyiv”, but also warned of “further destabilization” if European countries continue to send arms to Ukraine.

Russia’s president emphasized that efforts to export grain from Ukrainian ports - currently blocked by Russian warships - should be reciprocated by the lifting of “relevant sanctions”. The outcome of the summit - particularly as it relates to Ukraine’s admittance status to the EU - could inflame the Kremlin, potentially escalating the conflict and putting equity markets on the defensive.

Foundational Trading Knowledge

Forex Fundamental Analysis

Recommended by Dimitri Zabelin

POWELL TESTIMONY

After raising interest rates by 75 basis points for the first time since 1994, Fed Chair Jerome Powell will testify in front of the US Senate Banking Committee and the House Committee on Financial Services. The central bank reiterated its “unconditional” commitment to price stability last week, suggesting that aggressive tightening will likely continue.

Mr. Powell said the central bank could raise rates by 50 or 75 basis points in July, depending on inflation and economic activity. An unintended risk Fed tightening could have on the financial system is the pressure it would put on debt instruments (leveraged loans, collateralized debt obligations [CLOs]) that were aggressively issued under the outgoing ultra-easy credit regime.

According to US bank regulators, many leveraged loans possess weak structures. They “reflect layered risks that include some combination of high leverage, aggressive repayment assumptions, weak covenants, or terms that allow borrowers to increase debt, including draws on incremental facilities”.

Consequently, higher interest rates combined with the prospect of slower economic activity mean firms with low credit ratings, steeper debt payments, and lower profits margins become highly at risk of default. As it stands, the leveraged loan index is trading at its lowest point since November 2020.

Reverberations in this multi-trillion-dollar market will almost certainly spill over across asset classes. In the case of rising defaults, the US Dollar and Japanese Yen would likely rise the most against more cycle-sensitive currencies like the Australian and New Zealand Dollars. Consequently, Fed policy - and key economic data - will be crucial to monitor.

PMI DATA FOR JUNE

Both the US and Eurozone will be publishing flash PMI manufacturing, services, and composite data for June. Estimates across the three categories for both geographies are still indicating an expansion - that is, a reading above 50. Meanwhile, China continues to hover in contractionary territory - a print below 50 - due to its restrictive Covid-19 lockdown measures.

Absent shocking disappointments, weaker-than-expected figures could push equities higher if markets believe economic activity will not be drastically dragged down, but perhaps just enough to throttle higher interest rates. Having said that, the lag periods between when a policy is announced, then implemented, and then absorbed into the overall economy can be quite long. This weakens the connection between higher-frequency economic data and officials’ tactics.

Introduction to Technical Analysis

Learn Technical Analysis

Recommended by Dimitri Zabelin

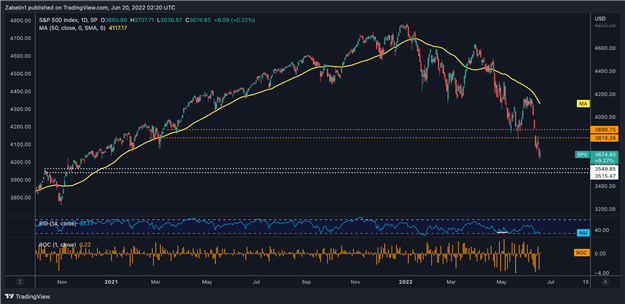

S&P 500 TECHNICAL ANALYSIS

The S&P 500 continues to fall, with the 50-day moving average showing a steepening decline. The benchmark equity index gapped lower between June 9th and 13th, skipping over two layers of support at 3890.75 and 3818.26. It is now coming closer to what could be technically-significant support between 3549.85 and 3515.47.

S&P 500 - Daily Chart

S&P 500 chart created using TradingView

The relative strength index (RSI) shows the S&P 500 is close to so-called “oversold” territory, though this is no guarantee of a turnaround. While the possibility of a brief bounce from this two-leveled floor is possible, traders should curb their enthusiasm. The road to recovery will be arduous, and the fundamental circumstances support a bearish outlook.