GOLD, XAU/USD, Federal Reserve, Powell, Rates, Real Yields - Talking Points

- Gold steadied this week as a hawkish Fed accelerated hike expectations

- Real yields could be the key for gold as higher nominal yields kick in

- Fed rate rises might lower inflation expectations. Will that sink XAU/USD?

Gold price headwinds are building as the Federal Reserve races to catch up with the curve.

Fed Chair Jerome Powell kicked things off on Monday by not ruling out a 50 basis-point (bp) hike at a Federal Open Market Committee (FOMC) meeting this year, if necessary.

Specifically, he said, “if we conclude that it is appropriate to move aggressively by raising the federal funds rate by more than 25 basis points at a meeting or meetings, we will do so.”

The market is now pricing in around seven rate hikes of 25 bp in the six meetings left in 2022, implying a 50 bp move at some point.

On Tuesday, St. Louis Fed President James Bullard added to his hawkish credentials by saying that “faster is better” when it comes to rate hikes.

These hawkish comments have lifted Treasury yields across the curve.

This environment can manifest itself in two ways for a lower gold price. The higher and rising nominal rate of return on fixed interest assets presents itself as better alternative to a non-yielding asset such as gold.

Secondly, if the Fed is perceived to be genuine about fighting inflation, then market priced inflation may come down. This increases the real return on debt investments. The real return being the nominal rate less the inflation rate over the same tenure.

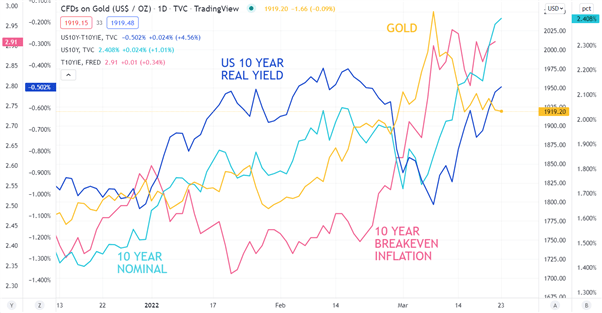

Looking at the chart below, we can see that the rally in gold earlier this month coincided with the increase in market priced 10-year breakeven inflation. This pushed down 10-year real yields.

Following that peak in gold, the 10-year breakeven rate remained relatively steady, but nominal yields picked up, lifting real yields and gold fell at the same time.

If the Fed continues to recognise that they need to raise rates aggressively, this could undermine gold further.

The outlier to this perspective is the unknown consequences of the Russian invasion of Ukraine and a closer look at the price action is warranted.

GOLD, US 10-YEAR NOMINAL, US 10-YEAR INFLATION AND US 10-YEAR REAL YIELD

Introduction to Technical Analysis

Moving Averages

Recommended by Daniel McCarthy

GOLD TECHNICAL ANALYSIS

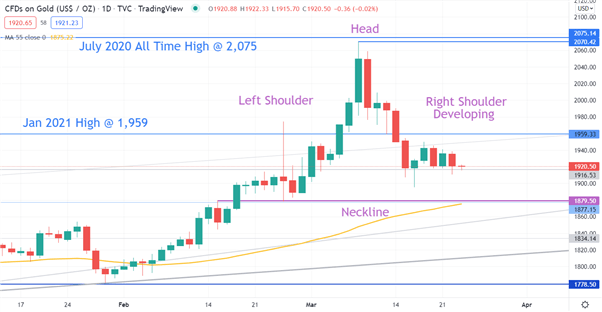

There are 2 observations to note in the gold chart below. A double top formation and a head and shoulders formation.

The all time high for gold was achieved in July 2020 at 2,075.14. Earlier this month the price rallied toward it but failed and made a peak of 2,070.42 creating a double top. This failure to break higher could be a bearish signal.

A bearish head and shoulder pattern is emerging and a break below the neckline may confirm the pattern.

Risk management techniques are always crucial and need to be looked at closely.

--- Written by Daniel McCarthy, Strategist for DailyFX.com

To contact Daniel, use the comments section below or @DanMcCathyFX on Twitter